モメンタムブレイクアウト戦略に基づく

概要

モメンタムブレイクアウト戦略は、市場の勢いを追跡するトレンドフォロー戦略です。複数の指標を組み合わせて市場が上昇トレンドか下降トレンドかを判断し、重要なレジスタンスラインをブレイクした時にロングポジションを建て、重要なサポートラインをブレイクした時にショートポジションを建てます。

戦略の原理

本戦略は主に複数の期間のドンチャンチャネルを計算し、市場のトレンドと重要な価格帯を判断します。具体的には、比較的長期(例:40日)のドンチャンチャネルの上限を価格が突破した場合に上昇トレンドと判断し、それに年初来高値や移動平均線の方向性配列などのフィルター条件を組み合わせてロングシグナルを出します。一方、長期のドンチャンチャネルの下限を価格が割り込んだ場合に下降トレンドと判断し、年初来安値などのフィルター条件と組み合わせてショートシグナルを出します。

ポジションの手仕舞いについては、固定ストップラインとトレーリングストップの2つの選択肢を提供します。固定ストップラインはより短期間(例:20日)のドンチャンチャネルに基づいてストップ水準を設定します。トレーリングストップは毎日ATR値に基づいて変動するストップラインを計算します。これらのストップ方法はどちらもリスクを適切にコントロールできます。

優位性分析

この戦略はトレンド判断とブレイクアウト操作を組み合わせることで、市場の短期から中期の方向性チャンスを効果的に捉えることができます。単一指標と比較して、複数のフィルター条件を総合的に活用することで、一部の偽ブレイクを除外し、エントリーシグナルの質を向上させます。また、ストップ戦略の適用により耐性も強く、相場が短期的に調整しても損失を効果的に抑えられます。

リスク分析

この戦略の主なリスクは、相場が急激に変動し、ストップがトリガーされてポジションが手仕舞いされる可能性があることです。その際、相場がすぐに反転するとチャンスを逃す恐れがあります。また、複数のフィルター条件を用いることで一部のチャンスが除外され、ポジション保有頻度が低下します。

リスクを低減するには、ATR値を調整したり、ドンチャンチャネルの幅を広げたりすることで、ストップが破られる可能性を減らせます。また、フィルター条件を緩和または削除することでエントリー頻度を高められますが、リスクも増加します。

最適化の方向性

本戦略は以下の点から最適化が可能です:

- ドンチャンチャネルの期間を最適化し、最適なパラメータの組み合わせを探る

- 異なる種類の移動平均線をフィルター指標として試す

- ATR乗数を調整する、または固定ポイントストップに変更する

- MACDなどのトレンド判断指標を追加する

- 年初来高値・安値の判断ウィンドウ期間を最適化する

異なるパラメータをテストすることで、リスクとリターンのバランスが取れた最適なパラメータの組み合わせを見つけることができます。

まとめ

本戦略は複数の指標を組み合わせてトレンド方向を判断し、重要な価格ポイントでのブレイクアウト時に取引シグナルを発します。ストップメカニズムにより、本戦略は強力なリスクコントロール能力を備えています。パラメータ設定を最適化することで、安定した超過収益を実現できます。本戦略は、市場に対して明確な判断を持たないがトレンドに追随したい投資家に適しています。

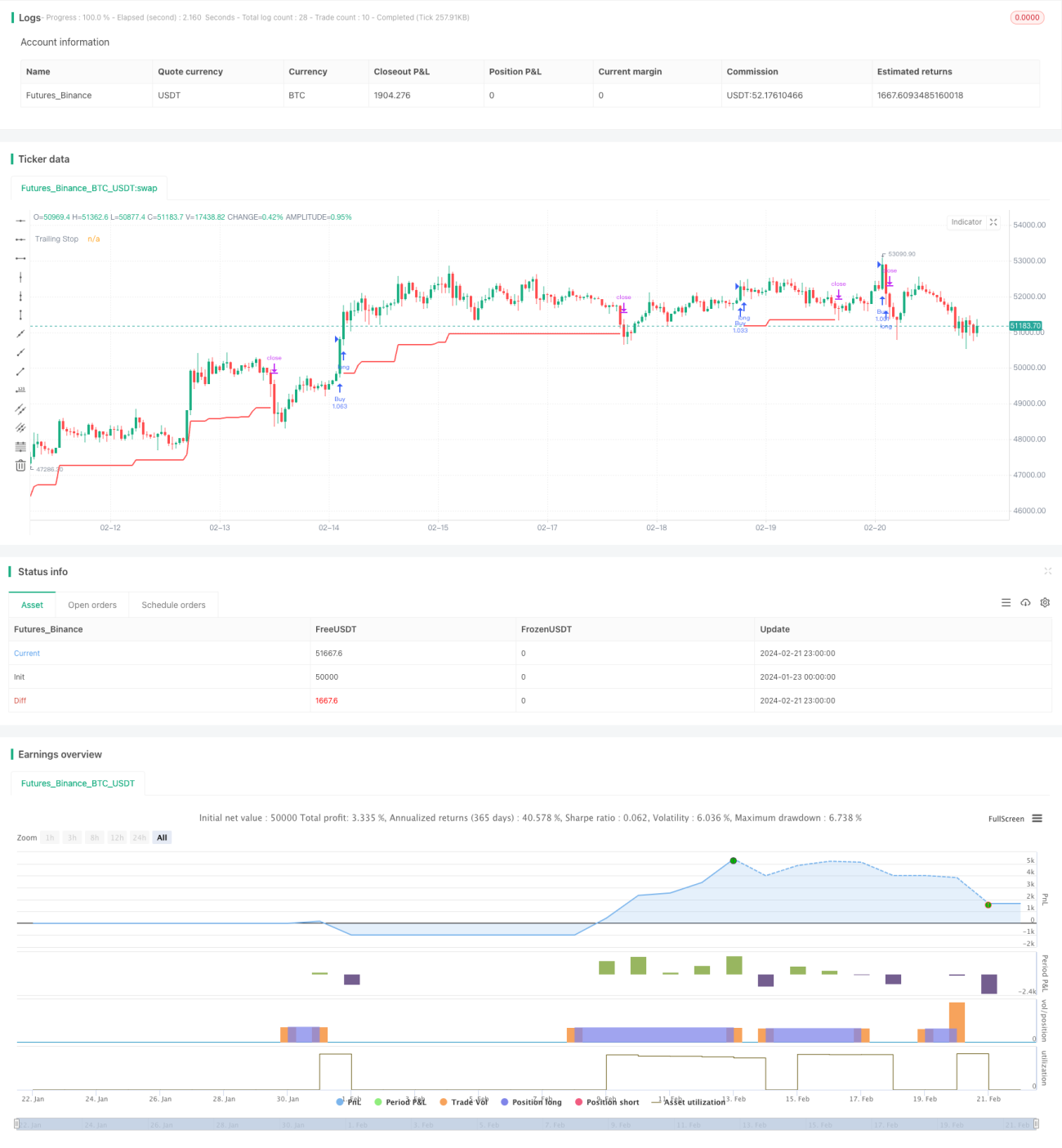

/*backtest

start: 2024-01-23 00:00:00

end: 2024-02-22 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © HeWhoMustNotBeNamed

//@version=4- 1