二因子リバーサル・バンドブレイクアウト・コンビネーション戦略

1

Follow

1802

Followers

概要

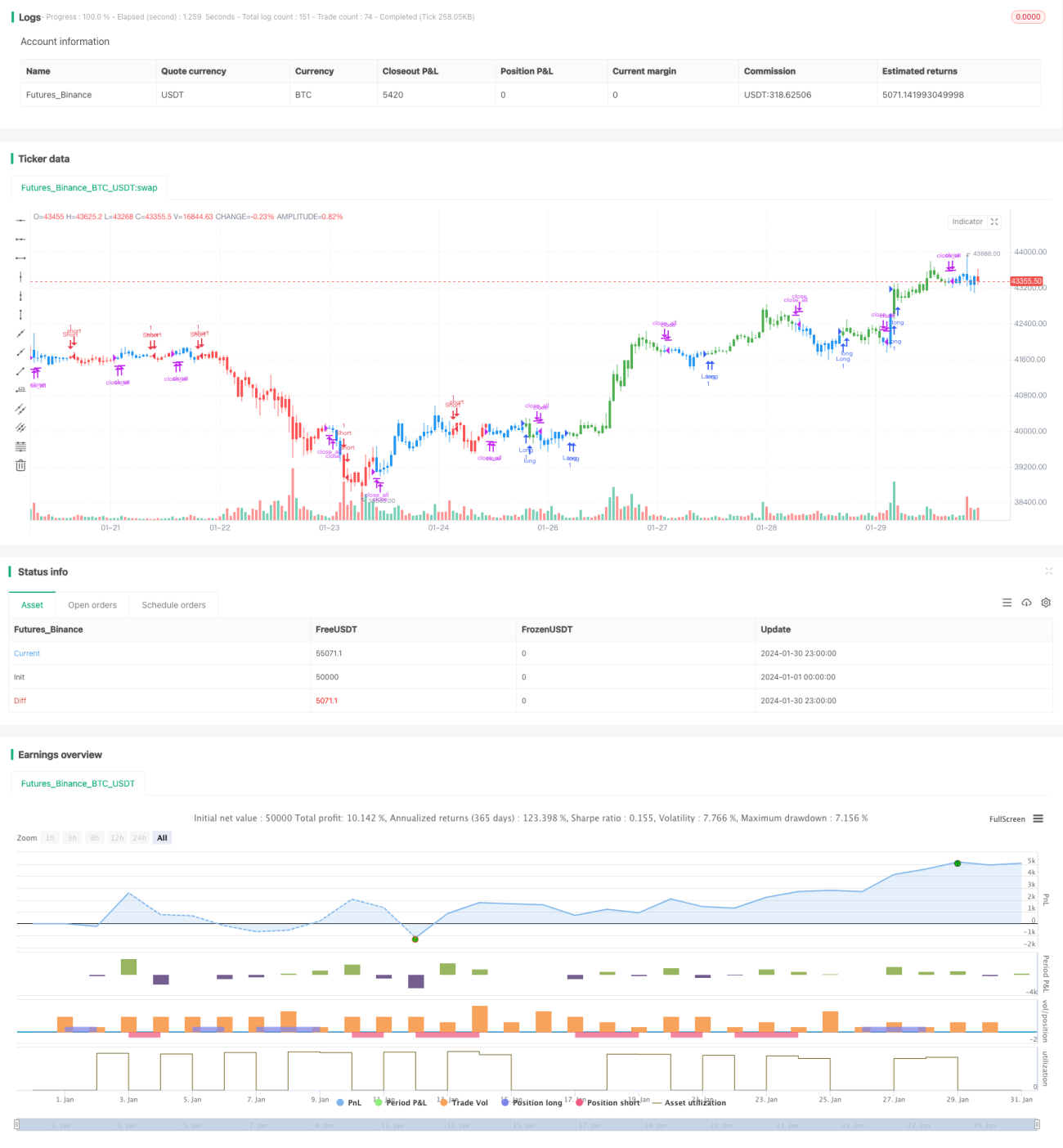

本戦略は2つの因子を組み合わせた戦略であり、逆転因子とバンド・チャネル因子によって駆動され、複数因子を重ね合わせることで、異なる市場環境において戦略の優位性を発揮します。

戦略の原理

本戦略は以下の2つのサブ戦略から構成されます:

-

123逆転戦略: 終値が2日連続で下落した後、本日の終値がそれまでの2日間の最安値を上抜け、かつ9日間のストキャスティクスの%Kラインが%Dラインを上抜けた場合に買いシグナル。終値が2日連続で上昇した後、本日の終値がそれまでの2日間の最高値を下抜け、かつ9日間のストキャスティクスの%Kラインが%Dラインを下抜けた場合に売りシグナル。

-

バンド・フィルター: 一定期間の価格からバンド指標を計算し、バンド指標がある閾値より大きい場合は買い、ある閾値より小さい場合は売り。

複合シグナルは、123逆転戦略とバンド・フィルター戦略の両方が買いシグナルである場合に買いポジションを保有し、両方が売りシグナルである場合に売りポジションを保有し、それ以外はポジションをクローズします。

戦略の優位性

- 2つの因子で駆動されるため、市場への適応性が高く、様々な相場で利益を獲得可能

- 123逆転戦略は、レンジ相場において逆転のチャンスを捉える

- バンド・フィルターは、明確なトレンド相場でトレンドに追随できる

- 複合シグナルによる検証により、誤ったトレードの確率を低減できる

リスク分析

- パラメータ設定が不適切だと、取引回数が過剰になる可能性がある

- レンジ相場では複数の損失が発生する可能性がある

- 取引手数料の影響に注意する必要がある

最適化の方向性

- バンド・フィルターのパラメータを調整し、バンド指標の計算を最適化する

- 123逆転戦略のパラメータを調整し、買い・売りの逆転判定を最適化する

- 損切りメカニズムを導入し、1回当たりの損失を管理する

まとめ

本戦略は逆転因子とトレンド因子を総合的に活用し、複数因子駆動の定量取引を実現しています。2つの因子による検証により誤トレードの確率を低減し、様々な市場で優れたパフォーマンスを発揮します。今後、パラメータ調整や損切りの設定を通じてさらに最適化することで、戦略の安定性と収益性を向上させることが可能です。

Source

Pine

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 21/05/2019

// This is combo strategies for get Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1