価格変化率と移動平均線に基づく定量化戦略

1

Follow

1802

Followers

概要

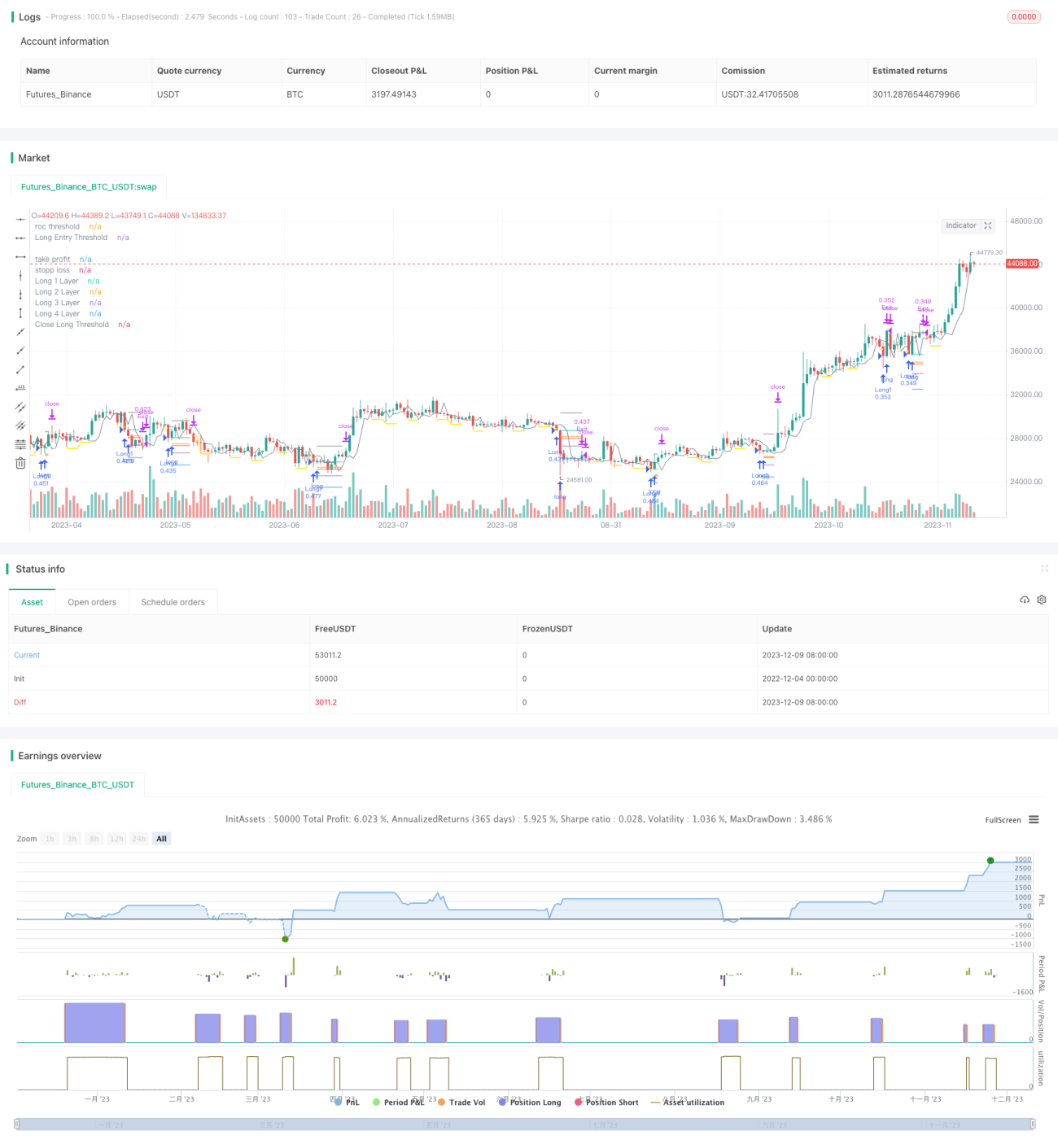

この戦略は、価格変化率と移動平均線のテクニカル指標を組み合わせ、買いポイントと売りポイントを正確に特定します。価格が明確に下落したときに買い閾値を設定し、さらに下落したときにロングポジションを建てます。価格が上昇したときに売り閾値を設定し、さらに上昇したときに決済します。同時に、ポジション追加方式を採用し、複数回に分けて買い、コストを低減します。

戦略の原理

買いロジック

- 価格変化率ROCを計算し、買い閾値ラインを設定します。

- 価格が買い閾値ラインを下回った時点を記録し、買い制限ラインを起動します。

- 買い制限ラインは入力パラメータに基づいて持続時間を設定し、期限切れ後に無効になります。

- 価格がさらに下落して買い制限ラインを下回った時点で、最初のロングポジションを建てます。

売りロジック

- 価格変化率ROCを計算し、売り閾値ラインを設定します。

- 価格が売り閾値ラインを上回った時点を記録し、売り制限ラインを起動します。

- 売り制限ラインは入力パラメータに基づいて持続時間を設定し、期限切れ後に無効になります。

- 価格がさらに上昇して売り制限ラインを上回った時点で、全てのロングポジションを決済します。

リスク管理

戦略にはストップロスと利益確定機能が組み込まれており、パラメータをカスタマイズして、ポジション保有中のリスクをリアルタイムで制御できます。

ポジション追加方式

取引ポジションを建てるたびに、入力パラメータに基づいて一定の割合で後続の買い価格を設定し、分割買いによるポジション追加を実現します。

優位性分析

- 価格変化率指標ROCを使用して売買ポイントを特定。ROCは価格変化に非常に敏感で、売買ポイントの精度が高い。

- 制限ライン方式で売買タイミングをさらに確認し、偽のブレイクアウトを回避。

- ポジション追加方式により、リスクを管理可能な範囲に抑えつつ市場価値に追随。

- 組み込みのストップロス・利益確定機能で、個別ポジションのリスクを厳格に制御。

リスクと対策

- 市場が激しく変動した場合、戦略が過剰なポジションを建てる可能性がある。対策:ポジション追加のパラメータを適切に設定し、総ポジション数を制限する。

- 価格が方向感のないレンジ相場では、ストップロスや利益確定が頻繁にトリガーされる可能性がある。対策:利益確定・ストップロスの幅を適度に広げるか、機能を停止する。

最適化提案

- 他の指標と組み合わせてエントリータイミングをフィルタリングする。例えば移動平均線と併用し、価格が移動平均線を下回った場合のみROC指標を採用する。

- ポジション追加ロジックを最適化し、特定の条件を満たした場合のみポジション追加を開始する。例えば、価格がさらに一定以上下落した場合にのみ追加で買いを行う。

- 銘柄によってパラメータ設定は大きく異なるため、十分なバックテストと模擬取引により最適なパラメータ組み合わせを見つける必要がある。

- 適応型の利益確定・ストップロスを設定し、市場のボラティリティに応じて異なるストップロス幅を設定することができる。

まとめ

本戦略はROC指標を活用して売買ポイントを正確に特定し、制限ライン方式でシグナルをフィルタリングし、組み込みの利益確定・ストップロスでリスクを防ぎ、ポジション追加により利益を拡大します。パラメータを適切に設定すれば、リスクを管理可能な範囲に抑えつつ超過収益を得ることが可能です。今後はシグナルフィルタリングとリスク管理メカニズムをさらに最適化し、より多くの市場環境に適応できるようにすることが期待されます。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1