多重移動平均線強気トレンド戦略

概要

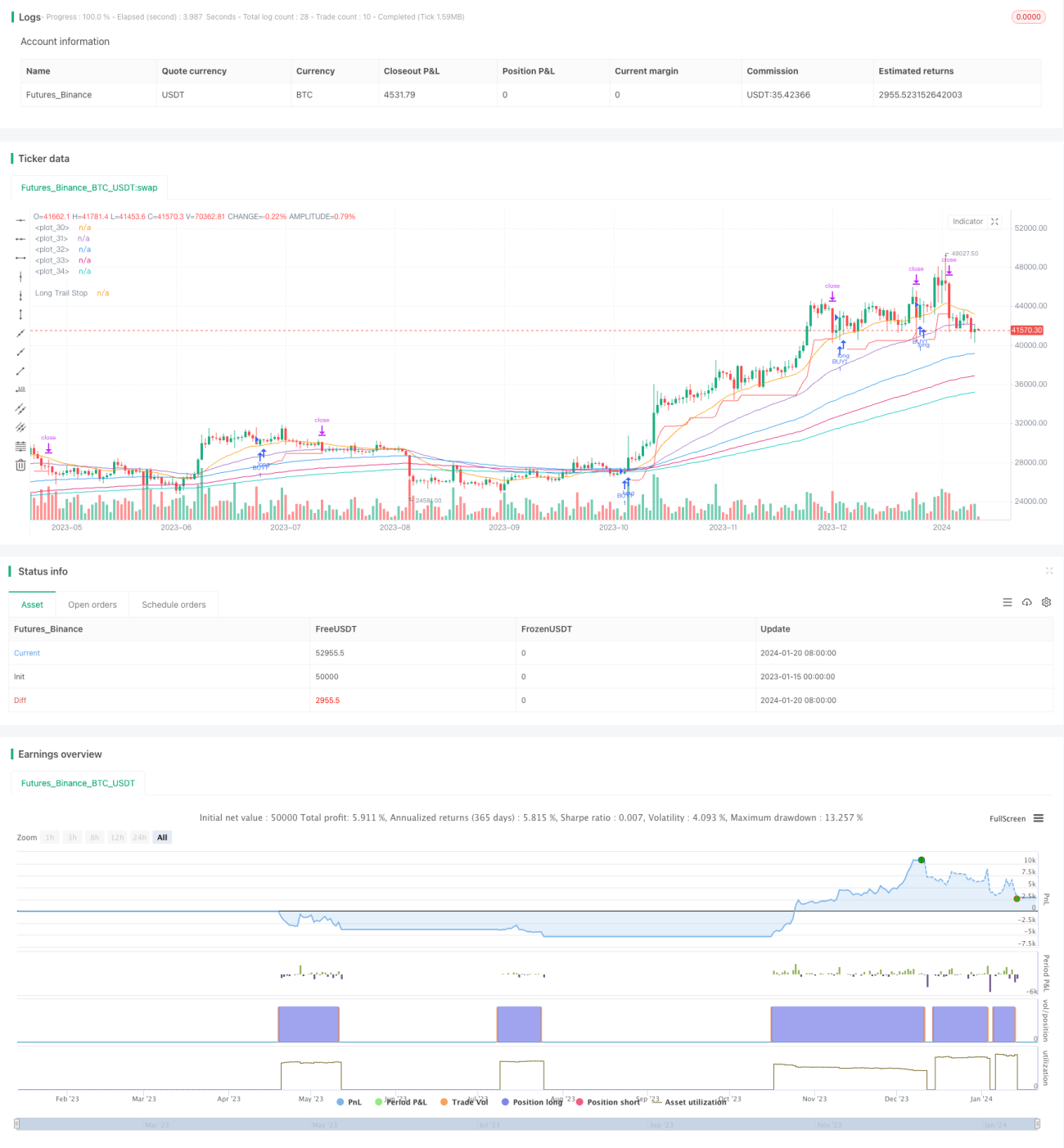

多重移動平均線による強気トレンド戦略は、異なる期間の複数の指数平滑移動平均線(EMA)に基づいて判断を行うトレンドフォロー戦略です。価格が10日EMAを突破し、他のより長期のEMAラインが強気の配列(マルチヘッド配列)になっている時に買いポジションを取ります。その後、8%のトレーリングストップを使用して利益を確定します。

戦略原理

本戦略は、10日、20日、50日、100日、150日、200日の6つの異なる期間のEMAラインを使用します。これらのEMAラインは、市場が現在どの周期段階にあるかを判断するために使用されます。短期EMA(例:10日線)が長期EMA(例:20日線、50日線)を上抜けた時、市場が強気トレンドのマークアップ段階に入ったと見なされます。

具体的には、以下の条件が全て満たされた場合に、戦略は買いポジションを開きます:

- 10日EMAが20日EMAよりも高い

- 20日EMAが50日EMAよりも高い

- 100日EMAが150日EMAよりも高い

- 150日EMAが200日EMAよりも高い

- 終値が10日EMAを上抜ける

買いポジションを開いた後、戦略は8%のトレーリングストップを使用して利益を確定します。つまり、株価が購入価格の8%以上下落しなければ、保有を継続します。8%を超える下落(ドローダウン)が発生した場合、損切りを行います。

全体として、この戦略の核心的な考え方は、EMAの多重フィルター条件を使用して強気トレンドへの突入を判断し、その後トレーリングストップで利益を確定することです。

優位性分析

本戦略(多重移動平均線強気トレンド戦略)には、以下のような主な利点があります。

- 偽のブレイクアウトを効果的にフィルタリングし、価格サイクルのマークアップ段階を確実に捉え、不要な取引回数を減らすことができます。

- EMAラインの多重フィルタリングにより、ストップロスが突破される可能性を低減し、より安全にポジションを保有できます。

- 8%のトレーリングストップは、きつすぎず緩すぎず、利益を適切に確定すると同時に、過度に頻繁なストップロスを避けることができます。

- 本戦略はパラメータ調整に柔軟性があり、異なる銘柄に合わせて最適なパラメータの組み合わせを見つけることができます。

リスク分析

本戦略には注意すべきリスクもいくつかあります。

- EMAラインの配列順序は相場のトレンドを100%判断できるわけではなく、依然として損失が発生する可能性があります。

- 8%のトレーリングストップは、大きな相場変動の中で利益の一部を失う可能性があります。

- EMA移動平均線システム自体が価格変動に対して遅延するため、転換点の判断が遅れる可能性があります。

これらのリスクに対しては、EMAの期間パラメータを適切に調整するか、他の指標を補助判断として導入することで最適化・改善が可能です。

最適化の方向性

本戦略の特性を考慮し、今後以下のような点から最適化を行うことができます。

- 異なるEMAの組み合わせや期間パラメータをテストし、最適なパラメータを見つける。

- ボラティリティインデックス系の指標を追加してトレンドの強さを判断し、不要なエントリーを避ける。

- MACD、KDJなどの追加のフィルター指標を導入して強気配列を判断する。

- 機械学習アルゴリズムを導入し、動的なストップロスを実現する。

まとめ

多重移動平均線による強気トレンド戦略は、全体的に比較的安定かつ信頼性の高いトレンドフォロー戦略です。トレンド判断とリスク管理の両方を兼ね備えています。パラメータ調整やアルゴリズムの最適化により、さらに改善の余地が大きくあります。総じて、試して使用し研究する価値のある有効な戦略です。

- 1