1

Follow

1802

Followers

概要

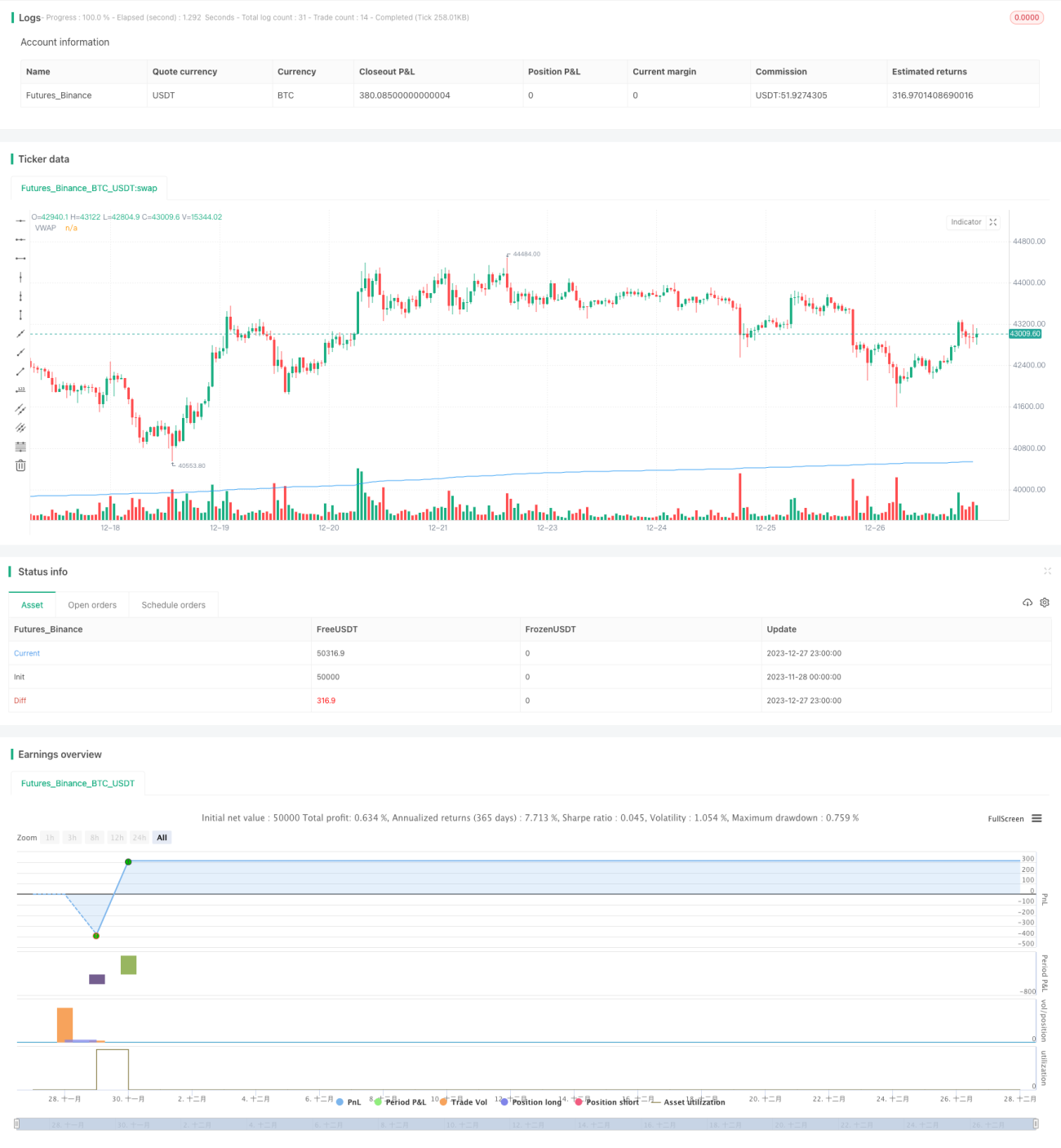

出来高加重平均価格(VWAP)戦略は、特定の期間における株式の平均価格を追跡する戦略です。この戦略はVWAPをベンチマークとして使用し、価格がVWAPを上回った場合や下回った場合にロングまたはショートのポジションを建てます。また、取引管理のためにストップロスと利益確定の条件を設定します。

戦略の原理

この戦略では、まず典型価格(高値、安値、終値の平均)と出来高の積の合計、および出来高の合計を計算します。次に積の合計を出来高の合計で割り、VWAP値を算出します。価格がVWAPを上抜けた場合にロング、下抜けた場合にショートのポジションを取ります。

ロングポジションの利益確定条件は、価格がエントリー価格より3%上昇した場合に利益確定、ストップロス条件は価格がエントリー価格より1%下落した場合に損失を確定することです。ショートポジションも同様の条件です。

優位性分析

VWAP戦略の主な優位性は以下の通りです。

- VWAPという広く認められた重要な統計指標を取引シグナルのベースとして使用することで、戦略の有効性が高まります。

- VWAPシグナルとストップロス・利益確定を併用することで、トレンドで利益を得ると同時に損失を抑えることができます。

- 戦略ロジックがシンプルで明確であり、理解と実装が容易です。

リスク分析

本戦略には以下のリスクも存在します。

- VWAPは将来の価格を予測できないため、VWAPシグナルに遅れが生じる可能性があります。

- ストップロス条件が緩すぎる場合、損失が拡大する恐れがあります。

- バックテストの期間が長いほど取引シグナルが多くなり、実運用での結果に差異が生じる可能性があります。

これらのリスクは、パラメータの調整やストップロスアルゴリズムの最適化などによって低減できます。

最適化の方向性

本戦略は以下の方向性で最適化が可能です。

- VWAPのパラメータを最適化し、最適な計算期間を特定する。

- 移動ストップロスや指数移動ストップロスなど、他のトレーリングストップロスアルゴリズムをテストする。

- VWAPシグナルの誤りを回避するために、出来高インジケーターやボリンジャーバンドなど、他の指標をフィルターとして組み合わせる。

まとめ

総じて、出来高加重平均価格戦略はVWAPという重要指標の予測力を活用し、ストップロスと利益確定条件を設定することで、長期的な正のリターンを得ることができます。しかし、市場変動によるリスクを低減し、戦略の収益性を高めるためには、さらなる最適化や他の戦略との組み合わせが必要です。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1