トレンドフォロー型ブレイクアウト戦略

概要

これはトレンドフォロー型のブレイクアウト戦略です。ブレイクアウトが発生した際に強い銘柄を買い、弱い銘柄を売り、トレンドに追随します。

戦略の原理

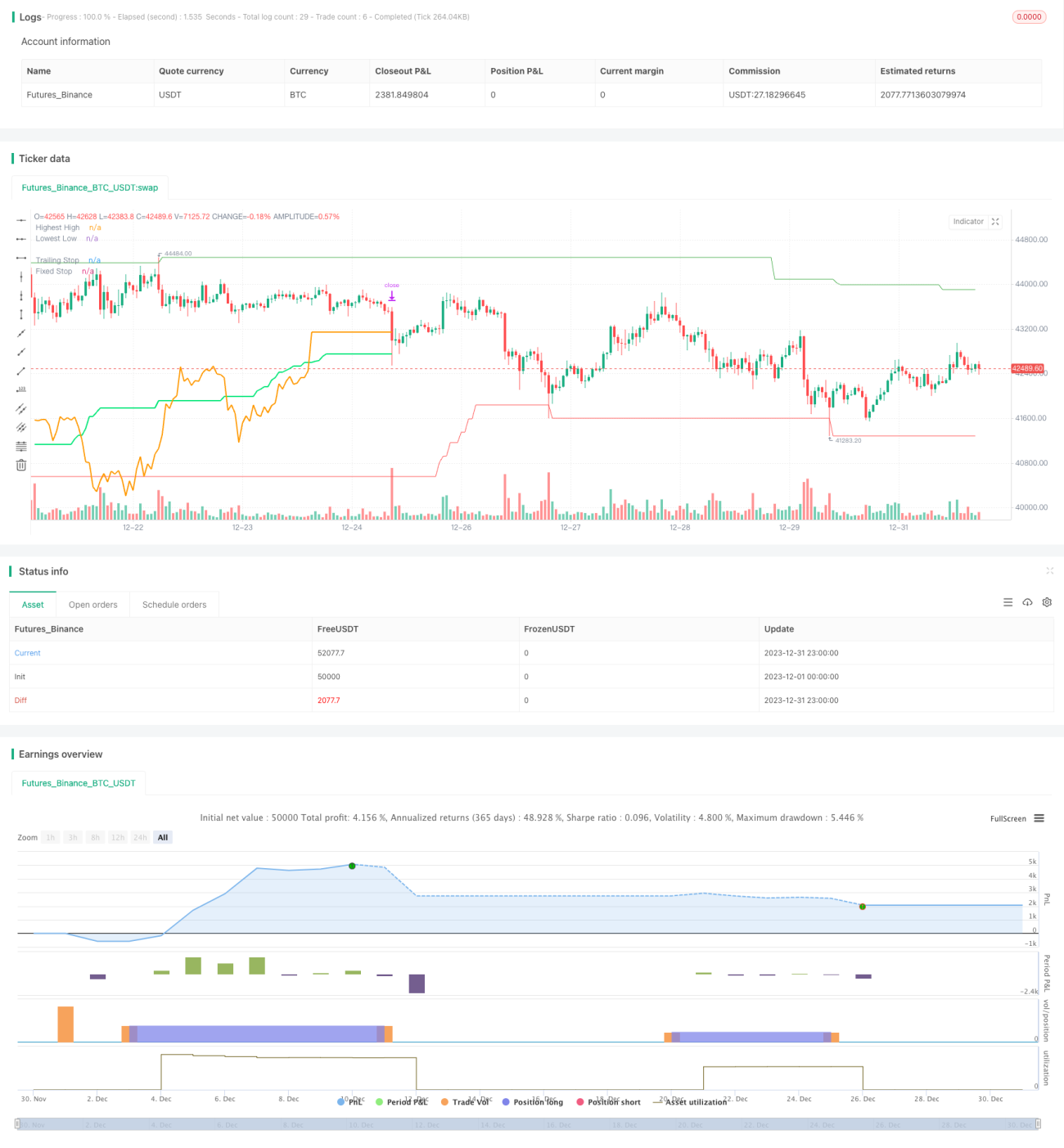

本戦略は主に2つの指標でエントリーとエグジットのシグナルを判断します。1つはhighest()関数で判断する一定期間の最高値、もう1つはlowest()関数で判断する一定期間の最安値です。

終値が過去一定期間(パラメータhighPeriod)の最高値を上回った場合、上昇トレンドのブレイクアウトと判断し、買いシグナルを発します。終値が過去一定期間(パラメータlowPeriod)の最安値を下回った場合、下降トレンドのブレイクアウトと判断し、売りシグナルを発します。

