渐進的BB KCトレンド戦略

1

Follow

1802

Followers

概要

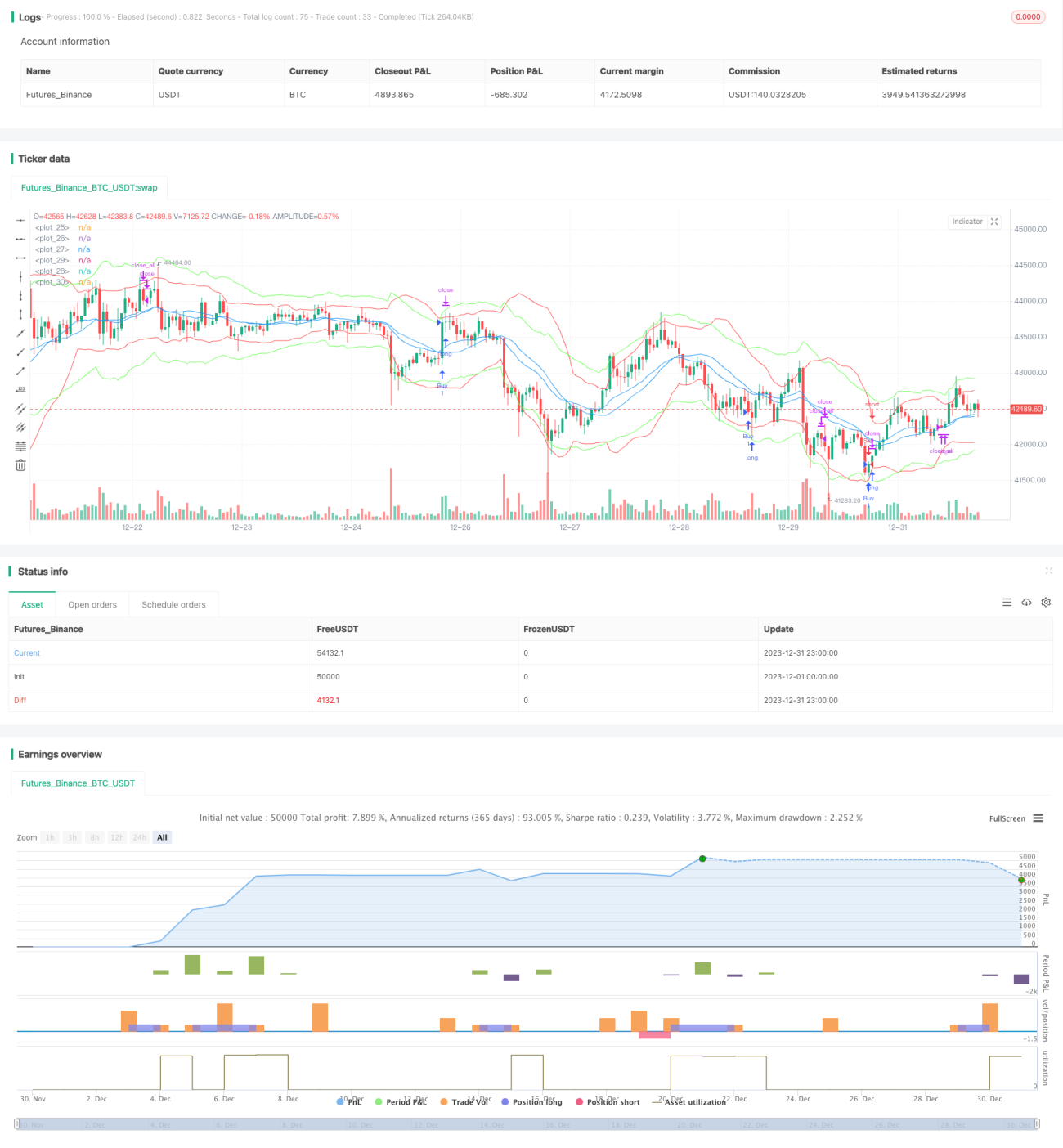

本戦略は、ボリンジャーバンドとケルトナーチャネルを組み合わせて市場トレンドを識別します。ボリンジャーバンドは価格の変動範囲に基づいてチャネルを定義するテクニカル分析ツールです。ケルトナーチャネルは、価格の変動性とトレンド性を組み合わせてサポートやレジスタンスを判断するテクニカル指標です。両指標を併用することで、ボリンジャーバンドとケルトナーチャネルのゴールデンクロス発生を判断材料にロング・ショートの機会を探り、出来高の状況でシグナルを検証します。これによりトレンドの開始を効果的に捉え、無効なシグナルを最大限削減できます。

戦略の原理

- 20期間のボリンジャーバンドの中央線、上限線、下限線を計算し、バンド幅は標準偏差の2倍で規定します。

- 20期間のケルトナー中央線、上限線、下限線を計算し、バンド幅は真の範囲(ATR)の2.2倍で規定します。

- ケルトナー上限線がボリンジャー上限線を上抜け、かつ出来高が10期間平均を上回った場合にロングします。

- ケルトナー下限線がボリンジャー下限線を下抜け、かつ出来高が10期間平均を上回った場合にショートします。

- ポジション建て後20本のローソク足が経過しても決済されない場合、強制的に利確・損切りで決済します。

- ロング後は1.5%のストップロス、ショート後は-1.5%のストップロスを設定し、ロング後は2%のトレーリングストップ、ショート後は-2%のトレーリングストップを設定します。

本戦略は主にボリンジャーバンドで変動範囲と強度を判断し、ケルトナーチャネルで補助検証を行います。パラメータは異なるものの性質が似ている2つの指標を組み合わせることでシグナルの精度を高め、出来高を加えることで無効なシグナルを効果的に減少させます。

優位性分析

- ボリンジャーバンドとケルトナーチャネル両指標の利点を総合的に活用し、取引シグナルの精度を向上。

- 出来高指標と組み合わせることで、市場で頻繁にラインを突破する無効シグナルを効果的に削減。

- ストップロスとトレーリングストップのメカニズムによりリスクを効果的に管理。

- 無効シグナル後の強制的な利確・損切り設定により、迅速な損切り・利確が可能。

リスク分析

- ボリンジャーバンドもケルトナーチャネルも移動平均線をベースに変動性を加味した指標であり、レンジ相場では誤シグナルが発生しやすい。

- 複利メカニズムがなく、何度も損切りに遭うと大きな損失につながる可能性がある。

- 反転シグナルが比較的多く、パラメータ調整後にトレンド機会を逃しやすい。

ストップロスの幅を適度に広げるか、MACDなどの補助指標を追加してシグナルをフィルタリングすることで、誤シグナルによるリスクを軽減できます。

最適化の方向性

- 異なるパラメータ(移動平均線の期間や標準偏差の倍数など)が戦略の収益率に与える影響をテスト可能。

- KDJやMACDなど他の指標を追加してシグナルを判断することで精度向上が可能。

- 機械学習手法によるパラメータ自動最適化が可能。

まとめ

本戦略はボリンジャーバンドとケルトナーチャネルを総合的に用いて市場トレンドを識別し、出来高指標でシグナルを補完します。パラメータ最適化や他のテクニカル指標の追加などによりさらに強化でき、より幅広い市場状況に適応可能です。本戦略は全体的に実用性が高く、習得と調整が容易な定量取引戦略の一つです。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1