動的トレンドフォロー反転戦略

概要

動的トレンド追跡反転戦略は、JD Sequential指標に基づく短期の定量取引戦略です。本戦略は、価格の高値と安値をリアルタイムで追跡し、現在のトレンドの方向性と強さを判断することで、市場の反転ポイントを効率的に捉え、エントリーとエグジットのタイミングを図ります。従来のJD Sequential戦略と比較して、以下の改善が施されています。

- 高値と安値を使用してトレンドを判断するため、終値を使用するよりも素早く価格変動を捉えることができます。

- カウンターの最大値は9ではなく7であり、より迅速に取引シグナルを生成できます。

- サポート・レジスタンスラインや5カウントの反転をストップロスとして使用するオプションが追加されました。

本戦略は、5分足や15分足などの短期時間足での使用に適しており、短期的な価格変動や反転の機会を効果的に捉えることができます。

戦略の原理

動的トレンド追跡反転戦略の核心ロジックはJD Sequential指標に基づいています。この指標は、現在の期間と過去2期間の高値・安値を比較し、価格が連続してより高い高値またはより低い安値を更新しているかどうかを判断し、1~7の順序カウントを提供します。カウントが7に達した時点で取引シグナルが生成されます。

具体的には、戦略内で以下の変数が定義されています。

- sp_up: 高値が2期間前の高値を超えた場合にtrue

- sp_dn: 安値が2期間前の安値を下回った場合にtrue

- sp_ct: 現在のカウントを記録。sp_upまたはsp_dnがtrueの場合に+1カウントされ、最大値は7

- sp_com: カウントが7に等しい場合にtrue

- sp_usr: カウントが7かつsp_upの場合の中間価格。上値抵抗線として機能

- sp_dsr: カウントが7かつsp_dnの場合の中間価格。下値支持線として機能

取引シグナルの生成ロジックは以下の通りです。

- ロングシグナル: sp_comがtrueかつsp_dnがtrue。カウント完了かつ下降トレンド中であることを示す。

- ショートシグナル: sp_comがtrueかつsp_upがtrue。カウント完了かつ上昇トレンド中であることを示す。

ストップロスのロジックは以下の通りです。

- ロングのストップロス: カウントが反転して5になる(sp_upがtrue)か、価格がsp_usrを上抜ける。

- ショートのストップロス: カウントが反転して5になる(sp_dnがtrue)か、価格がsp_dsrを下抜ける。

本戦略は、高値・安値をリアルタイムで比較することでトレンドの方向性と強さを判断し、カウンターによるタイミングでエントリーすることで、短期的な反転の機会を効果的に捉えることができます。また、ストップロスラインを設定してリスクをコントロールします。

優位性分析

従来のJD Sequential戦略と比較して、動的トレンド追跡反転戦略には以下のような優位性があります。

- より迅速なシグナル生成。高値・安値の比較は終値よりも速くトレンドを捉えることができ、7カウントは9カウントよりも速くシグナルを生成できます。

- ストップロスメカニズムの追加。5カウント反転やサポート・レジスタンスラインによるストップロスにより、リスクをより適切にコントロールできます。

- 柔軟な設定。ストップロスの有無や一部カウントの表示を選択可能。

- 短期取引に適合。高頻度のシグナルに適切なストップロスを組み合わせることで、特に短期時間足に適しています。

本戦略の主な強みは、反応が迅速であり、短期的な突発的なイベントによる大きな変動を効果的に捉えられる点です。また、完全な手動取引と比較して、アルゴリズムによるシグナル生成とストップロスはトレーダーの感情の影響を軽減し、安定性を向上させます。

リスク分析

動的トレンド追跡反転戦略には、以下のような一定のリスクも存在します。

- 高頻度取引による取引コストの増加。取引頻度が高いと、手数料やスリッページのコストが増加します。

- 誤ったシグナルが発生しやすい。レンジ相場では、高値・安値の比較が頻繁に取引シグナルを発生させ、簡単に嵌められる可能性があります。

- ストップロスが過激すぎる。ハードストップロスは容易に刈り取られる可能性があるため、適時にストップロスを移動させることを検討すべきです。

上記のリスクを低減するため、以下の点から最適化が可能です。

- ポジションサイズを調整し、1回の取引に使用する資金量を減らす。

- レンジ相場では取引を停止し、無駄な取引を避ける。

- 移動ストップロスやレンジブレイクアウトストップロスを採用し、嵌められる確率を低減する。

戦略の最適化方向

動的トレンド追跡反転戦略には、まだ大きな最適化の余地があります。主な方向性は以下の通りです。

- 複数時間足の組み合わせ。より上位の時間足で主要なトレンド方向を確認し、主要トレンドに逆らう取引を避ける。

- 他の指標との組み合わせ。ボラティリティ指標や出来高指標などと組み合わせることで、シグナルの品質を向上させる。

- 機械学習によるフィルタリング。機械学習アルゴリズムを用いて取引シグナルを補助的に判断し、誤取引を減らす。

- パラメータ最適化。カウント期間数、取引時間帯、ポジション比率などのパラメータを最適化し、異なる市場環境に適合させる。

- リスク管理メカニズムの強化。移動ストップロス、ポジションコントロールなど、より豊富なリスク管理手段を追加し、リスクをさらに制限する。

- バックテストによるデータ蓄積。バックテストのサンプル数と時間幅を拡大し、パラメータの安定性を検証する。

まとめ

動的トレンド追跡反転戦略は、高値・安値をリアルタイムで比較することでトレンドの方向性と強さを判断し、JD Sequential指標の7カウントルールを使用して取引シグナルを生成し、短期的な反転の機会を高頻度で捉えます。従来のJD戦略と比較して、本戦略は高値・安値を使用した判断、カウント期間の短縮、ストップロスメカニズムの追加などの改善を施しており、よりタイムリーな取引シグナルを得ることができます。

