ATRチャネルと移動平均線のリバーサルに基づくアルゴリズム取引戦略

1

Follow

1802

Followers

概要

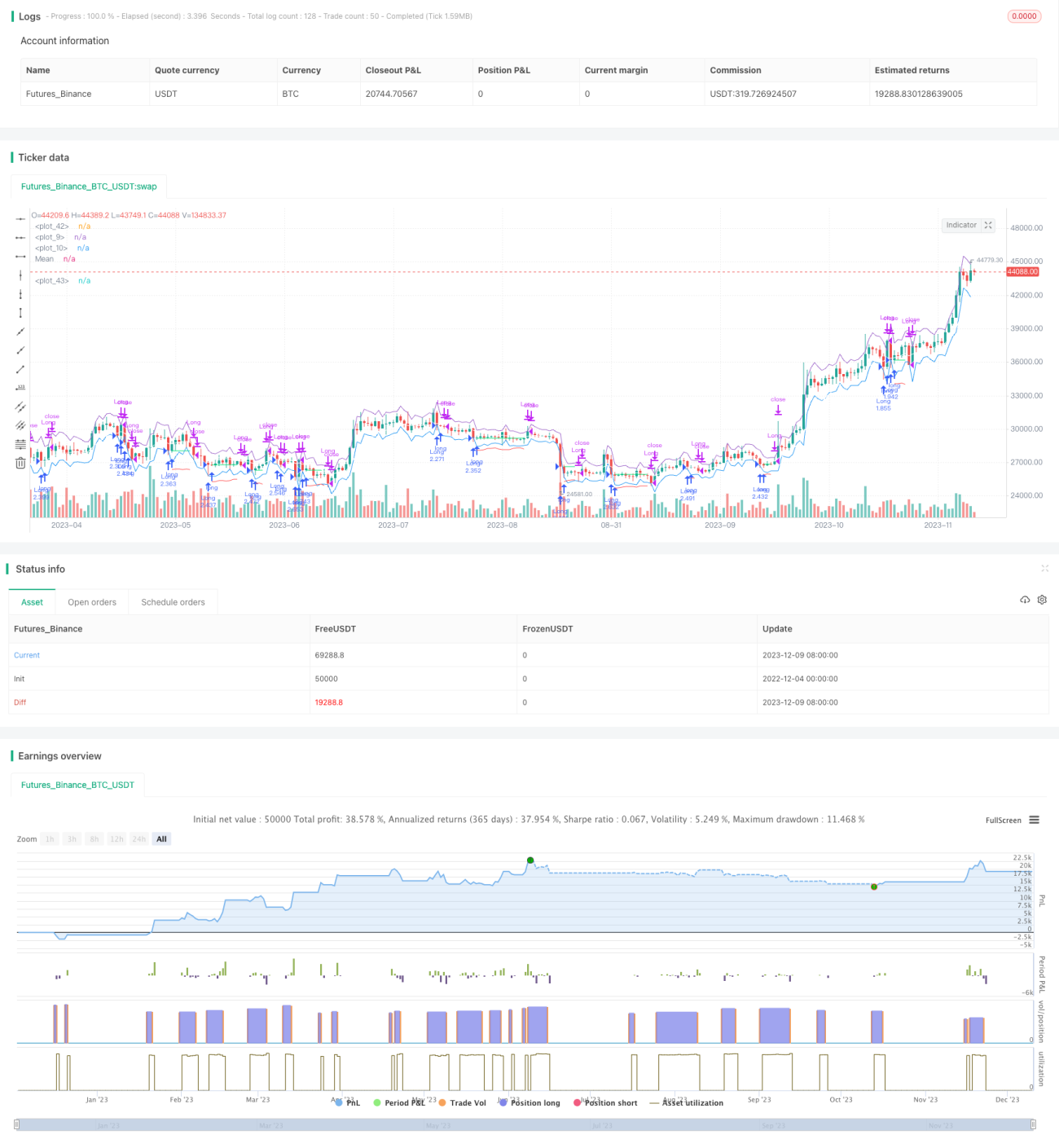

本戦略はロング専用の戦略であり、価格がATRチャネルの下限をブレイクしたタイミングでエントリーし、ATRチャネルの移動平均線またはATRチャネルの上限で利確エグジットを行います。また、ATRを用いてストップロス価格を計算します。この戦略は短期のスキャルピングトレードに適しています。

戦略の原理

価格がATRチャネルの下限を下回った場合、異常な下落が発生したことを示します。このとき、次のローソク足の始値でロングエントリーします。ストップロス価格はエントリー価格からATRストップロス係数×ATRを差し引いた値です。利確価格はATRチャネルの移動平均線またはATRチャネルの上限とし、現在のローソク足の終値が前のローソク足の最安値を下回った場合は、前のローソク足の最安値を利確価格とします。

具体的には、本戦略は以下のロジックで構成されています。

- ATRとATRチャネルの移動平均線を計算

- 時間フィルター条件を設定

- 価格がATRチャネルの下限を下回った場合、ロングエントリー可能とマーク

- 次のローソク足の始値でロングエントリー

- エントリー価格を記録

- ストップロス価格を計算

- 価格がATRチャネルの移動平均線またはATRチャネルの上限を上回った場合、ポジションを決済して利確

- 価格がストップロス価格を下回った場合、ストップロスでエグジット

優位性分析

本戦略には以下の優位性があります。

- ATRチャネルを使用してエントリーと利確を行うため、信頼性が高い

- 異常な下落後にのみロングエントリーするため、高値掴みを防止

- ストップロスルールが厳格であり、リスクを効果的にコントロール

- 短期のスキャルピングトレードに適しており、長期保有の必要がない

- ルールがシンプルで理解しやすく、実装と最適化が容易

リスク分析

本戦略には以下のリスクも存在します。

- 頻繁な取引による手数料とスリッページのリスク

- ストップロスが連続でトリガーされる可能性

- パラメータの最適化が不適切な場合、戦略のパフォーマンスに悪影響

- 対象銘柄の価格変動が大きい場合、ストップロスの幅が大きくなりすぎる可能性

ATRの期間を調整したり、ストップロス係数を小さくすることで上記のリスクを低減できます。また、取引手数料が低い証券会社を選ぶことも重要です。

最適化の方向性

本戦略は以下の点からさらに最適化できます。

- 他のインジケーターによるフィルターを追加し、最適なエントリータイミングを逃さないようにする

- ATR期間パラメータの最適化

- 再エントリー機構の追加を検討

- ストップロス幅の動的調整

- トレンド判断ルールを追加し、逆張りエントリーを回避

まとめ

本戦略は全体的にシンプルで実用的な短期のブレイクアウト・リバーサル戦略です。明確なエントリールール、厳格なストップロスメカニズム、および完成された利確方法を備えています。また、パラメータ調整の余地もあり、最適化が可能です。トレーダーが適切な対象銘柄を選択し、ストップロスでリスクを管理できれば、本戦略は良好な結果を得られるでしょう。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1