추세 반전 추적 손절매 전략

개요

이 전략은 추세 반전 지표에 기반하여, 추세 추적 손절 메커니즘을 결합함으로써 추세 시장에서는 추세를 따라가고, 횡보 시장에서는 손실을 줄이는 효과를 구현합니다.

전략 원리

이 전략은 Hull 이동평균선을 주요 추세 판단 지표로 사용합니다. 가격이 Hull 평균선을 상향 돌파하면 매수하고, 하향 돌파하면 매도합니다. 동시에 McGinley 평균선을 결합하여 추세를 확인합니다.

포지션 진입 후, 가격이 반전되어 Hull 평균선이 교차 발생하면 추세 변경 로직을 실행하여 현재 포지션을 청산합니다.

이 전략은 또한 추세 추적 손절 메커니즘을 도입합니다. 포지션 진입 후 ATR에 따라 동적 손절 가격을 계산합니다. 가격 움직임에 따라 손절선도 동적으로 조정되어 이익 추적 손절을 실현합니다.

전략 장점

- Hull 평균선을 사용하여 추세 반전 지점을 판단하며, Hull 평균선은 돌파 신호에 대한 민감도가 높습니다.

- McGinley 평균선을 결합하여 추세를 확인함으로써 일부 거짓 돌파를 걸러낼 수 있습니다.

- 동적 추적 손절 메커니즘을 채택하여 시장 변동성에 따라 손절 폭을 조정할 수 있어 손실을 효과적으로 제어합니다.

- Hull 평균선 검증 시 추세 반전에 신속하게 대응하여 손실 확대를 방지합니다.

- 다양한 매개변수 조합을 쉽게 전환하여 테스트하고 최적의 매개변수를 찾을 수 있습니다.

리스크 및 해결 방안

-

횡보 장세에서 손절이 발동될 가능성이 있습니다.

- 손절 폭을 적절히 확대하고 손절 버퍼를 추가할 수 있습니다.

-

급격한 변동 장세에서 추적 손절이 가격 변동을 따라잡지 못할 수 있습니다.

- 평활 주기를 단축하여 손절이 가격을 더 빠르게 따라가도록 할 수 있습니다.

-

거짓 돌파로 인해 불필요한 손실이 발생할 수 있습니다.

- 다른 지표를 추가하여 확인하고 거짓 돌파를 방지합니다.

-

부적절한 매개변수로 인해 전략 성과가 좋지 않을 수 있습니다.

- 다양한 시장 사이클에 대해 백테스트를 수행하여 최적의 매개변수를 찾을 수 있습니다.

최적화 방안

- 캔들 패턴, 볼린저 밴드, RSI 등 다른 지표를 결합하여 신호 품질을 높입니다.

- 다양한 종목 및 기간 매개변수에 대해 최적화하여 최상의 매개변수 조합을 찾습니다.

- 머신러닝 등의 방법을 시도하여 매개변수 적응형 최적화를 수행할 수 있습니다.

- 손절 알고리즘을 최적화하여 손절을 보장하면서 불필요한 손절을 최소화합니다.

- 자금 관리와 결합하여 포지션 관리 전략을 최적화합니다.

- 자동 이익 실현 메커니즘을 추가하는 것을 고려합니다.

요약

이 전략은 전반적으로 비교적 안정적인 추세 추적 전략입니다. 고정 손절과 달리 이 전략은 동적 손절 메커니즘을 사용하여 시장 변동성에 따라 손절 폭을 조정함으로써 손절이 걸릴 확률을 효과적으로 줄입니다. 또한 Hull 평균선과 추세 변경 로직의 도입으로 추세 반전에 신속하게 대응할 수 있습니다. 그러나 이 전략은 횡보 장세에서의 손절 리스크, 거짓 돌파 리스크 등 일부 리스크도 존재합니다. 지표 매개변수, 손절 알고리즘, 포지션 관리 등을 추가로 최적화함으로써 다양한 시장에서 더 안정적인 성과를 얻을 수 있습니다.

