二重トレンドフィルターチェーン移動平均線比率戦略

1

Follow

1802

Followers

概要

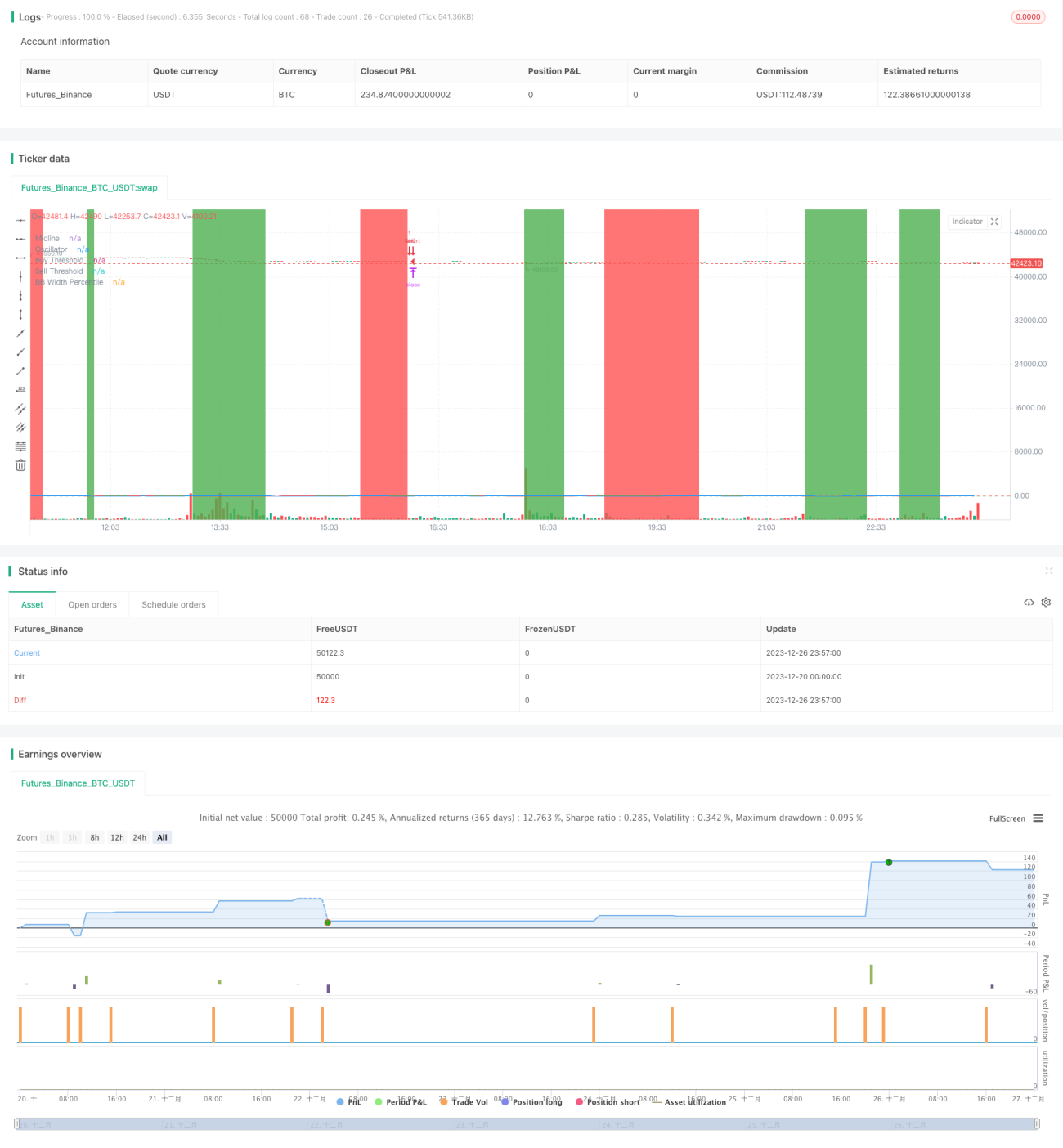

本戦略は、二重移動平均線比率指標にボリンジャーバンドフィルターと二重トレンドフィルター指標を組み合わせ、チェーン式エグジットメカニズムを採用したトレンドフォロー戦略です。この戦略は、移動平均線比率指標を利用して中長期的なトレンド方向を識別し、トレンド方向が明確な場合に有利なエントリーポイントを選び、利確・損切りのエグジットメカニズムを設定して利益を確定し、損失を抑えることを目的としています。

戦略の原理

- 短期移動平均線(10日線)と長期移動平均線(50日線)を計算し、その比率を「価格移動平均線比率」とします。この比率は、価格の中長期的なトレンド変化を効果的に識別できます。

- 価格移動平均線比率をパーセンタイルに変換します。これは、過去一定期間における現在の比率の相対的な強弱を示します。このパーセンタイルをオシレーターと定義します。

- オシレーターが設定された買い閾値(10)を上抜けたときに買いシグナル、売り閾値(90)を下抜けたときに売りシグナルを発生させ、トレンドフォローを行います。

- ボリンジャーバンド幅指標を組み合わせて取引シグナルをフィルタリングし、バンドが収縮したときに取引を実行します。

- 二重トレンドフィルター指標を採用し、価格が上昇トレンドチャネルにある場合のみ買いシグナル、下降チャネルにある場合のみ売りシグナルを発生させることで、逆張り取引を回避します。

- チェーン式エグジットメカニズムを設定します。利確、損切り、および組み合わせエグジットを含み、複数のエグジット条件を事前設定し、最も利益の大きい条件を優先的にエグジットします。

戦略の優位性

- 二重トレンドフィルターメカニズムにより、主トレンド方向を確実に判断し、逆張り取引を回避できます。

- 移動平均線比率指標は、単一の移動平均線よりもトレンド変化を効果的に判断できます。

