ボリンジャーバンドRSIインジケーターのCCI移動平均線クロス戦略

概要

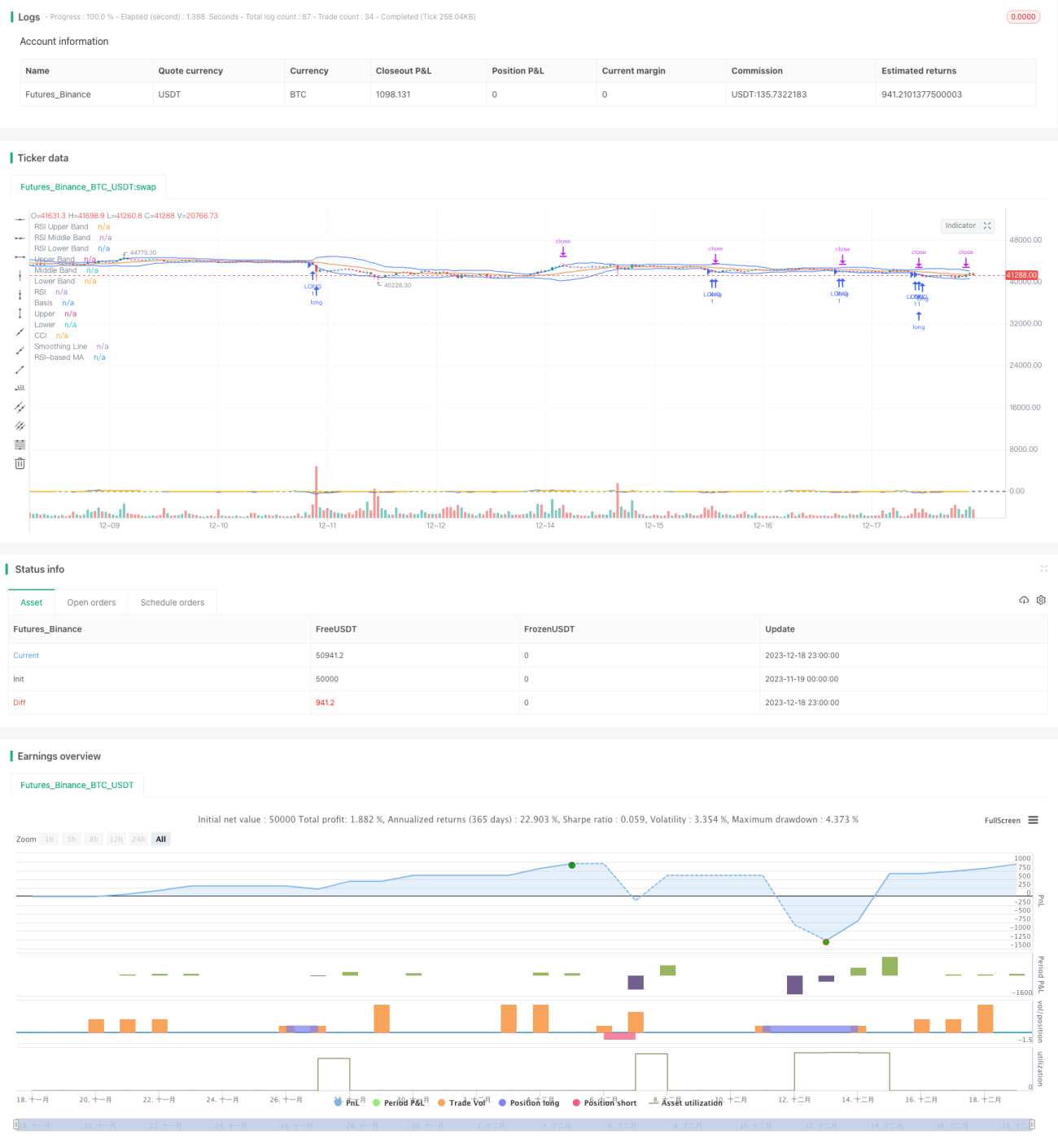

本戦略は、ボリンジャーバンド、相対力指数(RSI)、および商品チャネル指数(CCI)の3つの指標を組み合わせ、それらの交差シグナルを検出して買い・売りシグナルを発します。この戦略は、市場の買われ過ぎ・売られ過ぎの現象を見極め、反転ポイントでエントリーすることで良好な投資リターンを得ることを目的としています。

