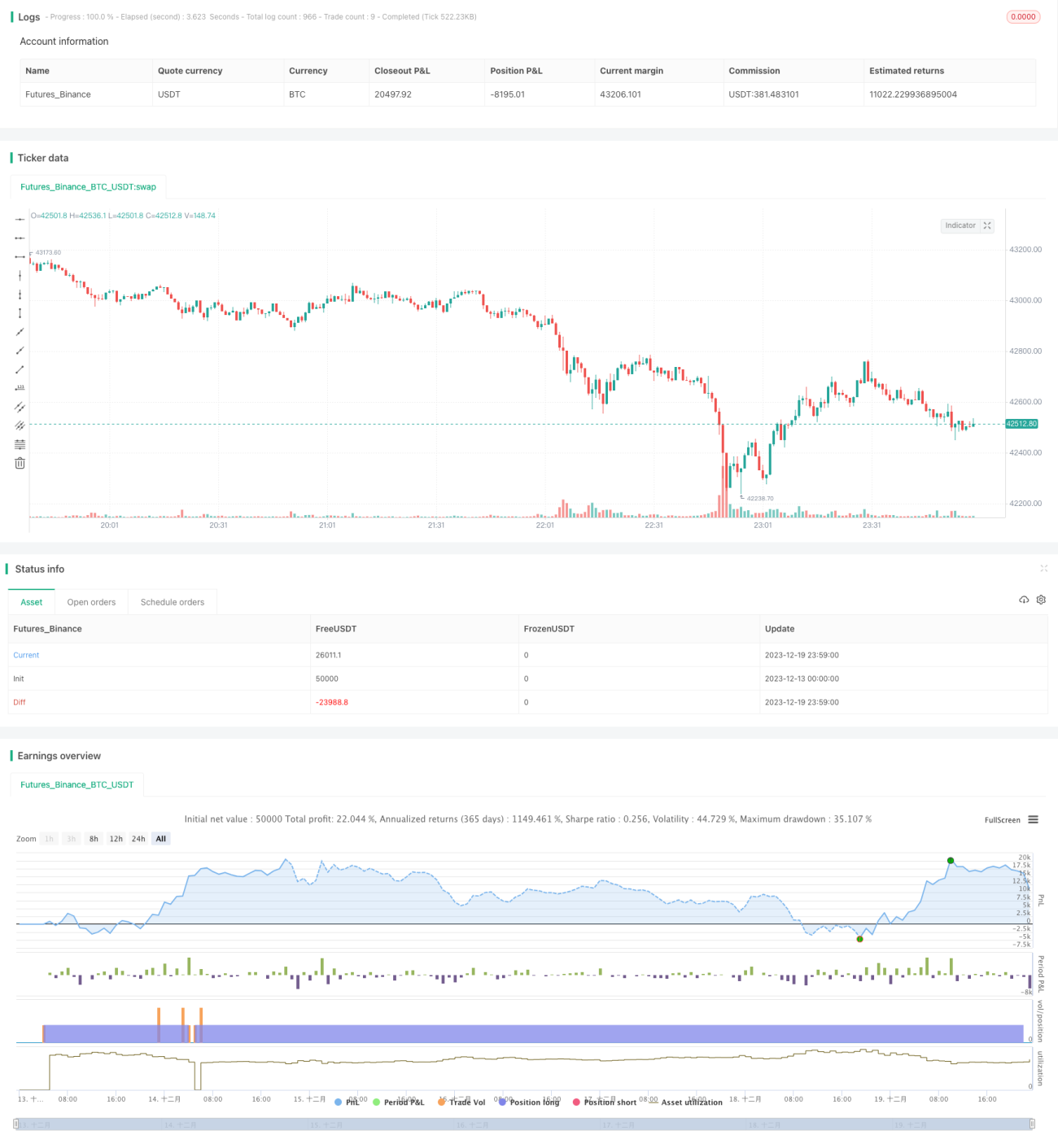

移動平均線の回転反転戦略

本戦略は「移動平均線に基づく平均回帰反転戦略」(Mean Reversion Reverse Strategy Based on Moving Average)と命名され、その主な考え方は、重要な移動平均線を下回った後に買い入れ、事前に設定した目標利益に達したら利益確定を行うことです。

本戦略の基本原理は、短期移動平均線の反転を利用して、レンジ相場におけるリバウンドの機会を捉えることです。具体的には、価格が長期の移動平均線(例えば20日線、50日線など)を下回った後、強い売られ過ぎの兆候を示す場合、市場変動の平均回帰(mean reversion)特性により、価格はある程度のリバウンドを生じる傾向があります。この時、短期の移動平均線(例えば10日線)が上向きに反転するシグナルを発すれば、良い買い入れタイミングとなります。本戦略では、終値が20日線を下回りながら50日線を上回っている場合に買い入れ、短期反転を利用してリバウンド相場を捉えます。

本戦略の具体的な買い入れロジックは以下の通りです。価格が20日線を下回ったら1枚買い、50日線を下回ったら1枚追加、100日線を下回ったらさらに1枚追加、200日線を下回った場合も最大1枚追加で、合計4枚の買い建てを行います。事前に設定した利益確定目標に達したらポジションを決済します。また、時間条件とストップロス条件も設定されています。

優位性分析

- 移動平均線の反転特性を活用することで、短期リバウンドの機会を効果的に識別可能

- 分割建玉により、単一ポイントのリスクを低減

- 利益確定条件を設定することで、利益を確定できる

- 始値と前回安値をフィルターとして使用し、偽のブレイクアウトを回避

リスク分析

- 長期保有時には、逆転リスクに直面する可能性がある。相場がさらに下落すると損失が拡大する

- 移動平均線のシグナルが誤報となる可能性があり、損失につながる可能性がある

- 設定した利益確定目標に到達せず、全額または一部の利益確定ができない可能性がある

最適化の方向性

- 異なるパラメータ設定における収益率と安定性をテスト可能

- MACDやKDなどの他の指標と組み合わせて買い入れを判断することを検討可能

- 各銘柄の特性に応じて、取引スタイルに適した移動平均線の周期を選択可能

- 機械学習アルゴリズムを導入してパラメータを動的に最適化することも可能

まとめ

本戦略は全体的に、古典的かつ汎用的な移動平均線取引戦略である。移動平均線の平滑化特性を正しく活用し、複数の移動平均線を組み合わせて短期買い入れタイミングを識別している。分割建玉と迅速な利益確定によりリスクを管理している。ただし、重要な政策ニュースなどの市場における突発的な事象への対応は受動的になりがちであり、これは今後の改善点である。全体的には、パラメータ最適化とリスク管理を適切に改良することで、安定した超過収益を得ることが可能な戦略である。

- 1