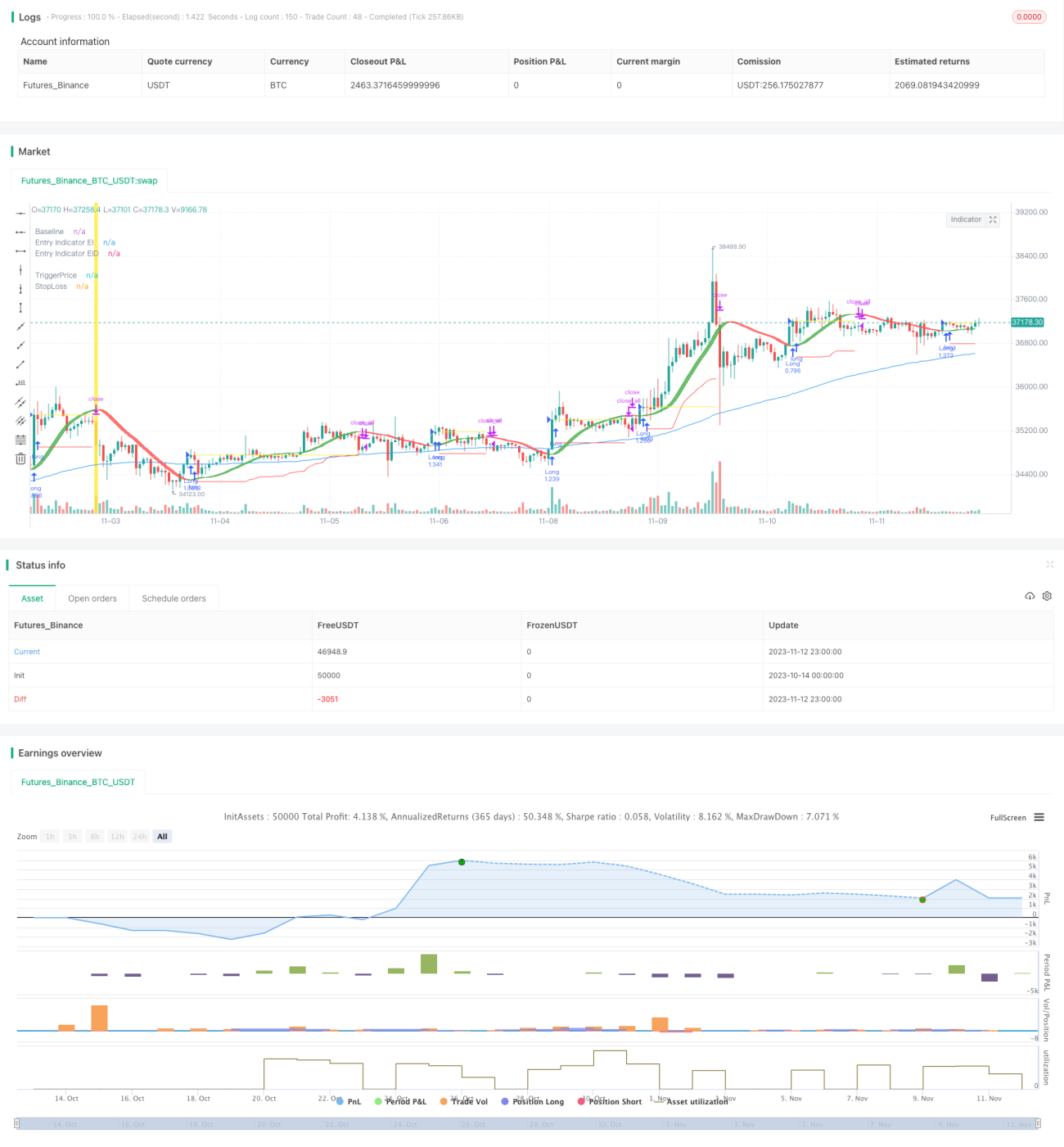

/*backtest

start: 2023-10-14 00:00:00

end: 2023-11-13 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// © Milleman

//@version=4

strategy("MilleMachine", overlay=true, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, initial_capital=10000, commission_type=strategy.commission.percent, commission_value=0.06)

- 1