戦略原理

ボリンジャーバンド

ボリンジャーバンドは、中央線(ミドルバンド)、上限線(アッパーバンド)、下限線(ロワーバンド)で構成されます。中央線には通常20日移動平均線が使用されます。上限線と下限線は、中央線からそれぞれ標準偏差2つ分上と下の位置に設定されます。価格が下限線に近づくと売られ過ぎとみなされ、上限線に近づくと買われ過ぎとみなされます。

RSI指標

RSI指標は、一定期間における終値の上昇と下降の速度変化を反映し、買い手と売り手の力関係を測定します。RSI値が0~30のときは売られ過ぎゾーン、70~100のときは買われ過ぎゾーンとなります。RSIが買われ過ぎゾーンから下降し始めたときは売りシグナル、売られ過ぎゾーンから上昇し始めたときは買いシグナルとして捉えることができます。

CCI指標

CCI指標は、株価がその平均価格からどれだけ乖離しているかを測定します。+100は価格が平均より大幅に高く買われ過ぎ、-100は価格が平均より大幅に低く売られ過ぎを示します。CCIは価格の極端な状態を反映します。

戦略の交差シグナル

本戦略では、ボリンジャーバンドで短期的な買われ過ぎ・売られ過ぎを判断し、RSI指標で買い・売りの勢力バランスを判断し、CCI指標で価格の乖離度合いを判断します。ボリンジャーバンド、RSI、CCIの3つの指標が同時に買い/売りシグナルを示したときに、取引注文を発します。

戦略の利点

- 複数の指標を組み合わせて判断することで、誤シグナルを減少させ、シグナルの精度を向上させる

- 市場の転換点を発見し、反転トレンドの機会を捉える

- 各パラメータをカスタマイズ調整可能で、様々な市場環境に適応できる

- 移動平均線を用いてCCI指標をフィルタリングし、ノイズを低減して安定性を高める

リスクと解決策

- ボリンジャーバンド、RSI、CCIはいずれも誤シグナルを発生させる可能性があり、取引損失につながる。パラメータを適度に緩和するか、他の指標を追加して検証することで対応できる。

- CCI指標は方向感のない相場(レンジ相場)にはあまり適さないため、移動平均線やボラティリティ指標で代替することが可能。

- 取引注文はストップロスのみで、利食い(利益確定)の仕組みがない。移動利食い(トレーリングストップ)を追加して利益の一部を確定することができる。

最適化の方向性

- より多くのパラメータ組み合わせをテストし、最適なパラメータを見つける

- 機械学習アルゴリズムを追加し、パラメータをリアルタイムで最適化する

- 利食い戦略を追加し、目標利益を設定する

- MACDやKDなどの指標をさらに組み合わせ、シグナルの信頼性を判断する

まとめ

本戦略は、短期・中期・長期の市場状況を総合的に考慮し、ボリンジャーバンド、RSI、CCIの3つの指標の交差シグナルを通じて市場反転のタイミングを判断します。比較的安定した反転フォロー戦略です。パラメータ調整や利食い方法などによるさらなる最適化が可能であり、様々な市場環境に適用できます。

/*backtest

start: 2023-11-19 00:00:00

end: 2023-12-19 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy(shorttitle="BBRSIstr", title="Bollinger Bands", overlay=true)

length = input.int(20, minval=1)

maType = input.string("SMA", "Basis MA Type", options = ["SMA", "EMA", "SMMA (RMA)", "WMA", "VWMA"])- 1