動的平均コスト定期積立複利戦略

概要

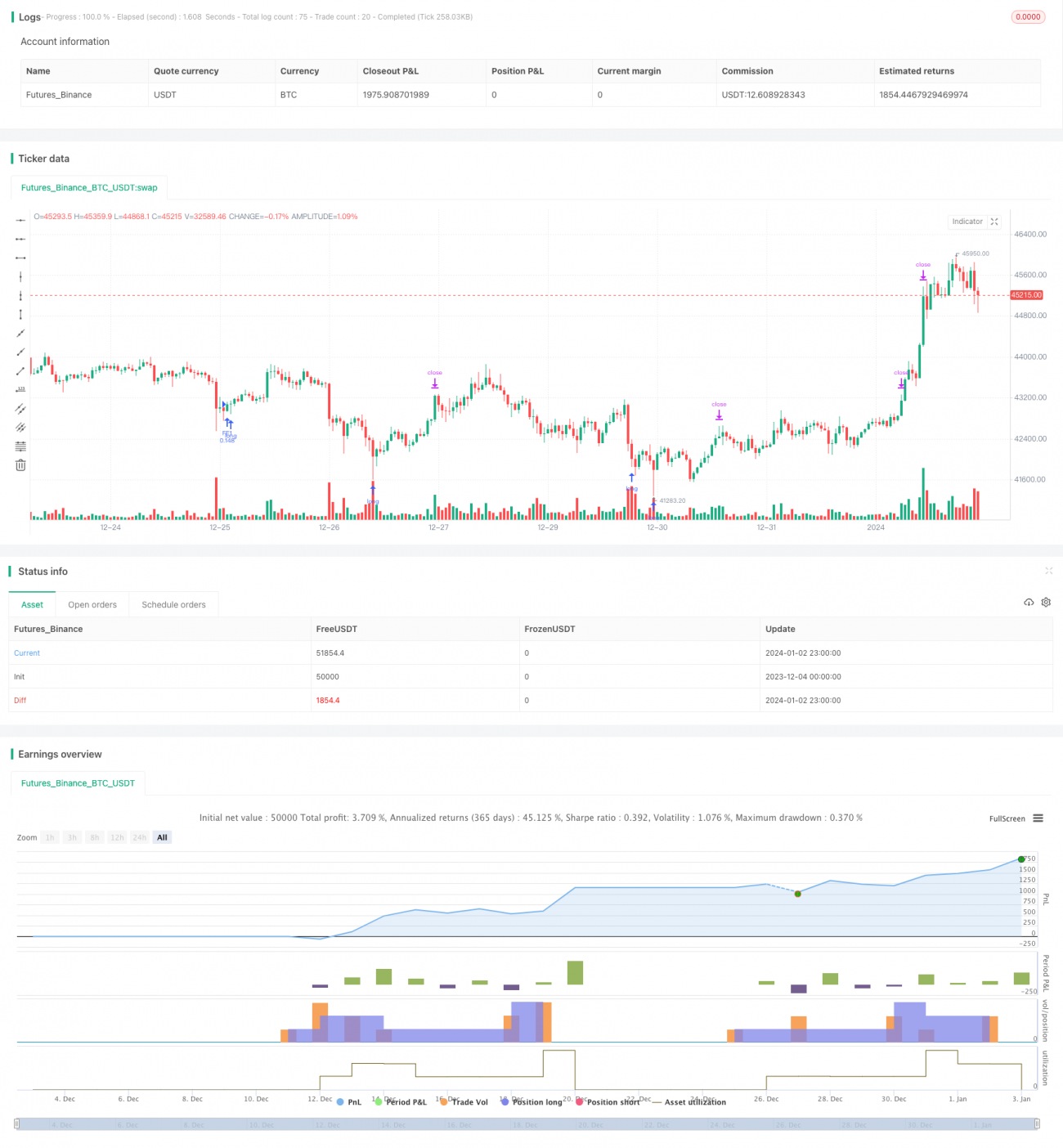

動的平均コストドルコスト平均法複利戦略は、各ポジションを開く数量を動的に調整し、トレンドの初期段階では少量のポジションを建て、レンジ相場の深まりに応じて徐々にポジションを増やしていきます。本戦略は指数関数を用いて各レベルのストップロス価格を計算し、トリガーされると再度分割で新規ポジションを建てることで、保有コストラインを指数関数的に下げることができます。深さが増すにつれてポジションコストは徐々に下方に圧縮され、価格が反転した後、分割で利確してより大きな利益を得ます。

