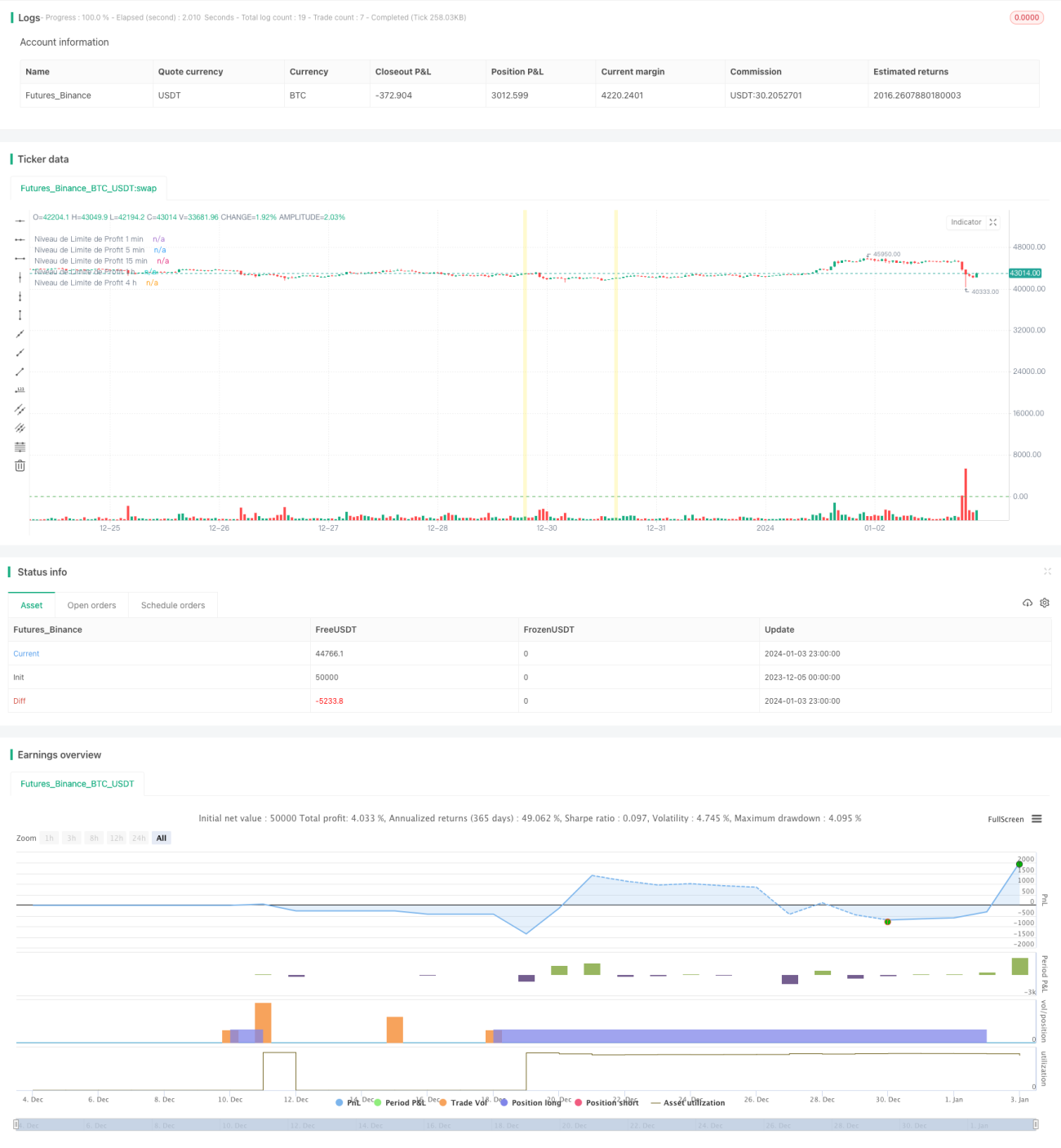

ブレイクアウトとスマート反転ボリンジャーバンド価格チャネル戦略

1

Follow

1802

Followers

概要

この戦略は、複数の時間足(1分、5分、15分、1時間、4時間)を組み合わせたブレイクアウト戦略であり、チャート上のサポートおよびレジスタンスゾーンを検出します。

戦略の原理

この戦略は、ボリンジャーバンドと価格チャネルを使用してサポートおよびレジスタンスゾーンを特定します。まず、各時間足の終値に基づいて単純移動平均線(SMA)と標準偏差(STDEV)を計算し、上限と下限を決定します。次に、「ブレイクアウトブロック」を検出します。これは、価格がサポートまたはレジスタンス水準をブレイクした状況と出来高に基づいて判断されます。高出来高を伴って価格がサポートまたはレジスタンス水準を突破した場合、ブレイクアウトブロックが形成されます。

ブレイクアウトブロックが検出されると、価格が下限を突破した場合は買いシグナルが、上限を突破した場合は売りシグナルが発生します。また、各時間足に対して価格チャネルを描画し、サポートとレジスタンスの水準を示します。

さらに、各時間足に対して利食いリミットレベルを設定します。これは、ポジションを利益確定で決済するための価格水準を指定することを意味します。同時に、損失を制限するためにストップロスレベルも設定します。

優位性の分析

- マルチタイムフレーム分析を活用し、より総合的に市場の動向を判断できる

- ブレイクアウトブロック、ボリンジャーバンドチャネル、出来高を組み合わせることで、シグナルの信頼性が向上

- 利食いとストップロスを設定することで、リスク管理に役立つ

リスク分析

- ボリンジャーバンドのパラメータ設定が不適切だと、偽のシグナルが発生する可能性がある

- ブレイクアウトが短期的な市場ノイズであり、高値掴みのリスクが生じる可能性がある

- マルチタイムフレームの判断により戦略の複雑性が増す

ボリンジャーバンドのパラメータを最適化したり、保有時間を延ばしたり、ストップロスを設定することで、これらのリスクをさらに回避できます。

最適化の方向性

この戦略は以下の点で最適化が可能です:

- ボリンジャーバンドのパラメータを最適化し、上限・下限が実際のサポートとレジスタンスをより正確に反映するようにする

- 機械学習アルゴリズムを追加し、ブレイクアウトの方向と強さを判断する

- 株価のボラティリティ指標を追加し、最適な売買タイミングを特定する

- MACDやKDなどの指標を追加し、トレンドと勢いを判断する

まとめ

この戦略は、複数の時間足のテクニカル指標分析を統合し、ブレイクアウト取引および利食い・ストップロスによるリスク管理を行う、柔軟で信頼性の高いブレイクアウトシステム取引戦略です。ただし、パラメータ設定とリスク管理は、実際の市場に応じて継続的にテストと最適化を行う必要があります。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1