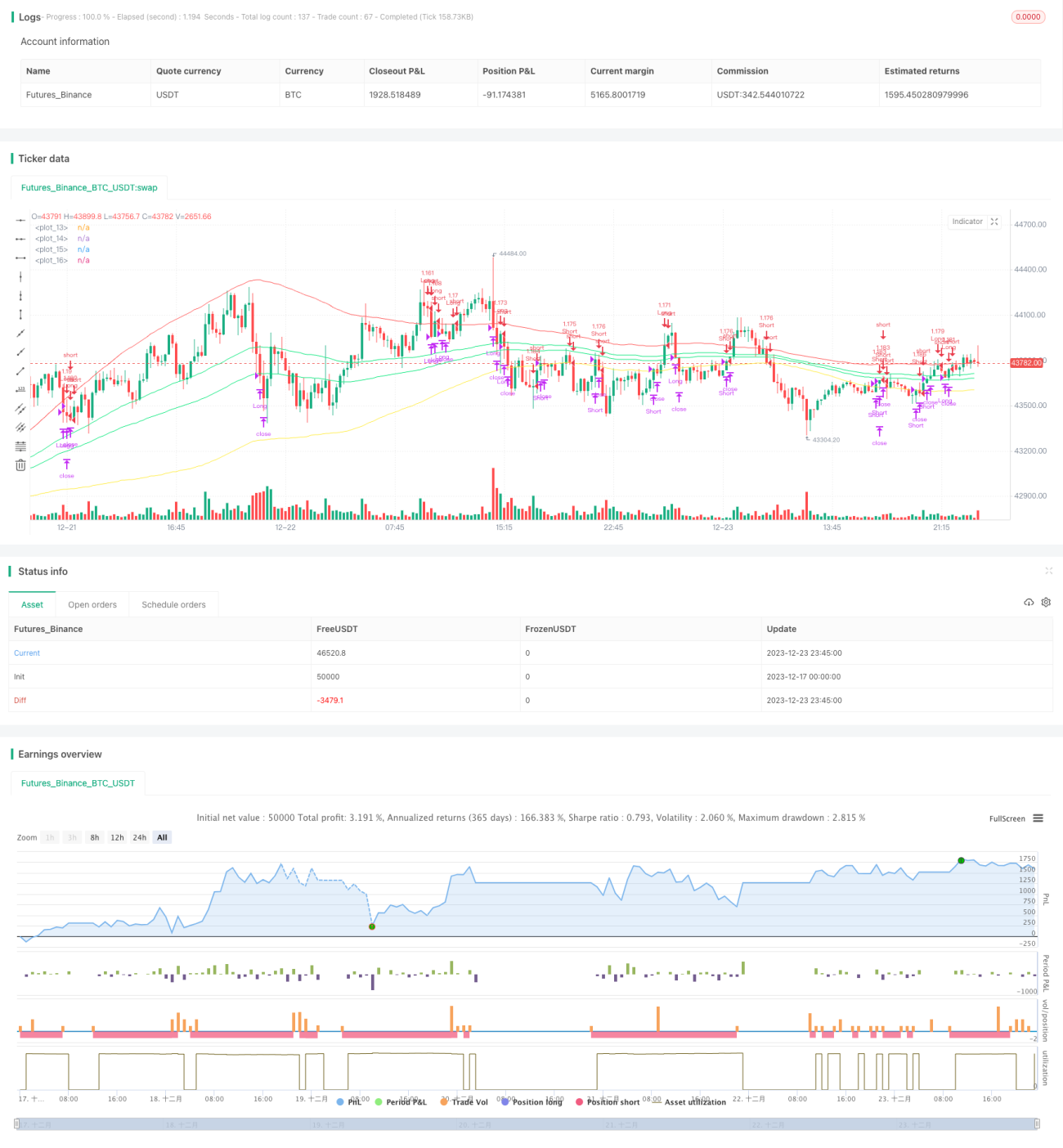

ダブルボラティリティバンドブレイクアウト戦略

1

Follow

1802

Followers

概要

二重波動帯突破戦略はトレンドフォロー戦略の一種です。波動帯の上下バンドを利用して価格トレンドを判断し、内部波動帯を上抜けた時にロングポジションを構築し、外部波動帯を下抜けた時にポジションをクローズします。

戦略の原理

本戦略はまず、指定期間内の移動平均線と標準偏差を計算し、標準偏差の数値を調整することで二重波動帯を構築します。内部波動帯は移動平均線に標準偏差1つを加減したもので構成され、外部波動帯は移動平均線に標準偏差1.5個を加減したものです。

価格が内部の上部バンドを突破した場合、相場が強気に転じたと判断してロングします。逆に価格が内部の下部バンドを割り込んだ場合、相場が弱気に転じたと判断してショートします。

ロング後の利益確定退出条件は、価格が外部の下部バンドを下抜けることです。ショート後の利益確定退出条件は、価格が外部の上部バンドを上抜けることです。

本戦略では、利益確定、ストップロス、トレーリングストップなどの退出メカニズムも同時に設定しています。

優位性分析

二重波動帯突破戦略には以下の優位性があります。

- 二重波動帯で価格の動きを判断することで、トレンドを効果的に追従できます。

- 内部波動帯の突破時にポジションを構築するため、不要な逆張り取引を回避できます。

- 利益確定、ストップロス、トレーリングストップを設定することで、リスクを効果的にコントロールできます。

- パラメータが調整可能なため、異なる銘柄に合わせて最適化できます。

リスク分析

二重波動帯突破戦略には以下のリスクも存在します。

- 相場がレンジ相場の場合、頻繁なポジション構築とストップロスが発生する可能性があります。

- パラメータ設定が不適切だと、容易にポジションが構築されたり、利益確定が難しくなったりする可能性があります。

- ブレイクアウトには偽のシグナルが含まれる場合があり、ダマシのブレイクアウトが発生するリスクがあります。

これらのリスクに対しては、パラメータを適切に調整したり、他の指標でフィルタリングを行ったり、手動でブレイクアウトの効果を監視することでリスクを低減できます。

最適化の方向性

二重波動帯突破戦略は以下の観点から最適化が可能です。

- 移動平均線と標準偏差のパラメータを最適化し、波動帯を異なる銘柄の特性に合わせる。

- 出来高やMACDなどの指標を追加してフィルタリングし、偽のブレイクアウトを回避する。

- 機械学習手法を用いて動的にパラメータを最適化する。

- 高頻度の時間枠で戦略を複製し、利益獲得の幅を拡大する。

まとめ

二重波動帯突破戦略は、価格の波動帯に対する相対的な位置変化を判断して取引シグナルを生成する、典型的なトレンドフォロー戦略です。本戦略は二重波動帯を利用して利益獲得領域を設定し、科学的な退出メカニズムを設定してリスクをコントロールします。パラメータの最適化とリスク管理が適切に行われれば、良好な結果を得ることができます。

Source

Pine

/*backtest

start: 2023-12-17 00:00:00

end: 2023-12-24 00:00:00

period: 15m

basePeriod: 5m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

strategy("BB Strat",default_qty_type = strategy.percent_of_equity, default_qty_value = 100,currency="USD",initial_capital=100, overlay=true)

l=input(title="length",defval=100)

pbin=input(type=float,step=.1,defval=.25)Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1