MACDトレンド追跡短期戦略

1

Follow

1802

Followers

概要

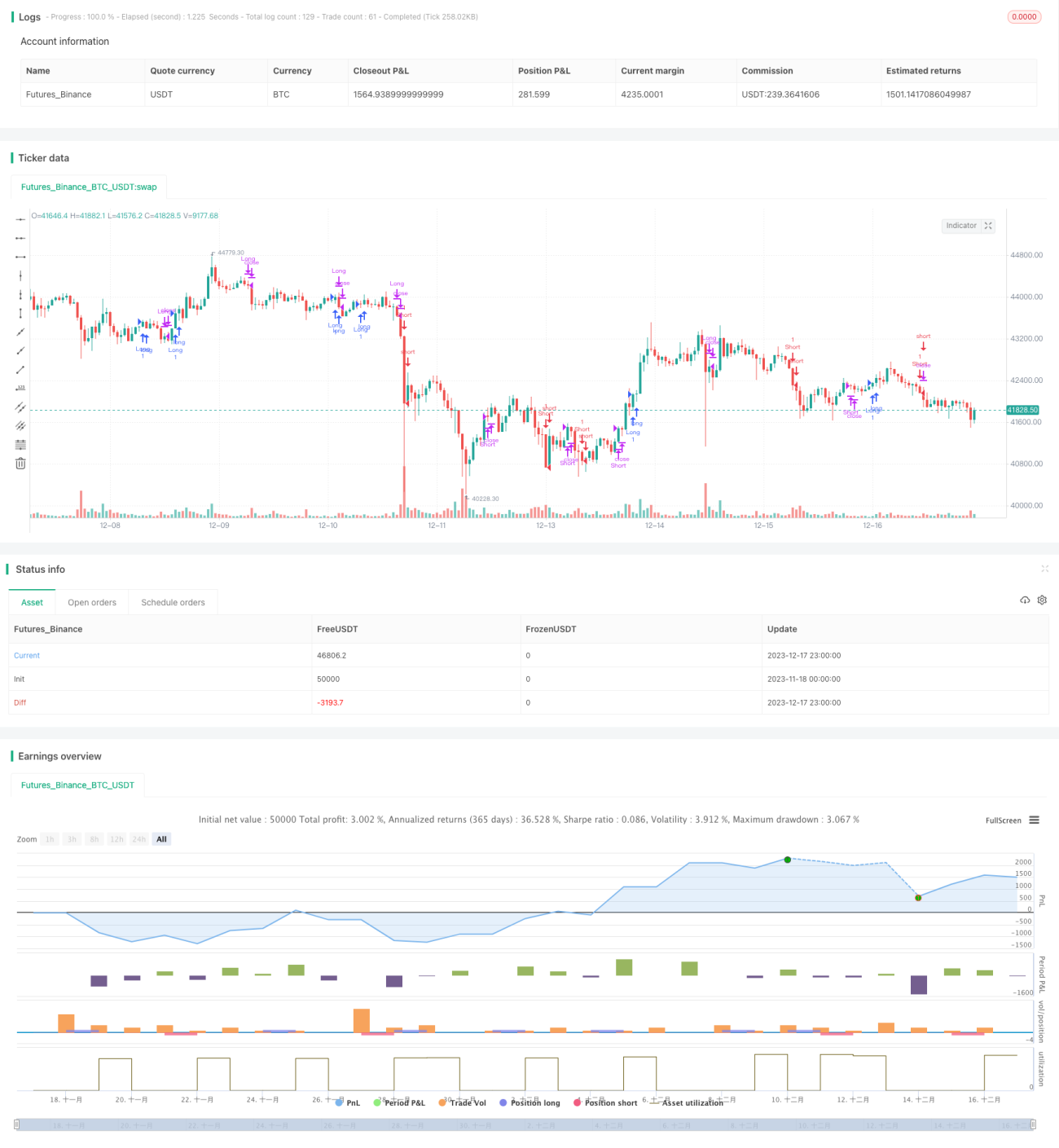

MACDトレンド追跡短期戦略は、移動平均線、MACDインジケーター、ウィリアムズ%Rインジケーターを組み合わせた短期売買戦略です。本戦略は3つのインジケーターの異なる組み合わせを活用し、ロング・ショートポジションのエントリーおよびエグジット条件を形成することで、短期価格のトレンド特性を捉えます。

戦略の原理

本戦略の主な取引ロジックは以下の通りです。

- 価格が指数移動平均(EMA)を上抜けたらロング、下抜けたらショートと判断します。

- MACDの短期線が長期線を上回ればロング、下回ればショートと判断します。

- ウィリアムズ%Rの短期移動平均線が長期移動平均線を上回ればロング、下回ればショートと判断します。

- これら3つの条件の組み合わせによりエントリーを判断します。

- 逆の条件が成立した場合にエグジットを判断します。

EMAで大局的なトレンド方向を判断し、MACDで短期的な価格モメンタムを判断することで、本戦略は良好なエントリーポイントで価格のトレンド特性を捉え、利益を獲得します。また、ウィリアムズ%Rは銘柄の買われ過ぎ・売られ過ぎの状況をさらに検証し、偽のブレイクアウトを回避するために使用します。

戦略の優位性

このような複数のインジケーターを組み合わせた構造は、典型的な短期トレンド追跡戦略であり、主に以下の優位性があります。

- 3つのインジケーターが相互に検証し合うため、偽シグナルの発生確率を低減できます。

- EMAが主要トレンド方向を判断し、MACDが短期的なモメンタムの強弱を判断します。

- ウィリアムズ%Rにより、激しい変動の中で高値追いや底値売りを回避できます。

- 逆条件の組み合わせでエグジットを判断し、リスク管理と緊密に連携します。

戦略のリスク

本戦略には以下のような主なリスクも存在します。

- 複数のインジケーターを組み合わせた構造が複雑であり、パラメータ最適化が難しい。

- 短期売買が頻繁に行われるため、取引コストが高くなる可能性がある。

- 真のトレンド転換点を正しく判断できず、損失リスクが生じる。

対策としては、主にパラメータ最適化と損切りに関して、最適なパラメータの組み合わせを模索し、適切な損切り水準を設定して、1回の取引における最大損失を抑制します。

戦略の最適化方向

本戦略は主に以下の点で最適化が可能です。

- より多くのインジケーターパラメータの組み合わせをテストし、最適なパラメータを探す。

- 出来高など、より多くのデータソースを追加して補助的に判断する。

- 動的ストップロスやトレーリングストップを設定し、リスク管理を強化する。

- 機械学習モデルを組み合わせて、真のトレンド転換点を判断する。

まとめ

MACDトレンド追跡短期戦略は、複数のインジケーターの利点を総合的に活用し、短期トレンドを判断すると同時にリスクをコントロールします。パラメータ最適化、損切り水準の設定、およびより多くのデータソースの導入により、戦略の勝率と収益性をさらに向上させることができます。本戦略の考え方は、さらなる拡張と深い研究に値します。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1