トレンドフォロー移動平均線クロス戦略

1

Follow

1802

Followers

概要

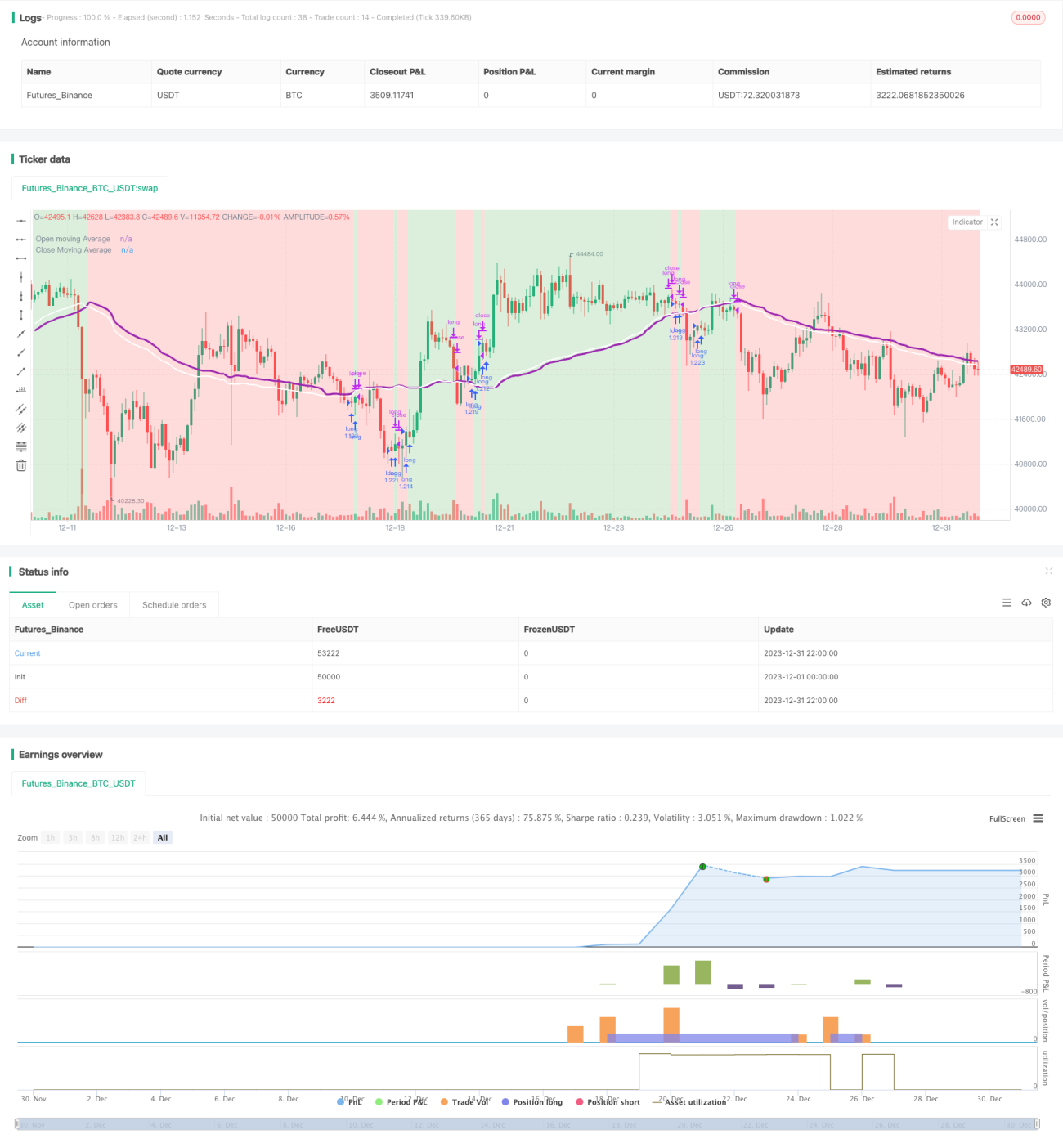

この戦略は移動平均線に基づいたシンプルな戦略で、様々な通貨ペアで良好な結果を得ることができます。始値の移動平均線と終値の移動平均線を描画し、2本の線がクロスしたタイミングでロングポジションの構築または決済を行います。原理としては、平均終値が上昇したときにポジションを構築し、これは将来の価格上昇を示唆する可能性があります。平均終値が下落したときにポジションを手仕舞い、これは将来の価格下落を示唆する可能性があります。あくまで推測に過ぎませんが、将来の価格を非常に正確に予測できる場合もあります。

戦略の原理

この戦略はまず、設定に基づいて移動平均線の種類(EMA、SMA、RMA、WMA、VWMA)を選択します。次に、移動平均線の計算期間(通常は10~250本のローソク足)を設定します。通貨ペアによって、異なる移動平均線の種類と期間を選択することで、全く異なる結果を得ることができます。

この戦略の具体的な取引ロジックは以下の通りです:

- 始値と終値の移動平均線を計算します。

- 終値の移動平均線と始値の移動平均線の値を比較します。

- 終値の移動平均線が始値の移動平均線を上抜けした場合、ロングポジションを構築します。

- 終値の移動平均線が始値の移動平均線を下抜けした場合、ロングポジションを手仕舞います。

ポジションを構築するのは価格上昇の兆候とみなし、手仕舞うのは価格下落の兆候とみなします。

戦略の優位性分析

この戦略には主に以下の利点があります:

- パラメータ設定が柔軟で、異なる通貨ペアに応じて最適なパラメータを選択できるため、ターゲットを絞った運用が可能。

- ロジックがシンプルで、理解・実装が容易。

- 一部の通貨ペアでは非常に高い収益率を得られ、全体的に安定性が比較的高い。

- ニーズに応じて異なるインジケーターを表示可能で、カスタマイズ性が高い。

リスク分析

この戦略には以下のリスクも存在します:

- 一部の通貨ペアやパラメータでは、収益率と安定性が高くない。

- 短期的な価格変動に効果的に対応できず、ボラティリティの高い通貨ペアには効果が乏しい。

- 移動平均線の期間選択の根拠が科学的・合理的とは言えず、ある程度の主観性がある。

対策と最適化の方向性:

- 可能な限り長期の時間足(12時間足、日足など)を選択することで、不要な取引を減らし安定性を高める。

- パラメータ最適化機能を追加し、異なるパラメータの組み合わせを自動テストして最適パラメータを見つける。

- 移動平均線の期間を適応的に選択する機能を追加し、システムが自動的に最適な期間を決定できるようにする。

まとめ

この戦略は全体的にロジックがシンプルで、移動平均線指標を用いて価格のトレンドと転換点を判断します。パラメータ調整により非常に良い結果を得ることが可能であり、有効なトレンド追従戦略として、さらなる改良と応用に値します。ただし、リスク管理にも注意し、適切な通貨ペアとパラメータを選択して、最大限の効果を発揮させる必要があります。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1