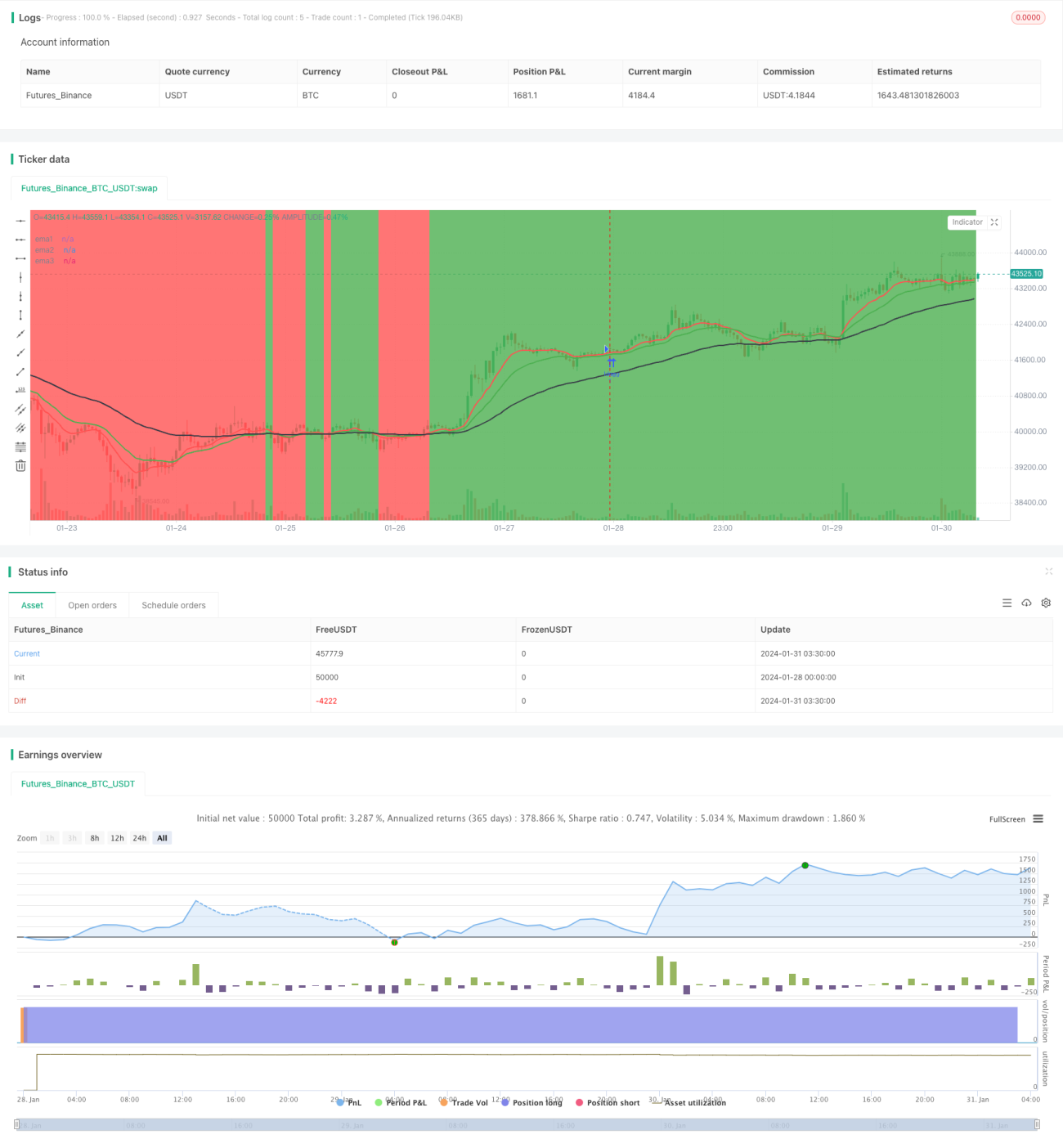

EMA平均線に基づくトレンド追従戦略

1

Follow

1802

Followers

概要

本戦略は、3つの異なる期間のEMA平均線に基づき、価格がEMA平均線より上にあるかどうかを判断して現在のトレンド方向を判定します。短期EMA線が長期EMA線を上抜けたときに買いシグナルを生成し、短期EMA線が長期EMA線を下抜けたときに売りシグナルを生成します。この戦略はトレンドに追随し、トレンドが転換した際にポジションを決済します。

戦略の原理

本戦略では、10日線、20日線、50日線の3本のEMA平均線を使用します。判断ルールは以下の通りです。

- 10日EMA線と20日EMA線がともに50日EMA線より上にある場合、上昇トレンドと定義します。

- 10日EMA線と20日EMA線がともに50日EMA線より下にある場合、下降トレンドと定義します。

- 短期EMA線(10日線と20日線)が長期EMA線(50日線)を上抜けたときに買いシグナルが発生します。

- 短期EMA線(10日線と20日線)が長期EMA線(50日線)を下抜けたときに売りシグナルが発生します。

- 上昇トレンドではロングポジションを保有し、下降トレンドではショートポジションを保有します。

- トレンドが転換した時点(EMA短期線と長期線がクロスした時点)で、現在のシグナル方向のポジションを決済します。

本戦略は、利益を確保し、適時に決済して利益を確定することで、ロングとショートを交互に行います。

優位性分析

本戦略には以下のような利点があります。

- ルールがシンプルで明確であり、理解しやすく実装しやすい。

- EMA平均線を用いてトレンド方向を判断するため、市場の短期的な変動に左右されにくい。

- 適時に決済し、トレンドに追随することで損失の拡大を防ぐ。

- 相場の方向を予測する必要がなく、トレンドに追随するため勝率が高い。

リスク分析

本戦略には以下のようなリスクも存在します。

- レンジ相場ではEMA平均線間のクロスが何度も発生しやすく、頻繁なエントリーと決済により取引コストが増加する可能性がある。

- 価格がギャップを空けた場合、EMAによるトレンド判断の効果が影響を受け、良好なエントリーチャンスを逃す可能性がある。

上記のリスクに対しては、以下の方法で改善できます。

- EMAの間隔が狭い場合、エントリールールを適度に緩め、過度な取引を避ける。

- 他の指標と組み合わせてトレンドを判断し、EMAの判断が無効になる状況を回避する。

最適化の方向性

本戦略は以下の方向から最適化できます。

- パラメータ最適化:異なるEMA期間のパラメータ組み合わせをテストし、最適なパラメータを見つける。

- 取引コスト最適化:エントリールールを適宜最適化し、不要な頻繁な取引を減らす。

- ストップロス戦略の最適化:適切なストップロス水準を設定し、1回あたりの損失を抑制する。

- 他の指標の併用:MACD、KDJなどの他の指標を活用して判断を補助し、エントリータイミングを最適化する。

まとめ

本戦略は全体的にシンプルで実用的です。EMAを用いてトレンド方向を判断し、適切なストップロス戦略を組み合わせることで、リスクを効果的に管理できます。同時に最適化の余地もあり、パラメータ最適化、ストップロス戦略、他の指標との併用などを行うことで、さらに効果を高めることが可能です。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1