概要

本戦略は、123パターン反転とスーパーオシレーターの2つの因子を組み合わせた、2因子定量反転追跡取引戦略です。基本的な考え方は、相場の反転を判断すると同時に、スーパーオシレーターの買い・売りシグナルを活用して、より正確なエントリータイミングを実現することにあります。

この戦略は主に中短期の反転取引に適しており、複数因子で確認することで、偽の反転を効果的にフィルタリングし、シグナルの質を高めることができます。

戦略の原理

-

123パターン反転

過去2日間の終値と現在の終値の大小関係を判断し、「高-高-低」または「低-低-高」のパターンを形成した場合、反転シグナルが発生する可能性があることを示します。

同時に、ストキャスティクス指標が買われすぎ・売られすぎの領域にあることを要求し、反転シグナルをさらに確認することで、偽の反転をフィルタリングします。

-

スーパーオシレーター (Awesome Oscillator)

Awesome Oscillatorは、中期と短期の移動平均線の差に基づいて構築されたモメンタム系指標です。短期線が長期線を上から下にクロスした場合が売りシグナル、下から上にクロスした場合が買いシグナルとなります。

本戦略では、この指標の買い・売り勢力の判断を用いて売買ポイントを決定します。

-

2因子確認

123パターン反転とAwesome Oscillatorの二重確認により、偽の反転を効果的にフィルタリングし、エントリータイミングの正確性を高めることができます。

戦略の利点

-

2因子で反転ポイントを確定することで、偽の反転シグナルを効果的にフィルタリングできます。

-

Awesome Oscillatorはモメンタム指標として、エントリータイミングの正確性を向上させます。

-

ストキャスティクス指標を組み込むことで、天井買いや底売りのリスクを回避できます。

-

反転戦略自体は高い勝率とリスクリワード比の利点を持っています。

戦略のリスク

-

反転失敗のリスクは依然として存在します。2因子により確率を低減できますが、完全に回避することはできません。

-

オーバー最適化のリスク。指標のパラメータ設定は、市場ごとにテスト・最適化する必要があり、過剰適合を防ぐ必要があります。

-

逆張りリスク。強いトレンド相場では、反転戦略は逆張りによる損失を生みやすくなります。ストップロスを設定してリスクをコントロールできます。

戦略の最適化方向性

-

指標パラメータの組み合わせをテスト・最適化し、パラメータのロバスト性を高める。

-

ストップロス戦略を追加し、1回あたりの損失を制御する。

-

セクター・業種の選択と組み合わせ、銘柄選定のミスを防ぐ。

-

保有期間を最適化し、過度な追跡を防止する。

-

補助条件として異なる移動平均線システムをテストする。

まとめ

以上より、本2因子定量反転追跡戦略は、一定の利益確率とリスクリワード比を確保しつつ、Awesome Oscillatorをエントリータイミングの補助ツールとして採用し、ストキャスティクス指標により天井買いを回避することで、反転取引のリスクを効果的に管理できる実用的な戦略です。

しかし、反転戦略自体のリスクも無視できません。指標パラメータの最適化やストップロス条件の設定など、リスク管理が依然として必要です。適切に運用すれば、本戦略は投資家に安定した超過リターンをもたらす可能性があります。

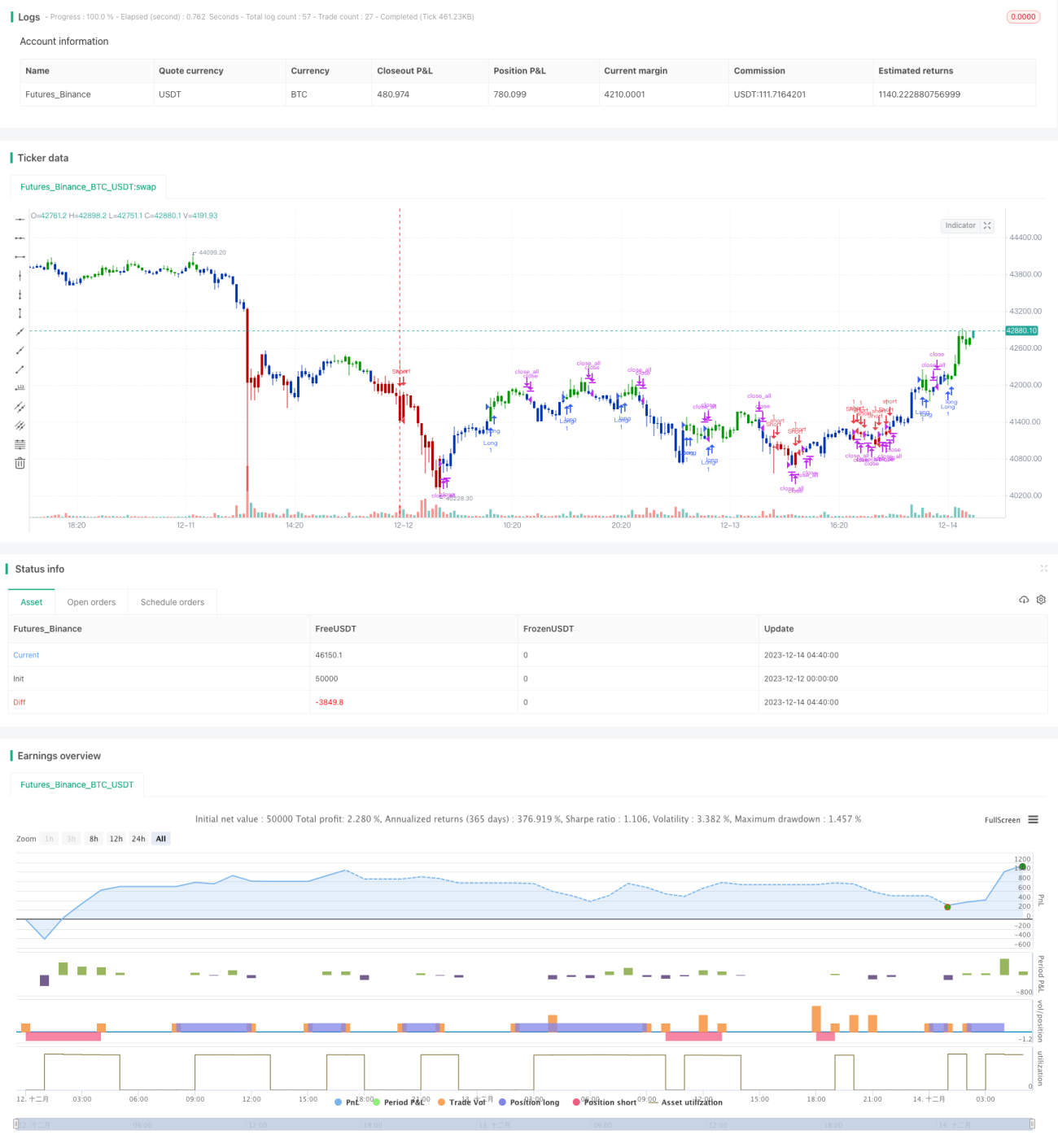

/*backtest

start: 2023-12-12 00:00:00

end: 2023-12-14 05:00:00

period: 20m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 12/08/2021

// This is combo strategies for get a cumulative signal. - 1