有意義な足(バー)フィルターに基づくブレイクアウト累積戦略

概要

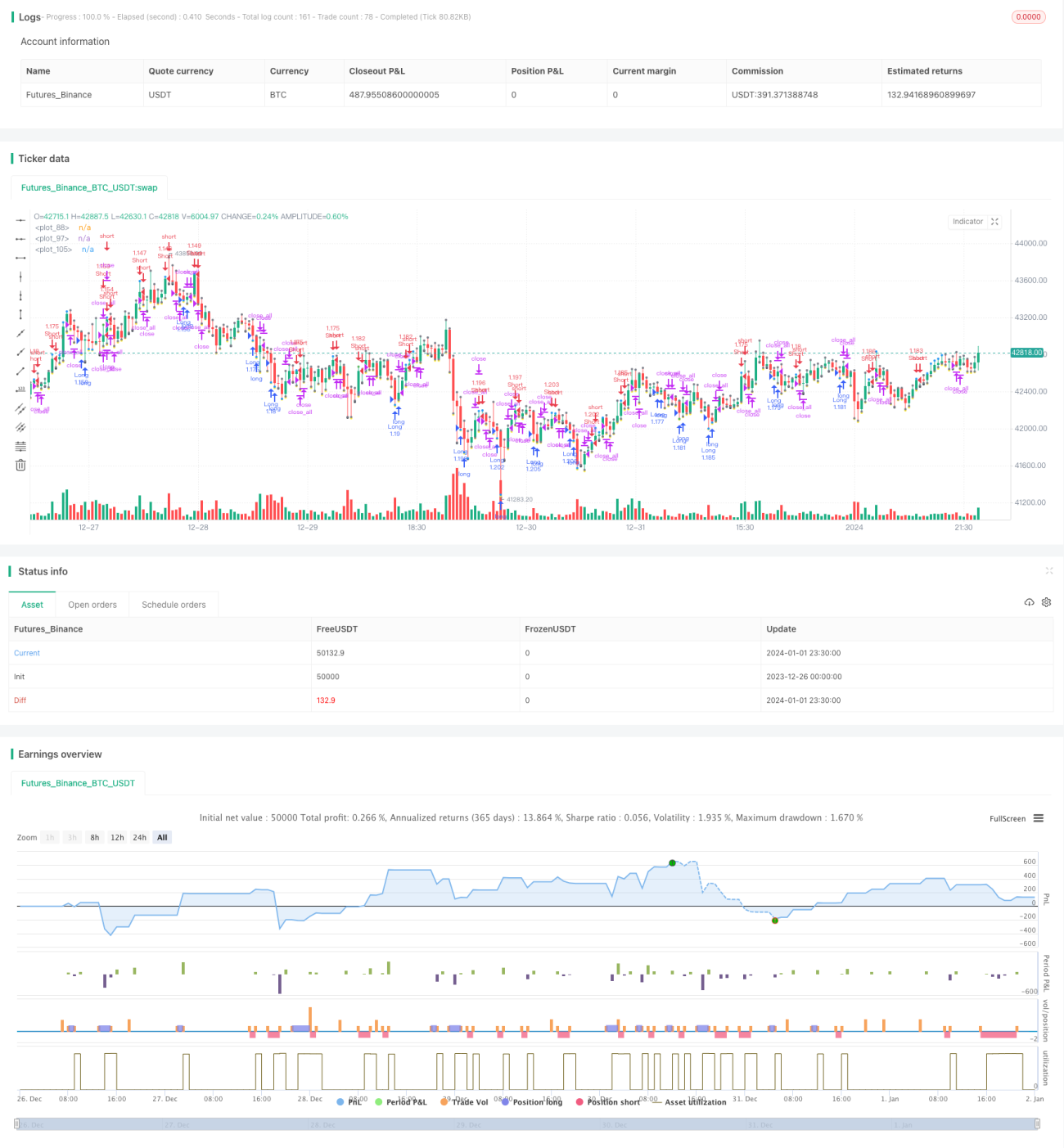

本戦略は、ローソク足の「有意義な柱線」を判断してトレンドを予測し、ブレイクアウトシグナルと組み合わせて取引シグナルを発します。戦略は小さすぎるローソク足を除外し、有意義な柱線のみを分析するため、頻繁な小さな変動によるノイズを避け、より安定した信頼性の高いシグナルを得ることができます。

戦略の原理

-

現在のローソク足の実体の長さ(body)を計算し、過去6本のローソク足のbodyの平均値の3倍を超えた場合、「有意義な柱線」とみなします。

-

連続して3本の有意義な柱線がすべて陽線である場合、強気シグナルと判断します。連続して3本の有意義な柱線がすべて陰線である場合、弱気シグナルと判断します。

-

シグナルを判断すると同時に、価格が以前の高値または安値を突破した場合にも追加の取引シグナルが発生します。

-

SMA移動平均線をフィルターとして使用し、価格がSMAを突破した場合のみポジションを保有します。

-

ポジション保有後、価格が再度エントリーポイントまたはSMA移動平均線を突破した場合、ポジションをクローズします。

優位性分析

-

「有意義な柱線」を使用してトレンドを判断することで、不要なノイズを大幅に除去し、シグナルを明確にします。

-

トレンドシグナルとブレイクアウトシグナルを組み合わせることで、シグナルの品質を向上させ、誤シグナルを減少させます。

-

SMA移動平均線によるフィルターは、高値掴みや安値売りを回避するのに役立ちます。SMA以下で買い、SMA以上で売ることで、シグナルの信頼性が高まります。

-

損切り・利確条件を設定することで、適時に損失を抑え利益を確保し、資金保全に寄与します。

リスク分析

-

本戦略はやや積極的で、3本のローソク足でシグナルを判断するため、短期的なレンジ相場をトレンド反転と誤認する可能性があります。

-

テストデータが十分でないため、異なる銘柄や時間足では効果に差が生じる可能性があります。

-

夜間や翌日へのポジション持ち越しに関する制御が組み込まれていないため、持ち越しリスクが存在します。

最適化の方向性

-

「有意義な柱線」のパラメータ(判断に使用するローソク足の本数や「有意義」の定義など)をさらに最適化できます。

-

異なる時間足のパラメータが結果に与える影響をテストし、最適な時間足を探求できます。

-

ATRを使用した損切りを追加してリスクを制御できます。

-

夜間のポジション持ち越し制御ロジックを追加することも検討できます。

まとめ

本戦略は、「有意義な柱線」によるフィルタリングとトレンド判断、ブレイクアウトを組み合わせて取引シグナルを生成することで、不要な小幅な変動を効果的に除去し、シグナルをより明確かつ信頼性の高いものにします。ただし、判断期間が短いため、誤判断のリスクが存在する可能性があります。パラメータ最適化やリスク管理手段を用いて、さらに改善することができます。

- 1