取引向けのIchimokuクラウドナイン戦略

概要

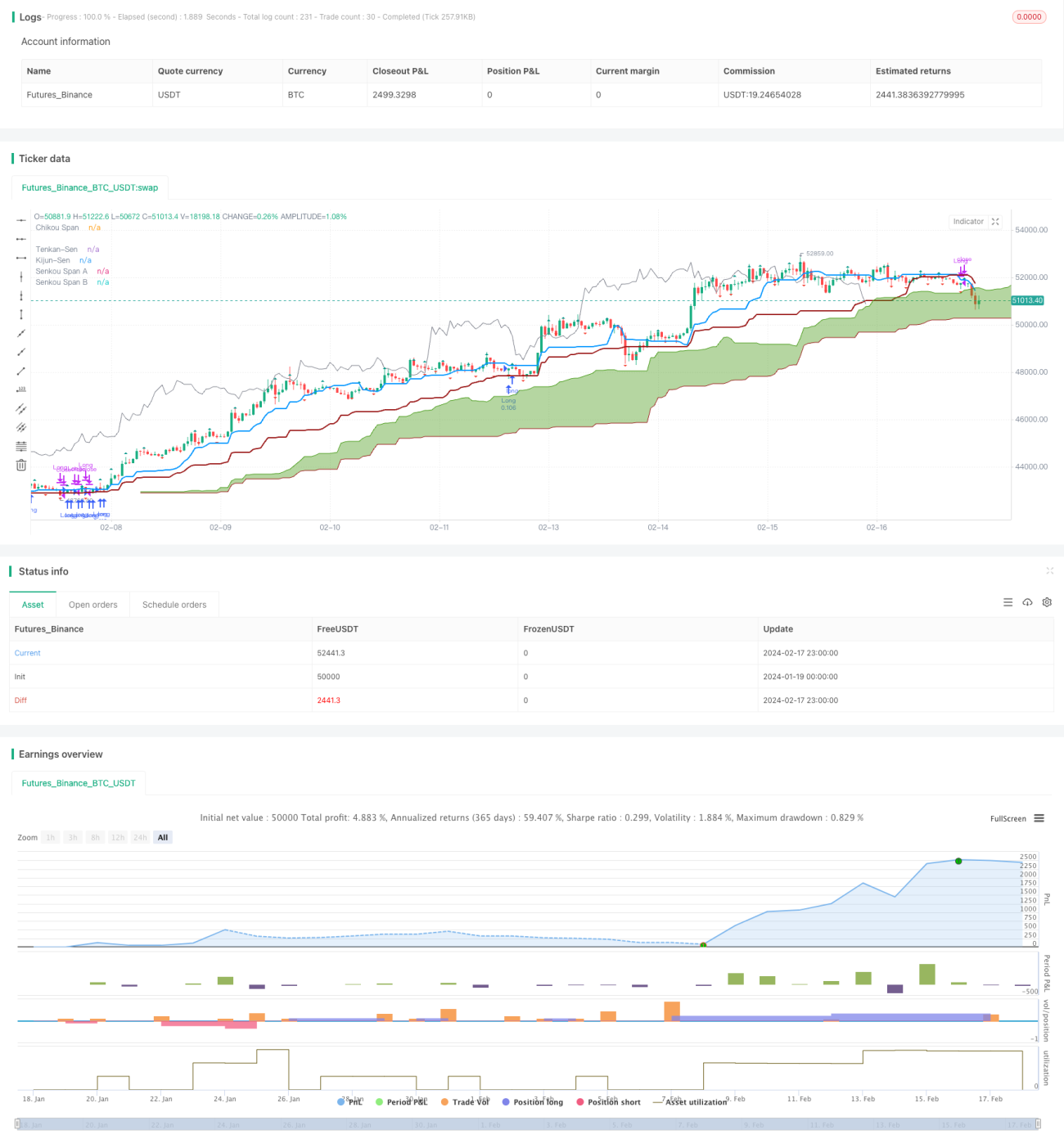

Ichimoku雲九戦略は、Ichimoku雲指標とWilliamsフラクタルを組み合わせた取引戦略です。この戦略は、Ichimoku雲指標が提供する複数の取引シグナルを利用して取引シグナルを生成します。実際の取引を目的とした戦略です。

戦略の原理

この戦略は主に以下のIchimokuシグナルに基づいてエントリーします。

- 雲の突破:価格の終値が雲の上端または下端を突破したときにシグナルが発生

- TKクロス:転換線(Tenkan)と基準線(Kijun)がクロスしたときにシグナルが発生

- 雲のねじれ:先行スパンA線と先行スパンB線がクロスしたときにシグナルが発生

- エッジクロス:価格が雲の片側から反対側に移動したときにシグナルが発生

さらに、この戦略は以下の状況でポジションをクローズします。

- 価格の終値が雲の中に入ったときにクローズ

- TKの逆クロスが発生したときにクローズ

- Williamsフラクタルがブレイクされたときに部分的にクローズ

この戦略は、Ichimoku雲チャートの複数の取引シグナルを統合し、取引シグナルの信頼性を高めるとともに、フラクタルを使用してストップロスを設定し、リスクを管理することを目的としています。

戦略の利点

単一シグナルの戦略と比較して、この戦略はIchimoku雲チャートの複数のシグナルを総合的に利用するため、誤ったシグナルをフィルタリングし、シグナルの精度を向上させることができます。同時に、戦略パラメータは柔軟に設定可能で、さまざまな銘柄やパラメータ最適化に適用できます。

さらに、戦略ではWilliamsフラクタルのブレイクを利用してストップロスを設定するため、より積極的にリスクを管理し、利益を確定し、大きな損失を回避できます。

戦略のリスク

この戦略は主に以下のリスクに直面します。

- 雲図指標には遅延性があり、価格変動をタイムリーに反映できない

- 複数のシグナルが保守的すぎて、一部の機会を逃す可能性がある

- フラクタルストップロスがブレイクされ、損失が発生する可能性がある

遅延性の問題に対しては、パラメータを適宜調整するか、一部のフィルタリングシグナルをオフにすることができます。フラクタルストップロスのリスクに対しては、フラクタルの時間周期を調整するか、部分的なストップロスのみを適用することができます。

戦略の最適化方向

この戦略は主に以下の観点から最適化できます。

- Ichimokuパラメータを調整し、異なる時間足や銘柄に適応させる

- 一部のフィルタリングシグナルを調整またはオフにし、コアシグナルを保持する

- フラクタルのパラメータを調整し、より大きな時間足のフラクタルを使用するか、部分的なストップロスのみを採用する

- 出来高指標などの他の指標フィルターを追加する

まとめ

Ichimoku雲九戦略は、Ichimoku雲チャートの複数の取引シグナルを統合することで、雲図指標の利点を活かしつつ、シグナルの精度と勝率を向上させます。また、戦略はフラクタルをストップロス手法として採用し、リスクを管理します。この戦略はパラメータとシグナルの最適化により、多銘柄のアルゴリズム取引に適用可能です。

/*backtest

start: 2024-01-19 00:00:00

end: 2024-02-18 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Ichimoku Cloud Nine", shorttitle="Ichimoku Cloud Nine", overlay=true, calc_on_every_tick = true, calc_on_order_fills = false, initial_capital = 5000, currency = "USD", default_qty_type = "percent_of_equity", default_qty_value = 10, pyramiding = 3, process_orders_on_close = true)

color green = #459915- 1