1

Follow

1802

Followers

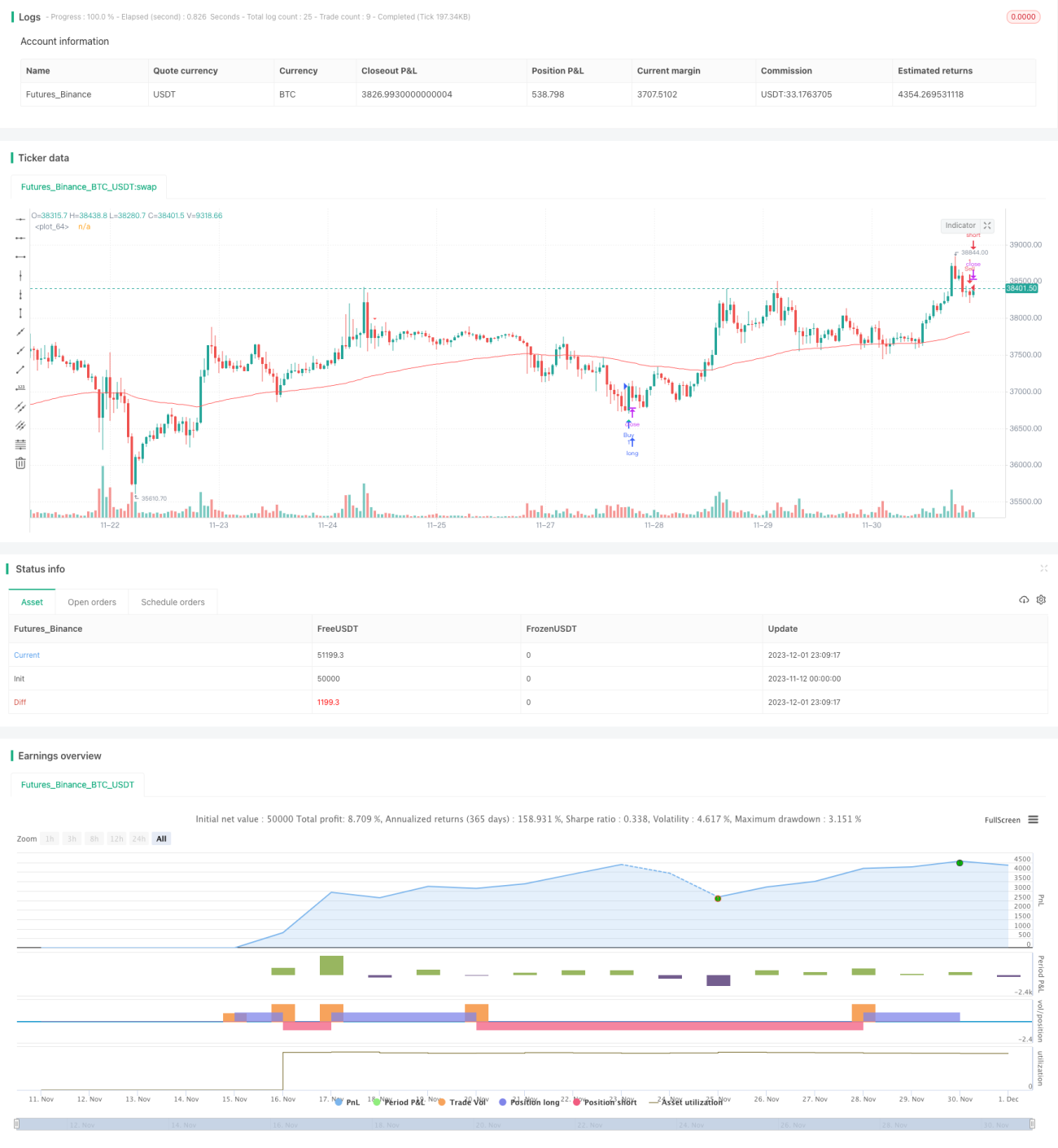

概要

これは、複数のテクニカル指標に基づく逆張り取引戦略です。CCI、モメンタム指標、RSIなどの指標を組み合わせ、潜在的な買い・売りの取引機会を特定します。指標が買われ過ぎ・売られ過ぎのシグナルを示し、価格が反落した場合に取引シグナルを発します。

戦略の原理

本戦略の取引シグナルは、カスタム指標「Edri極点売買ポイント」に由来します。これはCCI、モメンタム指標、RSIのクロス状況を総合的に判断します。具体的なロジックは以下の通りです。

買いシグナル条件:

- 「Edri極点売買ポイント」指標が買いシグナルを発する(CCIが0ラインを上抜ける、またはモメンタム指標が0ラインを上抜け、かつRSIが売られ過ぎラインを下回っている)

- 価格が100期間EMAまで引き戻されるか、それを下回る

売りシグナル条件:

- 「Edri極点売買ポイント」指標が売りシグナルを発する(CCIが0ラインを下抜ける、またはモメンタム指標が0ラインを下抜け、かつRSIが買われ過ぎラインを上回っている)

- 価格が100期間EMAまで引き戻されるか、それを上回る

本戦略では、通常のダイバージェンスを探す条件をオプションで設定することもできます。すなわち、RSIと価格の間に明確なダイバージェンスが生じた場合のみ取引シグナルを発生させます。

取引シグナルが成立した場合、ストップロスはエントリー価格 ± 2ATR、利食いはエントリー価格 ± 4ATRに設定されます。これにより、市場の変動度合いに応じた適切な損切り・利確範囲を設定できます。

優位性分析

- 複数の指標を総合判断することで、単一指標の偽シグナルを回避しやすい

- 逆張り取引方式は、レンジ相場における中短期の取引機会を捉えるのに有効

- ATRによる損切り・利確方式は、市場のボラティリティに応じてポジションを柔軟に調整可能

- ダイバージェンス条件を設定することで、極端な買われ過ぎ・売られ過ぎでない状況でのエントリーを回避できる

リスク分析

- インジケーターのパラメーター設定が不適切だと、取引機会を逃したり、誤ったシグナルが増える可能性がある

- 逆張り取引パターンは、トレンド相場で連続して損切りになるリスクがある

- ATRには遅延性があり、急激な相場変動時に損切り・利確ポイントを適時に更新できないことがある

解決策:

- パラメーターを複数回バックテスト・最適化し、最適な組み合わせを見つける

- トレンドが強い場合には本戦略の使用を一時停止することも検討する

- 移動ストップロスやトレーリングストップなど、他の損切り方法と組み合わせる

最適化の方向性

- 異なるパラメーターの組み合わせをテストする(CCI・モメンタム指標の期間、RSIパラメーター、ATR倍率など)

- 他の補助フィルター条件を追加する(価格パターン、出来高変化など)

- ポジション管理方法を調整する(ATR値に基づくポジション比率設定など)

- 異なる銘柄・時間足に対応するパラメーターテンプレートを用意する

- トレンドフォロー機構を組み込み、トレンド相場では逆張り取引を一時停止することを検討する

まとめ

本戦略は主にレンジ相場に適用し、中短期的な反転を捉えることで安定した収益を狙います。価格の短期的な急伸・急落を識別し、複数の指標に基づいて取引シグナルを生成します。適切なパラメーター最適化とリスク管理により、本戦略の利点を有効に活用できます。ただし、逆張り取引に固有の欠点、すなわち強いトレンド下では損失が続く可能性があることに注意が必要です。総じて、本戦略は一定の定量取引およびリスク管理の経験を持つ投資家に適しています。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1