戦略の原理

本戦略は、簡易なRSIの売られすぎシグナルと移動平均線によるタイミング選択を組み合わせて、ポジションを開くタイミングを決定します。RSIが売られすぎラインを下回り、かつ終値が移動平均線より小さい場合に初回ポジションのシグナルが発生します。初回ポジションを開いた後、指数関数に従って価格が下落する下限値を計算し、DCAシグナルを生成します。DCAのたびに、各ポジションの数量が等しくなるように保有量を調整します。保有量と保有コストが動的に変化するため、これはレバレッジ効果のような働きをします。

DCA回数が増えるにつれて保有コストは低下し続けるため、ごく小さな反発で収益を達成できます。連続して複数のポジションを開いた後、平均価格の上方にストップロスラインを描画します。価格が再び上昇して保有平均価格およびストップロスラインを超えると、ストップロスでポジションを決済します。

本戦略の最大の利点は、保有コストが低下し続けるため、レンジ相場でも徐々にコストを削減できることです。トレンドが反転した後は、保有コストが市場価格を大幅に下回っているため、より大きな利益を得ることができます。

リスクと欠点

本戦略の最大のリスクは、初期ポジションが限られていることです。継続的な下落トレンドでは、ストップロスのリスクがあります。そのため、自分が許容できるストップロスの幅を設定する必要があります。

また、ストップロス幅の設定にも両極端があります。大きすぎるストップロス幅を設定すると、十分な深さの反発を捉えられません。一方、小さすぎるストップロス幅では、中期調整中に価格が再びストップロスを超えて反転する確率が高くなります。そのため、市場や自身のリスク選好に応じて適切なストップロス幅を選択することが重要です。

DCAサイクルが長く、多くの階層を形成した後、価格が大幅に上昇した場合、ポジションコストが高くなりすぎてストップロスができなくなるリスクがあります。これも、自分の総ポジション量と許容できる最大ポジションコストに基づいて、DCAの階層を適切に設定する必要があります。

最適化の提案

-

タイミングシグナルの最適化:異なるパラメータや異なるインジケーターの組み合わせをテストし、より勝率の高いシグナルを選択することができます。

-

ストップロスメカニズムの最適化:単純なトレーリングストップロスの代わりに、Λ型ストップロスやアーク型ストップロスをテストすることで、より良いストップロス効果が得られる可能性があります。また、ポジションの時間分割戦略を導入してストップロス幅を調整することもできます。

-

利確方法の最適化:異なるタイプのトレーリング利確をテストし、より最適な利確の出口を見つけることで、総収益率を向上させることができます。

-

反発防止メカニズムの追加:ストップロス後に再びDCAシグナルがトリガーされ、新規ポジションが建つ可能性があります。その場合、一定の反発防止範囲を設けて、ストップロス直後にすぐに積極的にポジションを建てないようにすることを検討できます。

まとめ

本戦略は、RSIインジケーターで買い時を判断し、指数関数で計算された動的ストップロスDCA戦略を用いて、保有数量と保有コストを動的に調整することで、レンジ相場で価格優位性を得ることを目指します。最適化の提案は主にエントリー・エグジットシグナル、ストップロス方法、利確方法などです。全体として、本戦略は指数DCAの核となる考え方を活用し、保有コストを継続的に引き下げることで、レンジ相場ではより多くの運用スペースを得、トレンド相場ではより高いリターンを得ることができます。ただし、自身の資金管理計画に基づいて適切なパラメータを選択し、全体的なポジションリスクをコントロールする必要があります。

- 1