Momentum Breakthrough Moving Average Trading Strategy

Overview

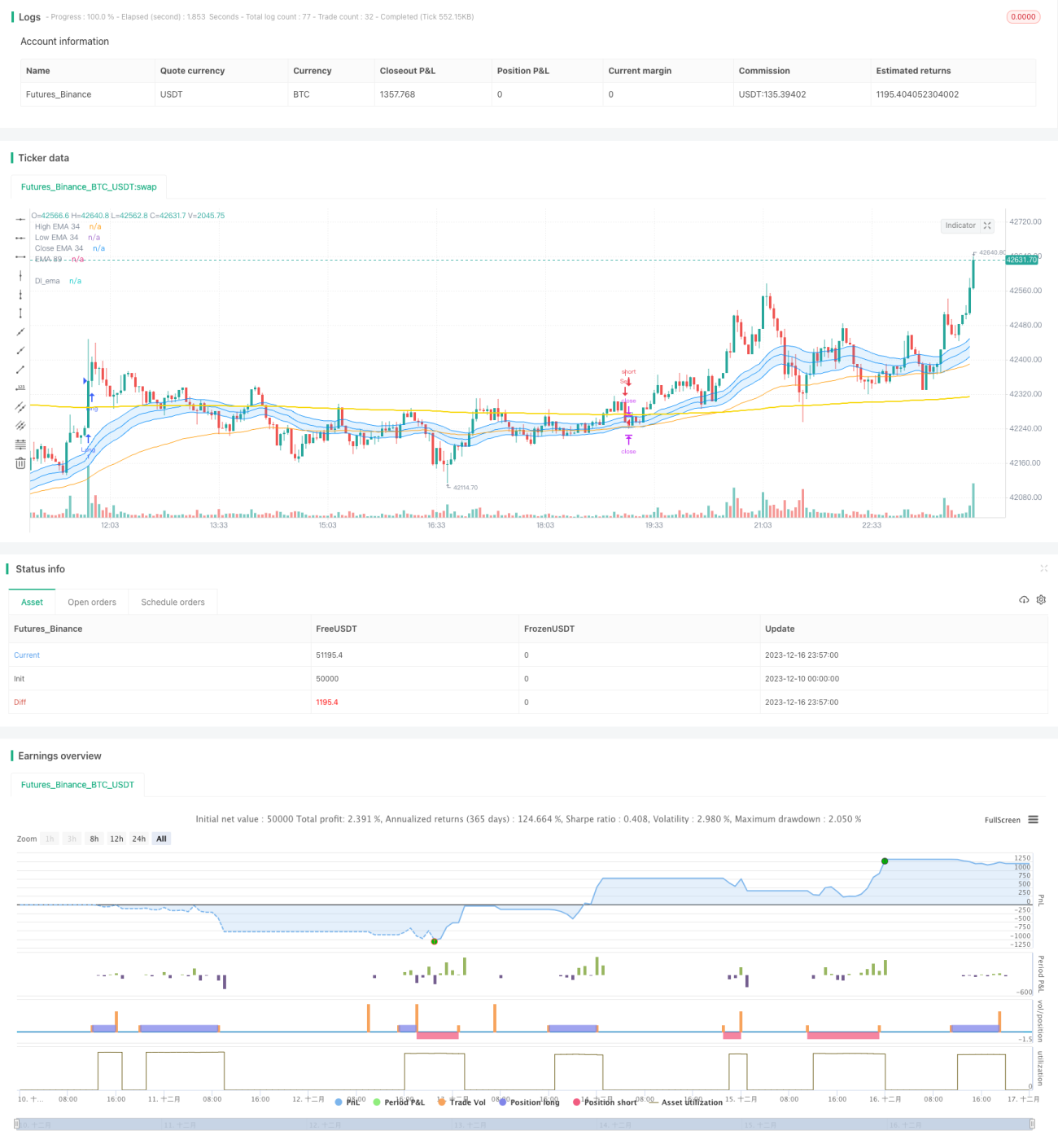

This strategy is a trend tracking strategy that combines momentum indicators and moving averages. It uses exponential moving averages as the main trend judgment tool and issues buy and sell signals in combination with high trading volume. The strategy is suitable for medium and long term holdings to track major market trends.

Strategy Principles

-

Use 34-period EMA as the main tool for trend judgment. When the price crosses above the EMA, it is a bullish signal, and when it crosses below, it is a bearish signal.

-

Compare the 21-day moving average of volume with 1.5 times the recent average. If the current volume is greater than 1.5 times the average, it is considered high volume.

-

Buy signals are only issued when the price crosses the EMA upward and the volume is high. Sell signals are only issued when the price crosses the EMA downward and the volume is high.

-

After opening a position, set stop loss and take profit ratios, which can be customized.

By comprehensively considering factors such as trends, momentum and risk control, it is relatively comprehensive and stable.

Advantage Analysis

-

Using EMA to determine the main trend direction of the market can effectively track medium and long term trends.

-

Combining with high trading volume FILTER can avoid being misled by false breakouts.

-

Setting stop loss and take profit ratios can effectively control the risk of single trades.

-

Adopting medium and long term holding strategies is not affected by high frequency market noise and steadily profitable.

Risks and Solutions

-

High probability of being misled by high frequency false breakouts. The solution is to add transaction volume verification.

-

Medium and long term holdings increase capital occupancy. The solution is to appropriately control the position size.

-

Moving average trading strategies may lag and miss short-term opportunities. The solution is to combine other short-term signals.

-

Significant fluctuations in volatile markets can lead to large losses. The solution is to set the appropriate stop loss position.

Optimization Directions

-

Test the strengths and weaknesses of different EMA cycle parameters to find the optimal parameters.

-

Test the impact of different stop loss and take profit ratio parameters on strategy return and risk resistance.

-

Try combining other indicators such as MACD and KDJ to determine short-term opportunities.

-

Optimize capital management strategies such as position control and dynamic stop loss methods.

Summary

Overall, this strategy is a stable medium-long term holding strategy. It can effectively track major market trends and use volume indicators to filter misleading signals. At the same time, appropriate stop loss and take profit means are adopted to control the risk of single trades. It can be described as a "steady and light" trend trading work. With proper optimization, I believe it can achieve a more ideal strategy rate of return.

- 1