ボリンジャーバンドとVWAPに基づく定量取引戦略

概要

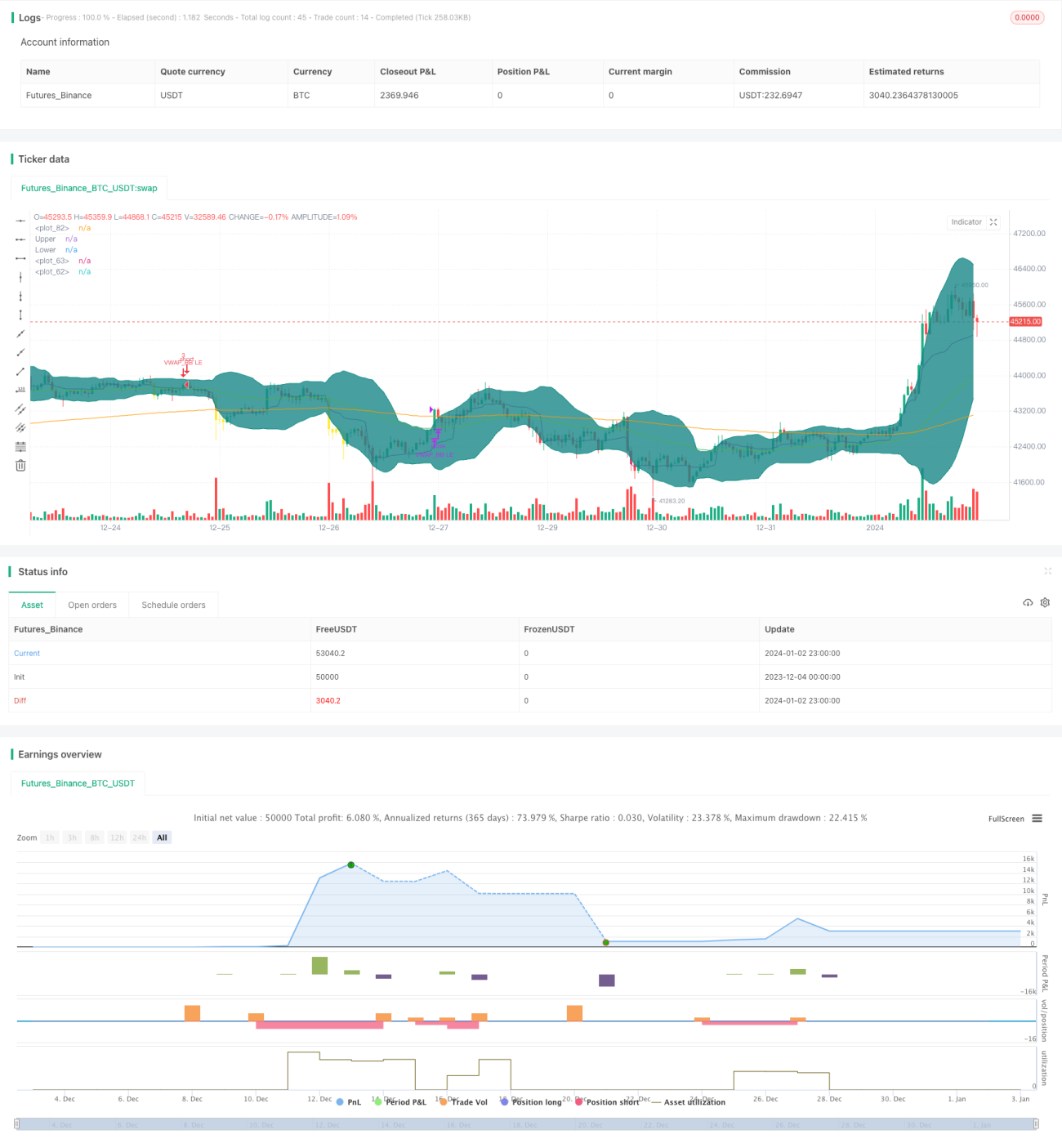

本戦略は、ボリンジャーバンド(BB)と代表価格量移動平均線(VWAP)の2つの指標を組み合わせて、売買シグナルを生成します。短期的な価格異常を発見してトレードを行うため、短期売買に適しています。

戦略の原理

本戦略は、以下のルールに基づいて売買を行います。

買い条件:

- 短期EMAが長期EMAを上回っていることをトレンドの前提条件とする。

- 終値がVWAPを上回っている場合、価格上昇と判断して買い。

- 過去10本のローソク足のうち、1本でも終値がボリンジャーバンドの下限を下回っている場合、価格異常と判断して買い。

売り条件:

- 終値がボリンジャーバンドの上限を上回った場合、価格が反転したと判断して売り。

具体的には、まず50日EMAが200日EMAを上回っているかを確認し、短期・長期EMAで大局的なトレンドを判断します。次にVWAPを用いて、価格が短期的に上昇トレンドにあるかを判断します。最後にボリンジャーバンドを使って、価格が短期的に異常な下落を起こしたかをエントリーの機会として捉えます。

エグジットルールは比較的シンプルで、価格がボリンジャーバンドの上限を上回った時点で反転が発生したと判断してポジションをクローズします。

優位性の分析

本戦略は複数の指標を組み合わせて価格の異常を判断するため、エントリーシグナルの有効性を高めることができます。EMAを使用して大局的なトレンドを判断することで、逆張りを回避できます。VWAPを組み合わせることで、短期的な価格上昇の機会を捉えることが可能です。ボリンジャーバンドを利用して価格異常を判断することで、短期売買のタイミングを正確に見極められます。

リスク分析

- EMAによる大トレンドの判断が不正確な場合、逆張りとなり大きな損失を被る可能性がある。

- VWAPは時間足や日中データに適用するのが最も効果的であり、日足データに使用すると効果が低下する。

- ボリンジャーバンドのパラメータ設定が不適切で、上下のバンドが広すぎたり狭すぎたりすると、シグナルを見逃す可能性がある。

これらのリスクに対しては、EMAの期間パラメータを適宜調整するか、他の大トレンド判断指標を試すことができます。VWAPパラメータは日中データに適用するか、他の短期指標に変更することも検討します。ボリンジャーバンドのパラメータを調整して最適な幅を探します。

最適化の方向性

- 大トレンドを判断するためにMACDなど他の指標を試す。

- EMAとボリンジャーバンドのパラメータを最適化し、最適な設定を見つける。

- ストップロス機構を追加する。

- 他の指標を組み合わせて偽のシグナルをフィルタリングする。

- 異なる銘柄や時間足のデータでテストを行う。

まとめ

本戦略はボリンジャーバンドとVWAPの2つの指標を組み合わせ、短期的な価格異常をエントリーのタイミングとして判断します。EMAを使用して大局的なトレンドを判断することで逆張りを回避し、短期的な価格トレンドの機会を素早く発見できます。日内取引や短期売買に適しています。パラメータの最適化や、より多くの判断指標を追加することで、戦略の安定性と収益性をさらに向上させることができます。

- 1