この戦略は同時にトレーリングストップと固定ストップを設定しています。トレーリングストップはATR指標に基づき、一定期間のATR値を計算し、その倍数(パラメータtrailingAtrMultiplier)をトレーリングストップ幅とします。固定ストップも同様にATR指標から算出します。

買い・売りエントリー後の最初のローソク足では固定ストップが有効となり、その後はトレーリングストップが主体となります。この組み合わせにより、一定の利益を確保しつつトレンドに追随できます。

また、本戦略にはポジションサイズ計算ルールが設定されています。許容最大損失率、口座資産などからポジションサイズを算出します。さらに取引銘柄数を考慮し、単一銘柄のポジションを適度に抑えます。

全体として、これは典型的なトレンドフォロー型戦略であり、ブレイクアウト発生時に市場に参入し、ストップで利益を確定しつつトレンドに追随し、トレンド反転時に退出します。

優位性分析

このブレイクアウト戦略の主な優位性は以下の通りです。

-

トレンド判断の正確性。最高値・最安値でトレンド反転を判断するため、誤シグナルが少なく精度が高い。

-

科学的で合理的なポジションサイズとストップ。最大損失率の設定や口座資産との連動により、過剰な取引や無効な取引を防止。ストップの組み合わせにより利益を確定しつつトレンドに追随。

-

シンプルで実用的、理解しやすい。基本的な指標のみを使用し、戦略ロジックが明確で習得が容易。

-

拡張性が高い。指標パラメータやポジションルールは入力ボックスで提供されており、ユーザーが調整可能。

総じて、実用性の高いブレイクアウト戦略である。判断は安全確実で、リスク管理とトレンド追随も考慮されている。中長期の保有に適している。

リスク分析

本戦略の主なリスクは以下の通りです。

-

トレンド反転リスク。ブレイクアウト戦略はトレンド判断に大きく依存するため、判断を誤ると大きな損失が発生する可能性がある。

-

パラメータ不適切リスク。最高値・最安値の期間パラメータを誤るとトレンドを見逃す可能性があり、ポジションサイズパラメータを誤ると損失が拡大する可能性がある。

-

ストップが過度にアグレッシブになるリスク。トレーリングストップの距離が小さすぎると、市場ノイズでロスカットされる可能性がある。

主な対策は以下の通りです。

-

トレンドフィルターの追加。例えば他の指標を加えて誤ったブレイクアウトを回避する。

-

パラメータの最適化。パラメータをテストし最適値を選択、安定性を確保する。

-

ストップ距離を適度に拡大。ある程度の調整に耐えられるようにする。

最適化の方向性

本戦略は以下の方向で最適化が可能です。

-

トレンド判断指標の追加。最高値・最安値に加え、移動平均線などを導入し、トレンド判断の精度を高める。

-

パラメータ設定の最適化。最高値・最安値の期間、ストップ倍数などをテストし、最適なパラメータの組み合わせを選択する。

-

市場に応じたポジションサイズ調整。ポジションサイズを市場のボラティリティと連動させる(例:VIX上昇時にポジションを縮小)。

-

出来高指標フィルターの追加。出来高を伴うブレイクアウトのみエントリーし、偽のブレイクアウトを回避する。

-

ベーシスと相関性による銘柄選択の最適化。ベーシスの変動が小さく、相関性の低い銘柄を組み合わせ、ポートフォリオリスクを低減する。

-

ストップメカニズムの最適化。トレーリングストップと固定ストップの比率をテストし、過度にアグレッシブなストップを回避する。

まとめ

本戦略はトレンドフォロー型のブレイクアウト戦略として、判断の正確性、ポジションサイズとリスク管理、運用の簡便性において優れたパフォーマンスを示しています。トレンドの初期を捉え、トレーリングストップによって利益の確定とトレンド追随のバランスを取っています。

もちろん、ブレイクアウト戦略である以上、トレンド判断への依存度が高く、ノイズの影響を受けやすいという弱点があります。また、パラメータ設定の不適切さが戦略パフォーマンスに影響を与える可能性もあります。これらの課題はさらなる最適化により解決する必要があります。

総じて、非常に実用的な戦略であり、その基本構造は定量戦略に必要な最も重要な要素を既に備えています。継続的に最適化・改良を重ねれば、安定的に利益を上げるプログラム戦略になり得ます。定量トレーダーにとって学びと参考の価値があるものです。

- 1