日次纏絡分心線定量化戦略

概要

日次巻き込み分散ライン定量戦略は、移動平均線と最高安値指標に基づく短期定量取引戦略です。SSL混合指標のEXIT矢印を利用して売買ポイントを判断し、QQE指標でフィルタリングを行い、ATR指標でストップロス水準と分割増持仓位を計算します。本戦略は、市場の変動に敏感でリスク管理を重視する投資家に適しています。

戦略の原理

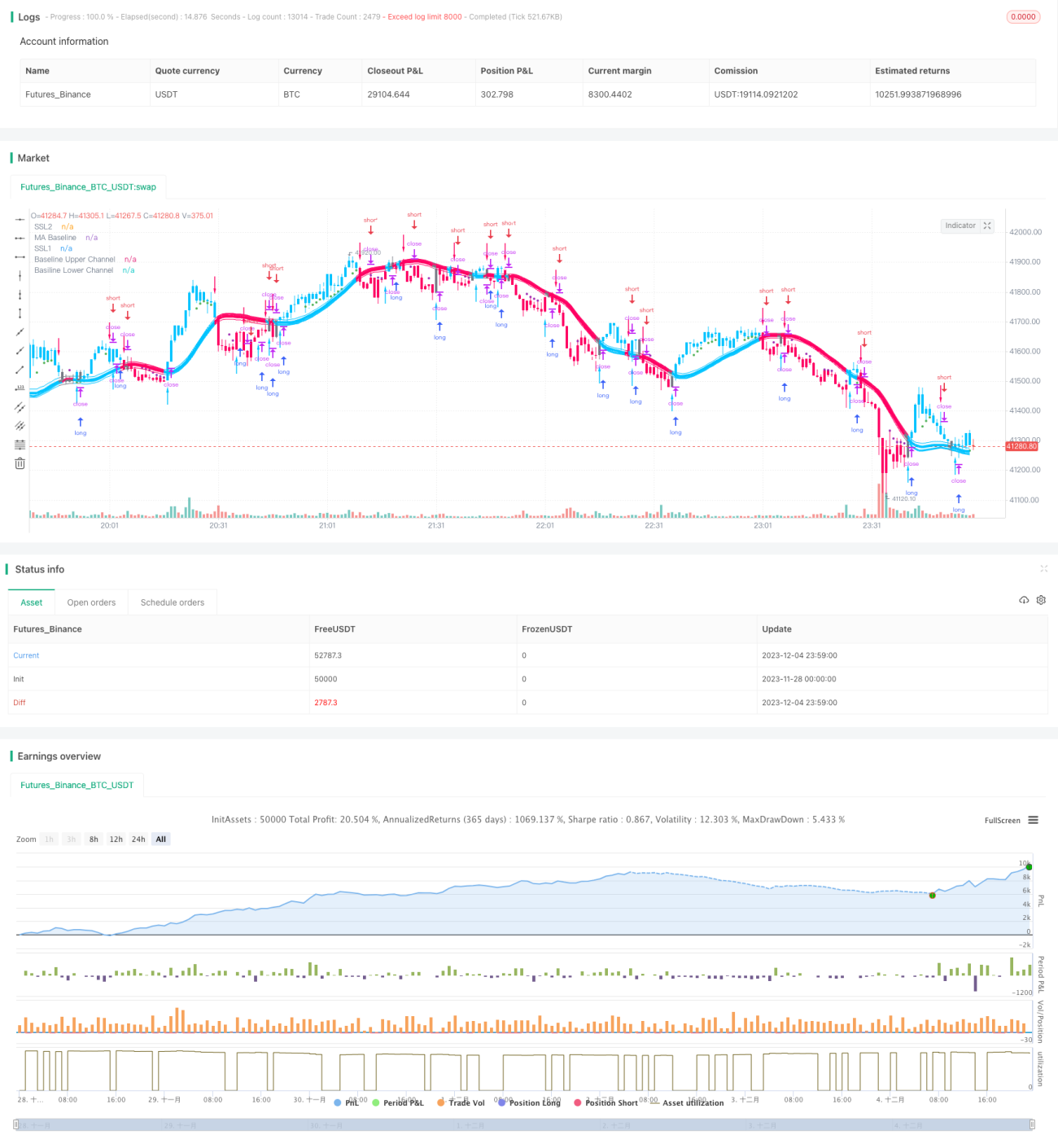

本戦略は、SSL混合指標のEXIT矢印を使用して売買のエントリーポイントを判断します。EXIT矢印の上方はEXIT高値、下方はEXIT安値です。終値がEXIT高値を下回って抜けたときに売りシグナルが発生し、終値がEXIT安値を上回って抜けたときに買いシグナルが発生します。

シグナルの信頼性を高めるため、本戦略ではQQE指標を補助フィルター条件として導入します。EXIT矢印によって生成されたシグナルは、QQE指標が同じ方向を示している場合にのみ実行されます。

リスクを管理するため、本戦略ではATR指標の倍数を使用してストップロス水準と分割増持仓位を計算します。空売りのストップロスは終値+ATR×1.8、買いのストップロスは終値-ATR×1.8です。3回に分割して増仓し、各回の増仓金額は初期金額の10%とし、増仓位はそれぞれ終値-ATR×0.1、終値-ATR×0.3、終値-ATR×0.7とします。

各増仓には個別のストップロスが設定されており、最初の増仓分(金額の20%)はストップロス水準に達した時点で損切りされ、残りのポジションは引き続き保有されます。

戦略の利点

- EXIT矢印で利益を獲得し、迅速に損切りしてリスクを効果的に管理

- QQE指標によるフィルタリングでシグナルの精度を向上

- ATR指標を利用して市場の変動に応じたストップロスと増仓水準を計算し、リスク管理がより精密

- 分割増仓により、トレンドを十分に捉えて利益を拡大

戦略のリスク

- 含み益のあるポジションが一部損切りされると、残りのポジションがさらに損切りされるリスクに直面する可能性がある。全体利食いや株式本体のファンダメンタルズに基づく利食いを検討すべき。

- EXIT矢印とQQE指標の市場変動に対する感度が異なるため、矛盾したシグナルが発生する可能性がある。パラメータを調整してシグナル競合を減らすべき。

- 増仓が過度に積極的だと、高値追いや底値売りの状況になりやすい。情勢を見極め、レバレッジ水準を引き下げるべき。

最適化の方向性

- 株式本体のファンダメンタルズ指標(例:PBR、PER、配当利回りなど)と組み合わせて利食いを行う。合理的な利食い水準を設定する。

- QQE指標のパラメータを調整し、EXIT矢印が生成するシグナルと一致させる。

- 市場の熱度に応じて増仓比率を引き下げ、レンジ相場では増仓を減らす。

- 最大ドローダウン、リスクリワード比などの指標を用いて最適なパラメータ組み合わせをテストする。

まとめ

本戦略は、SSL混合指標のEXIT矢印をシグナルの中核とし、QQE指標とATR指標をフィルタリングおよびストップロスに利用します。分割増仓により利益を増幅します。これは短期定量戦略であり、市場の短期的トレンドを追跡する状況に適しています。本戦略はドローダウン管理とリスク管理の能力を有しますが、シグナル競合や高値追い・底値売りなどのリスクに注意する必要があります。株式のファンダメンタルズに基づく利食い方法を組み合わせ、市場のレンジ相場を判断し増仓比率を調整する際により慎重になることができれば、本戦略の利益余地はさらに大きくなるでしょう。

- 1