本戦略の主な強みは反応が迅速であり、短期反転の捕捉に適している一方、取引頻度が高いことやストップロスが過激であることなどのリスクも存在します。今後の最適化方向としては、パラメータ調整、リスク管理メカニズムの強化、複数時間足の組み合わせなどが挙げられます。継続的な最適化と反復により、本戦略は短期的な反転シグナルを効率的に捉える強力なツールとなることが期待されます。

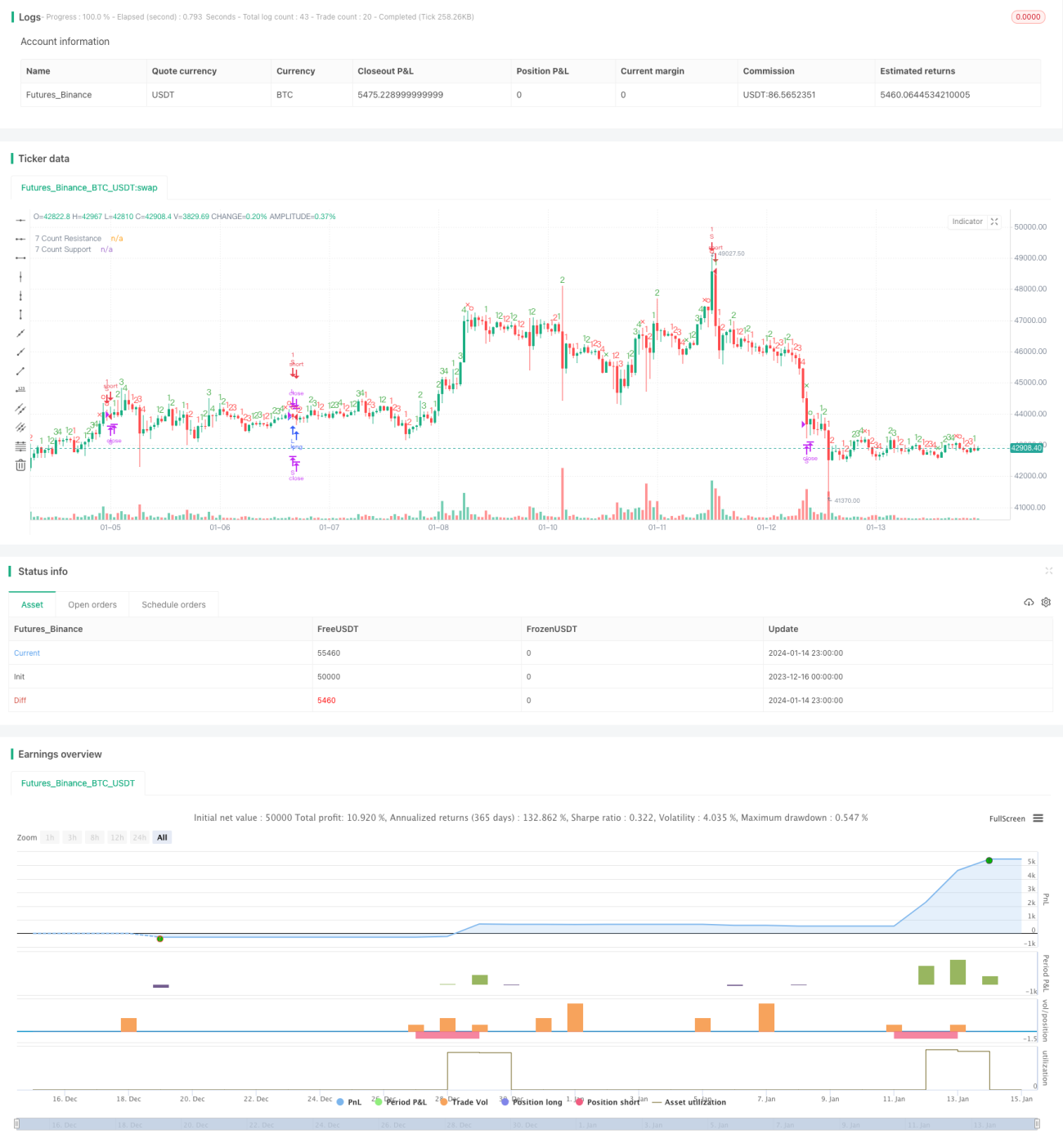

/*backtest

start: 2023-12-16 00:00:00

end: 2024-01-15 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// @NeoButane 7 Dec. 2018

// JD Aggressive Sequential Setup

// Not based off official Tom DeMarke documentation. As such, I have named the indicator JD instead oF TD to reflect this, and as a joke.

//- 1