マルチインジケーターに基づくトレンドフォロー戦略

概要

本戦略は、複数の指標を組み合わせてトレンドを特定し、トレンドフォロー型のストップロスで利益を確定する。主にボリンジャーバンド、RSI、ADXなどの指標を使用してエントリータイミングを判断し、ATRとボリンジャーバンドでストップロスを設定する。

戦略の原理

戦略の主要判断指標はボリンジャーバンド、RSI、ADXである。価格がボリンジャーバンドの下限に近づき、RSIが30を下回った場合、売られ過ぎと判断してロング(買い)を行う。価格がボリンジャーバンドの上限に近づき、RSIが70を上回った場合、買われ過ぎと判断してショート(売り)を行う。さらに、ADXが25を上回っている場合はトレンド形成と判断し、その場合の売買シグナルはより有効となる。

ポジション保有後は、ATR指標とボリンジャーバンドの上下限を使用してストップロスを行う。具体的には、ATRで最大ストップロス幅を設定し、価格が最大ストップロス地点に達したら損切りする。ボリンジャーバンドの上下限はトレーリングストップロスに使用し、価格の動きに応じてリアルタイムでトレーリングストップロス価格を更新する。

優位性分析

本戦略は複数の指標を組み合わせて判断するため、トレンドを効果的に識別でき、ストップロス機構で利益を確定し損失リスクを低減する、比較的堅実な戦略である。具体的な優位性は以下のとおり。

- ボリンジャーバンドで買われ過ぎ・売られ過ぎを判断し、反転の機会を捉えられる。

- RSI指標と組み合わせることで判断精度が向上する。

- ADX指標でトレンド形成を判断し、取引方向の正しさを確保する。

- ATRとボリンジャーバンドによるトレーリングストップロスで利益を最大限確保できる。

リスク分析

本戦略には以下のリスクも存在する。

- 複数指標による判断のため、パラメータ設定が過剰最適化されやすい。

- ボリンジャーバンドの幅が広い場合、買われ過ぎ・売られ過ぎシグナルの効果が低下する。

- ストップロスの追跡が不適切だと損失が拡大する可能性がある。

これらのリスクに対し、以下の対策を講じることができる。

- 複数のパラメータ組み合わせで最適化を行い、過剰最適化を防ぐ。

- 市場の変動に応じてボリンジャーバンドのパラメータを調整する。

- ストップロス距離のパラメータをテストし、通常の変動に耐えられるようにする。

最適化の方向性

本戦略は以下の方向でも最適化が可能である。

- ポジションサイズ管理を追加し、ストップロス乗数に応じてポジション規模を調整する。

- マネーマネジメントモジュールを追加し、1回のストップロス損失額を厳格に制御する。

- DMI、Envelopなど他のストップロス指標をテストする。

- 機械学習モデルを追加してトレンド確率を判断し、効果を高める。

まとめ

本戦略は総じて比較的堅実なトレンドフォロー型戦略である。複数指標でトレンド方向を確定し、ストップロス措置でリスクを管理することで、良好なリターンを得られる。また、いくつかの最適化の方向性も提示しており、さらなる改良により一層の効果向上が期待できる。

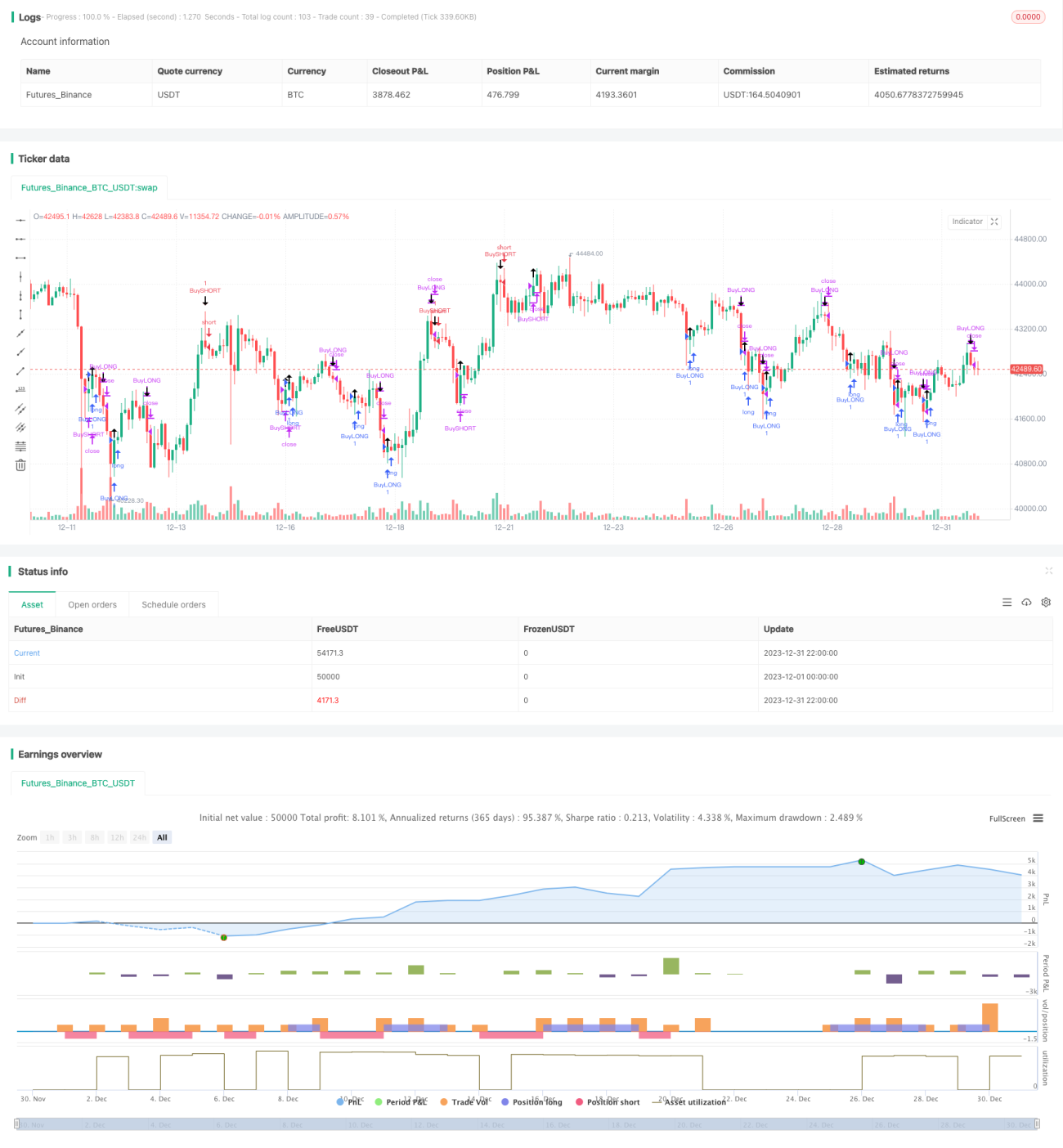

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

// THIS SCRIPT IS MEANT TO ACCOMPANY COMMAND EXECUTION BOTS

// THE INCLUDED STRATEGY IS NOT MEANT FOR LIVE TRADING

// THIS STRATEGY IS PURELY AN EXAMLE TO START EXPERIMENTATING WITH YOUR OWN IDEAS- 1