- ボリンジャーバンド幅指標は、市場の低ボラティリティ期を効果的に特定でき、この時期の取引シグナルはより信頼性が高まります。

- チェーン式エグジットメカニズムにより、利益が安定し、総利益を最大化できます。

リスクと解決方法

- レンジ相場で明確なトレンドがない場合、誤ったシグナルや反転が多発する可能性があります。解決方法は、ボリンジャーバンド幅フィルターを併用し、バンドが収縮したときのみ取引することです。

- 明らかなトレンド反転が発生した場合、移動平均線にはラグが生じ、反転シグナルを即座に判断できません。解決方法は、移動平均線の期間パラメータを適切に短縮することです。

- 相場でギャップが発生した場合、損切りポイントが瞬間的にヒットし、大きな損失が発生する可能性があります。解決方法は、損切りパラメータを適切に緩和することです。

戦略の最適化方向

- パラメータ最適化。移動平均線の期間、オシレーターの売買ポイント、ボリンジャーバンドのパラメータ、トレンドフィルターパラメータについて総当たりテストを行い、最適なパラメータ組み合わせを探します。

- 他の指標の組み込み。KD指標やMACD指標など、トレンド反転を判断する他の指標を追加することで、戦略の精度を向上させることができます。

- 機械学習。過去のデータを収集し、機械学習アルゴリズムを用いてモデルを訓練し、各パラメータを動的に最適化することで、パラメータの適応的調整を実現します。

まとめ

本戦略は、二重移動平均線比率指標とボリンジャーバンド指標を総合的に活用して中長期的なトレンド方向を判断し、トレンドを確認した後に最適なエントリーポイントを探してエントリーし、チェーン式エグジットメカニズムで利益を確定するため、信頼性が高く、効果も顕著です。この戦略は、パラメータ最適化、他の補助判断指標の追加、機械学習を通じてさらなる改良と利益率向上が期待できます。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1