概要

ダブルトレンドトラッキング戦略は、二つの指標を同時に組み合わせてトレンドを判断する定量取引戦略です。この戦略はまず123反転指標を使用して価格の反転シグナルを判断し、その後方向性トレンド指標(DTI)を組み合わせて価格のトレンド方向を判断することで、売買シグナルを二重確認します。

戦略の原理

この戦略は主に二つの部分から構成されています。

-

123反転指標

123反転指標の判断原理は次のとおりです。

- 終値が2日連続で上昇し、かつ9日スローKラインが50未満の場合に買い;

- 終値が2日連続で下落し、かつ9日ファストKラインが50を超える場合に売り。

これにより、価格反転のタイミングを捉えることができます。

-

方向性トレンド指標(DTI)

DTI指標の判断原理は、一定期間の価格変動の絶対値の移動平均を計算し、それを価格の平均変動幅で割るものです。

- DTIが買われすぎラインを上回る場合、現在は下落トレンドであることを示します;

- DTIが売られすぎラインを下回る場合、現在は上昇トレンドであることを示します。

-

両者の組み合わせ

まず123反転指標を使用して価格に反転シグナルが発生したかどうかを判断します。その後、DTI指標を組み合わせて反転後の価格の全体的なトレンド方向を判断します。

これにより、単純な反転シグナルだけに依存することで生じる偽反転問題を回避し、戦略の安定性と収益性を向上させることができます。

戦略の強み

-

二重指標による確認で、偽反転に伴うリスクを回避

-

反転とトレンド判断を組み合わせ、操作の柔軟性と安定性を両立

-

パラメータ最適化の余地が大きく、異なる銘柄に合わせて柔軟に調整可能

リスク分析

-

DTIパラメータの設定には経験が必要であり、不適切な設定はトレンド方向を誤判定する可能性がある

-

反転が必ずしも新しいトレンドの形成を意味するわけではなく、レンジ相場が発生する可能性がある

-

有効なストップロスが必要であり、1回の損失を抑制する必要がある

解決策:パラメータ最適化テスト+適切なストップロス+他の指標との組み合わせ

戦略の最適化方向性

-

DTIパラメータをテストし、最適なパラメータの組み合わせを見つける

-

他の指標と組み合わせて偽反転シグナルをフィルタリングする

-

ストップロス戦略を最適化し、最適なストップロスポイントを見つける

まとめ

ダブルトレンドトラッキング戦略は、123反転とDTIの二重指標確認により、価格反転の実質性を効果的に判断し、新しいトレンド方向を捉えることで、戦略の収益確率を高めることができます。ただし、パラメータ設定やストップロス戦略は継続的にテストと最適化を行い、戦略の収益余地を最大化する必要があります。総じて、この戦略はトレンド取引と反転取引の利点を組み合わせた、推奨に値する定量戦略です。

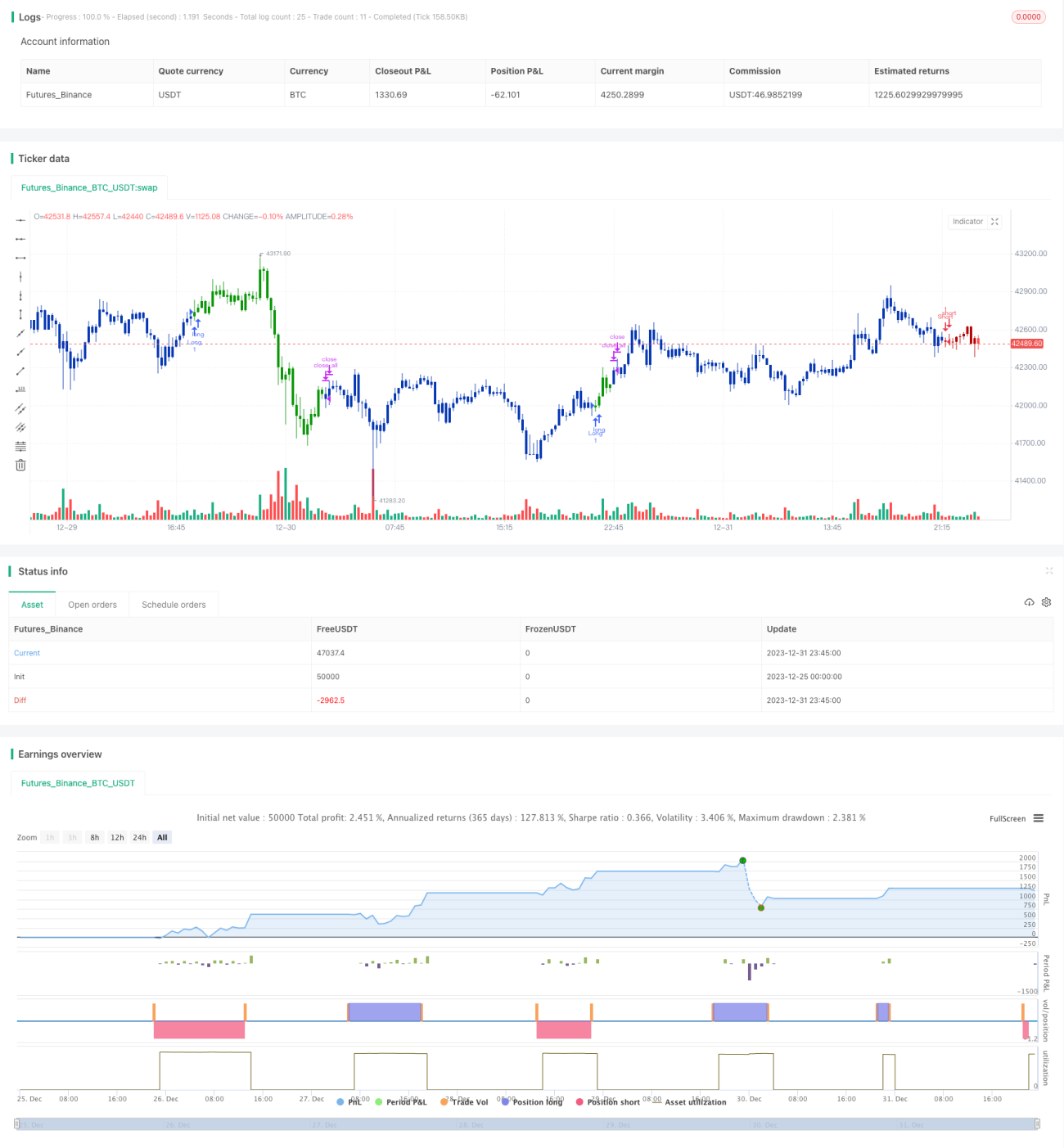

/*backtest

start: 2023-12-25 00:00:00

end: 2024-01-01 00:00:00

period: 15m

basePeriod: 5m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 19/02/2020

// This is combo strategies for get a cumulative signal. - 1