ダブルトラック逆MACDクオンツ取引戦略

概要

本戦略は、デュアルトラック逆MACD定量取引戦略です。ウィリアム・ブラウ(William Blau)の著書『Momentum, Direction and Divergence』で述べられたテクニカル指標を参考にし、それを拡張したものです。また、バックテスト機能を備えており、アラート、フィルター、トレーリングストップなどの追加機能も設定可能です。

戦略の原理

本戦略の中心指標はMACDです。高速移動平均線EMA(r)と低速移動平均線EMA(slowMALen)を計算し、その差xmacdを求めます。さらに、xmacdのEMA(signalLength)を計算してxMA_MACDを取得します。xmacdがxMA_MACDを上抜けたら買い、下抜けたら売りとなります。この戦略の鍵は逆張りシグナルであり、xmacdとxMA_MACDの関係が通常のMACD指標と逆であることに由来し、「逆MACD」という名称が付けられています。

また、本戦略にはトレンドフィルターが導入されています。買いシグナルが発生した際、強気トレンドフィルターが設定されていれば価格が上昇しているかどうかを検出します。同様に、売りシグナルでは価格の下落トレンドを検出します。RSI指標やMFI指標もシグナルのフィルタリングに使用できます。ストップロス機構を設定することで、閾値を超える損失を防ぐことも可能です。

優位性分析

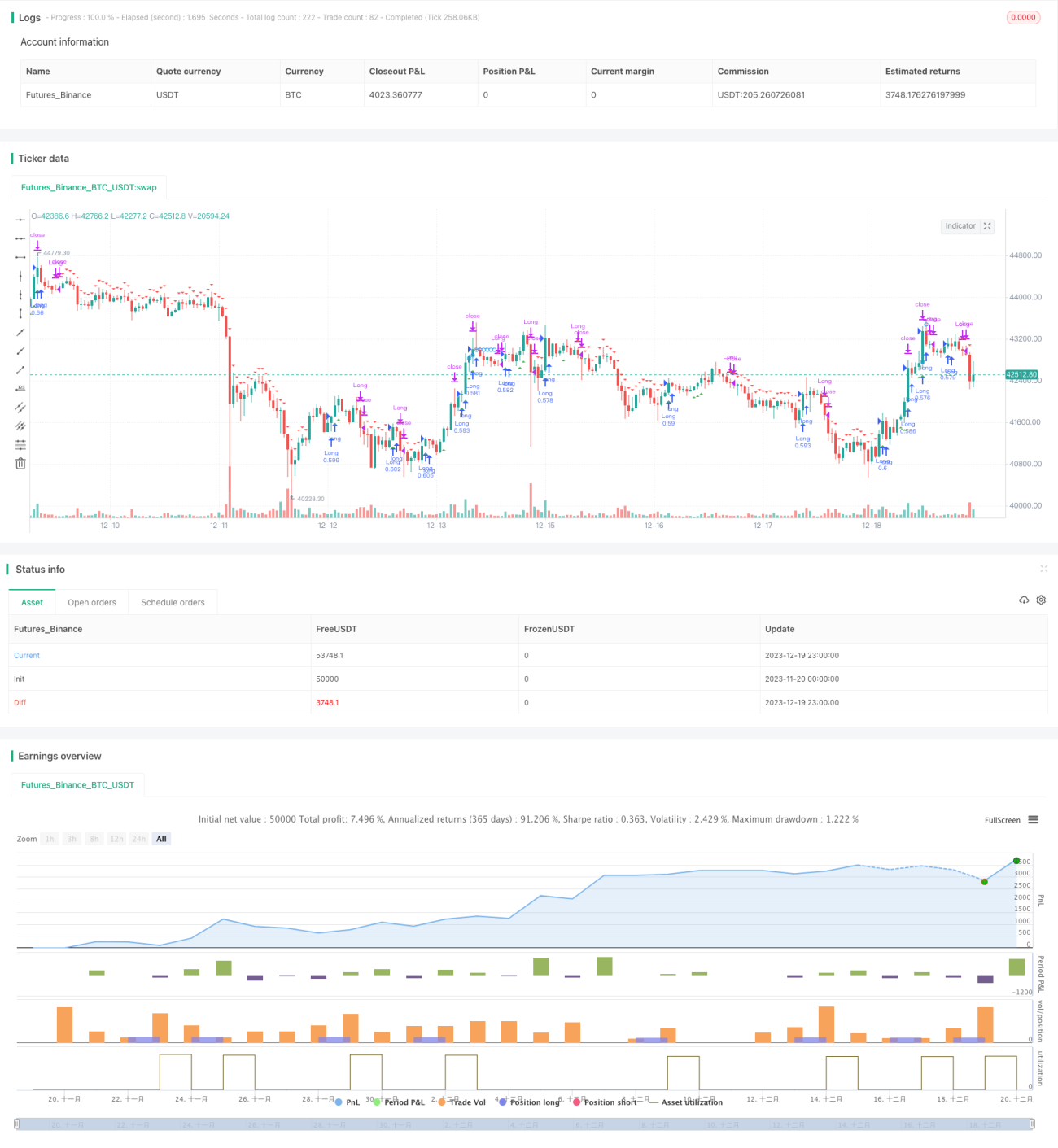

本戦略の最大の利点は、強力なバックテスト機能です。異なる取引銘柄を選択し、バックテストの期間を設定し、特定銘柄のデータに基づいて戦略を最適化できます。単純なMACD戦略と比較して、トレンドや買われ過ぎ・売られ過ぎの判断を追加し、類似したシグナルをフィルタリングできます。デュアルトラック逆MACDは従来のMACDとは異なり、従来のMACDでは見逃される可能性のある機会を捉えることができます。

リスク分析

本戦略のリスクは主に逆張りという考え方に起因します。逆張りシグナルは一定の機会を得られる一方で、従来のMACDの売買ポイントを放棄することになるため、慎重な評価が必要です。また、MACD自体がもともとダマシのシグナルを発生しやすいという問題があります。もみ合い相場に遭遇した場合、本戦略は過剰な取引を発生させ、取引コストやスリッページ損失を増加させる可能性があります。

リスクを軽減するためには、パラメータを適切に調整し、移動平均線の期間を最適化すること、トレンドや指標フィルターを組み合わせてもみ合い相場でのシグナル発生を避けること、ストップロスの距離を適度に広げて個別の取引損失を制御することが考えられます。

最適化の方向性

本戦略は以下の点から最適化が可能です:

- 高速・低速のトラックパラメータを調整し、移動平均線の期間を最適化して、特定の銘柄データでテストし、最適なパラメータの組み合わせを見つける。

- トレンドフィルターを追加または調整し、バックテスト結果に基づいて戦略の収益率が向上するか判断する。

- 異なるストップロスメカニズム(固定ストップロスとトレーリングストップのどちらが良いか)をテストする。

- KD、ボリンジャーバンドなどの他の指標を組み合わせ、追加のフィルター条件を設定してシグナルの品質を確保する。

まとめ

デュアルトラック逆MACD定量戦略は、古典的なMACD指標の考え方を参考にし、それを拡張・改良したものです。本戦略は柔軟なパラメータ構成、豊富なフィルター機構の選択肢、そして強力なバックテスト機能といった利点を備えています。これにより、異なる取引銘柄に応じて個別に最適化できるため、有望な定量取引戦略として検討する価値があります。

/*backtest

start: 2023-11-20 00:00:00

end: 2023-12-20 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version = 3

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 09/12/2016

// This is one of the techniques described by William Blau in his book- 1