CCIとEMAに基づく短期振れ戦略

概要

本戦略は短期のレンジ相場向けトレード戦略であり、EMA移動平均線とCCI指標を組み合わせて市場の短期トレンドと買われ過ぎ・売られ過ぎ状態を識別し、短期的な価格変動のチャンスを捉えます。

戦略の原理

本戦略は主に10日EMA、21日EMA、50日EMAの3本の移動平均線とCCI指標を用いてエントリーとエグジットのタイミングを判断します。

具体的なロジックは以下の通りです。

短期移動平均線(10日EMA)が中期移動平均線(21日EMA)を上抜け、かつ短期移動平均線が長期移動平均線(50日EMA)より高く、さらにCCI指標が0より大きい場合、強気シグナルとみなし買いエントリーを行います。短期移動平均線が中期移動平均線を下抜け、かつ短期移動平均線が長期移動平均線より低く、さらにCCI指標が0より小さい場合、弱気シグナルとみなし売りエントリーを行います。

手仕舞いのロジックは、短期移動平均線が再び中期移動平均線をクロスした時点で決済します。

戦略のメリット

-

移動平均線システムとCCI指標を組み合わせることで、短期的な価格変動のトレンド方向と買われ過ぎ・売られ過ぎ状態を効果的に識別できます。

-

移動平均線のゴールデンクロスとデッドクロスを利用してエントリーとエグジットを判断するため、シンプルで実用的です。

-

CCI指標のパラメータと期間設定が比較的妥当であり、一部の偽シグナルを除去できます。

-

複数の時間枠の移動平均線を採用することで、レンジ相場において良好なトレード機会を得られます。

戦略のリスク

-

短期トレードは変動が大きく、連続してストップロスが発生する可能性があります。

-

CCI指標のパラメータ設定が不適切だと、偽シグナルが増える恐れがあります。

-

レンジ相場の整理期間中、本戦略では少額の損失が複数回発生する可能性があります。

-

短期間で頻繁にトレードを行うトレーダーにのみ適しており、長期保有には向きません。

対応するリスク対策としては、CCIパラメータの最適化、ストップロス位置の調整、フィルター条件の追加などが挙げられます。

戦略の最適化方向

-

異なる期間のEMA移動平均線の組み合わせをテストし、パラメータを最適化できます。

-

MACDやKDJなど、他の指標やフィルター条件を追加して、一部の偽シグナルを除去できます。

-

動的なトレーリングストップを用いて、1回の損失を管理できます。

-

より長い時間枠のトレンド指標を組み合わせ、逆張りを避けることができます。

まとめ

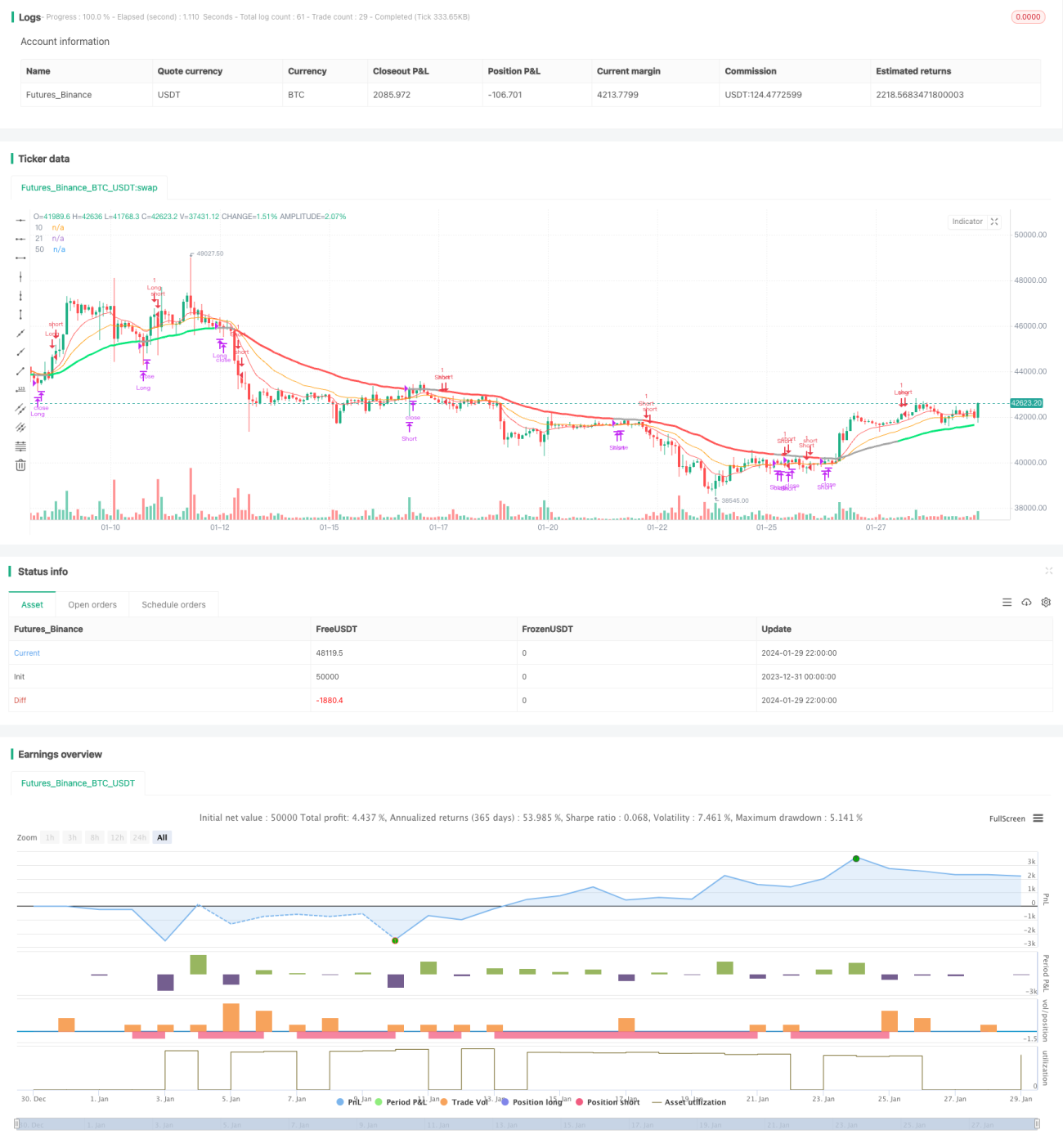

本戦略は全体的に典型的な短期レンジ相場戦略であり、移動平均線のゴールデンクロス・デッドクロスとCCI指標の買われ過ぎ・売られ過ぎ状態を利用して、価格の短期的な反転のチャンスを捉えます。本戦略は短期間での頻繁なトレードに適していますが、一定のストップロス圧力に耐える必要があります。パラメータの最適化やフィルター条件の追加により、戦略の安定性と収益性をさらに向上させることができます。

/*backtest

start: 2023-12-31 00:00:00

end: 2024-01-30 00:00:00

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

//study(title="Strat CCI EMA scalping", shorttitle="EMA-CCI-strat", overlay=true)

strategy("Strat CCI EMA scalping", shorttitle="EMA-CCI-strat", overlay=true)

- 1