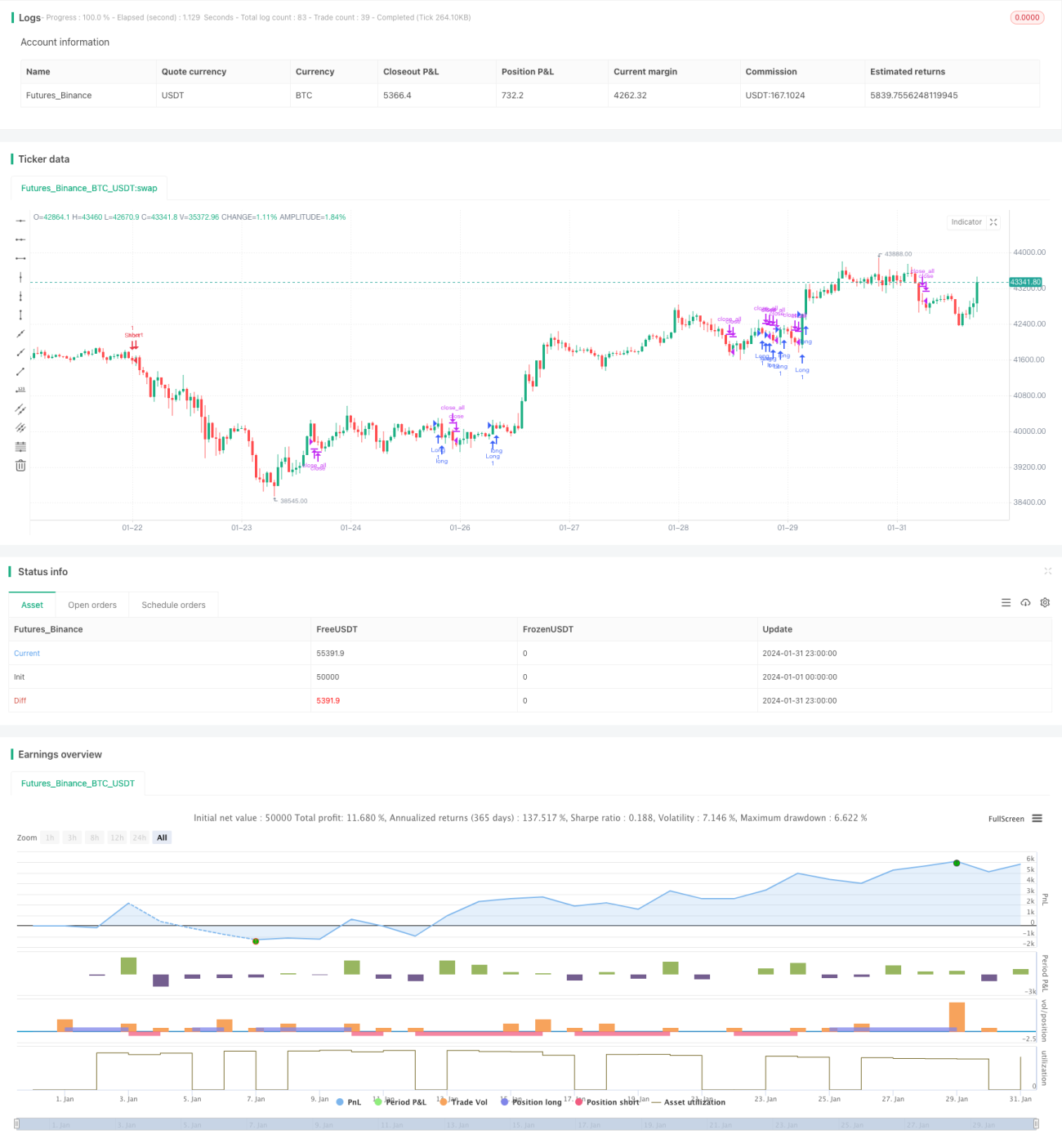

概要

本戦略の主な考え方は、123反転戦略と絶対価格変動指標という異なるタイプの2つの戦略を組み合わせ、統合シグナルを取得することです。具体的には、両方の戦略がロングシグナルを発した場合、最終戦略シグナルは1(ロング)となります。両方の戦略がショートシグナルを発した場合、最終戦略シグナルは-1(ショート)となります。両方の戦略のシグナルが一致しない場合、最終シグナルは0(何もしない)となります。

戦略原理

まず、123反転戦略の原理は以下の通りです。終値が2日連続で前日の終値を下回り、かつストキャスティクス・オシレーターが買われすぎラインを下回っている場合、ロングします。終値が2日連続で前日の終値を上回り、かつストキャスティクス・オシレーターが売られすぎラインを上回っている場合、ショートします。

次に、絶対価格変動指標(APO)は、2本の指数移動平均線の差を示します。短期移動平均線が長期移動平均線を上回っている場合はプラスとなり、トレンドが上昇していることを示します。逆の場合はマイナスとなり、トレンドが下降していることを示します。

最後に、本戦略は2つのサブ戦略のシグナルを統合します。つまり、両者が一致したシグナルを発した場合、そのシグナルに従って取引を行い、そうでない場合は取引を行いません。

優位性分析

本戦略は、短期的な反転シグナルと価格の中長期的なトレンドを総合的に考慮しており、相場の転換点を効果的に識別できます。123反転戦略やAPO指標を単独で使用する場合と比較して、本戦略はシグナルの信頼性を大幅に高め、誤ったシグナルの発生を低減できます。

また、本戦略は複数のテクニカル指標を活用して市場を総合的に判断するため、特定の指標のみに依存することはありません。これにより、ある指標が機能しなくなった場合でも、全体的な判断を誤るリスクを回避できます。

リスク分析

本戦略の最大のリスクは、123反転戦略とAPO指標が相反するシグナルを発した場合です。その場合、トレーダーは自身の経験に基づいてどちらのシグナルがより信頼できるかを判断する必要があります。判断を誤ると、取引機会を逃したり、損失が発生する可能性があります。

さらに、相場が急激に変動し、短期反転シグナルと中長期トレンドシグナルの両方が同時に機能しなくなった場合、戦略のシグナルも誤ったものになる可能性があります。トレーダーは、主要な政治・経済イベントが相場に与える影響に注意し、必要に応じて戦略の実行を一時停止する必要があります。

最適化の方向性

本戦略は、以下の方向で最適化できます。

-

サブ戦略のパラメータを最適化し、サブ戦略のシグナルをより信頼性の高いものにします。例えば、移動平均線の期間パラメータを調整します。

-

他の補助的な判断指標を追加し、投票メカニズムを形成します。複数の指標が一致したシグナルを発した場合、シグナルの信頼性がさらに高まります。

-

ストップロス戦略を追加します。価格の動きがテクニカル指標の予想に反した場合、早めに損切りすることで損失の拡大を防ぐことができます。

-

エントリーとストップロスの位置を最適化します。過去のバックテストデータに基づいて、より適切な具体的な数値を設定します。

まとめ

本戦略は、複数のテクニカル指標を総合的に活用して相場を判断することで、単一指標への依存リスクをある程度回避し、シグナル判断の精度を高めています。同時に、本戦略には改善の余地もあり、投資家は自身のニーズに合わせてパラメータを調整することができます。総じて、ダブル・コンフィデンス価格変動量子化戦略は、シグナル信頼性の高い取引戦略であり、さらなる研究と応用に値します。

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 22/04/2019

// This is combo strategies for get - 1