チャネル突破反転トレーディング戦略

1

Follow

1802

Followers

概要

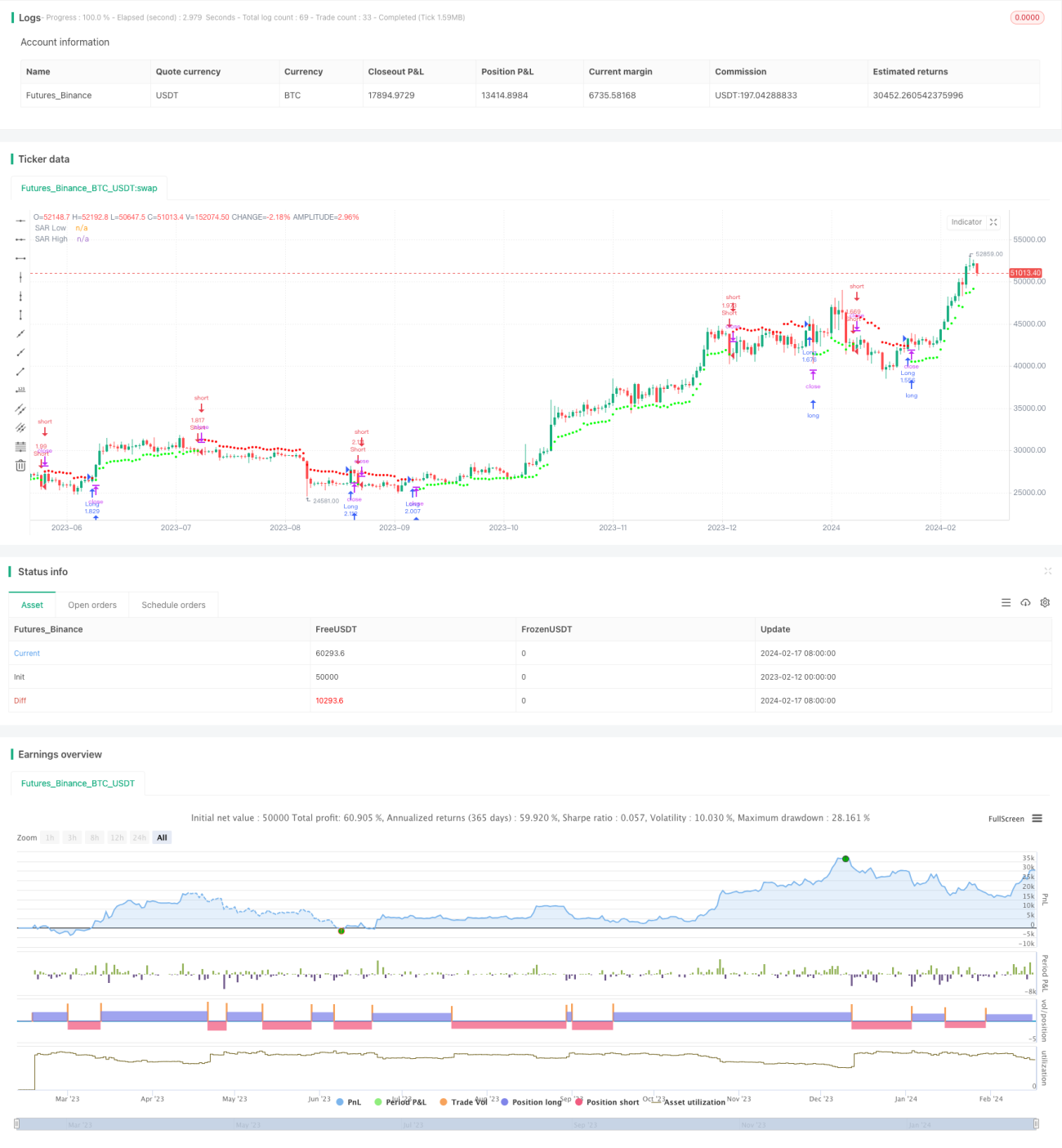

チャネルブレイクアウト逆張り取引戦略は、価格チャネルを追跡する移動利確・損切りポイントを用いた逆張り取引戦略です。加重移動平均法を用いて価格チャネルを計算し、価格がチャネルをブレイクしたときに買いまたは売りのポジションを取ります。

戦略の原理

本戦略はまず、Wilderの平均真実範囲(ATR)指標を用いて価格変動率を計算します。次にATR値から平均範囲定数(ARC)を計算します。ARCは価格チャネルの半幅です。次にチャネルの上限と下限、すなわち利確・損切りポイント(SARポイントと呼びます)を計算します。価格が上限をブレイクすると売り、下限をブレイクすると買いを行います。

具体的には、まず最近N本のローソク足のATRを計算します。次にATRに係数を乗じてARCを求めます。ARCに係数を乗じることでチャネルの幅を調整できます。ARCをN本のローソク足の最高終値に加えることでチャネル上限(高SAR)を、ARCを最低終値から引くことでチャネル下限(低SAR)を求めます。終値が上限をブレイクしたら売り、下限をブレイクしたら買いを行います。

戦略の利点

- 価格変動率を利用した適応型チャネルにより、市場の変化を追跡できます

- 逆張り取引、トレンド反転市場に適しています

- 移動利確・損切りにより、利益を確定しリスクを管理できます

戦略のリスク

- 逆張り取引は仕掛けられたままになりやすいため、適切にパラメータを調整する必要があります

- 大幅な変動のある市場ではポジションが手仕舞いされやすいです

- パラメータが不適切だと取引が過剰になる可能性があります

解決方法:

- ATR期間とARC係数を最適化し、チャネル幅を適切にします

- トレンド指標を組み合わせてエントリーのタイミングをフィルタリングします

- ATR期間を長くして取引頻度を減らします

戦略の最適化方向

- ATR期間とARC係数の最適化

- エントリー条件の追加(例:MACD指標との組み合わせ)

- 損切り戦略の追加

まとめ

チャネルブレイクアウト逆張り取引戦略は、チャネルを用いて価格変動を追跡し、変動が激しくなったときに逆張りでポジションを構築し、適応型の移動利確・損切りを設定します。この戦略は、逆張りが主体の保ち合い市場に適しており、反転ポイントを正確に予測できれば良好な投資収益を得られます。ただし、損切りポイントが緩くなりすぎないように注意し、パラメータ最適化の問題にも留意する必要があります。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1