거북이 돌파 후 되돌림 적응형 거래 전략

개요

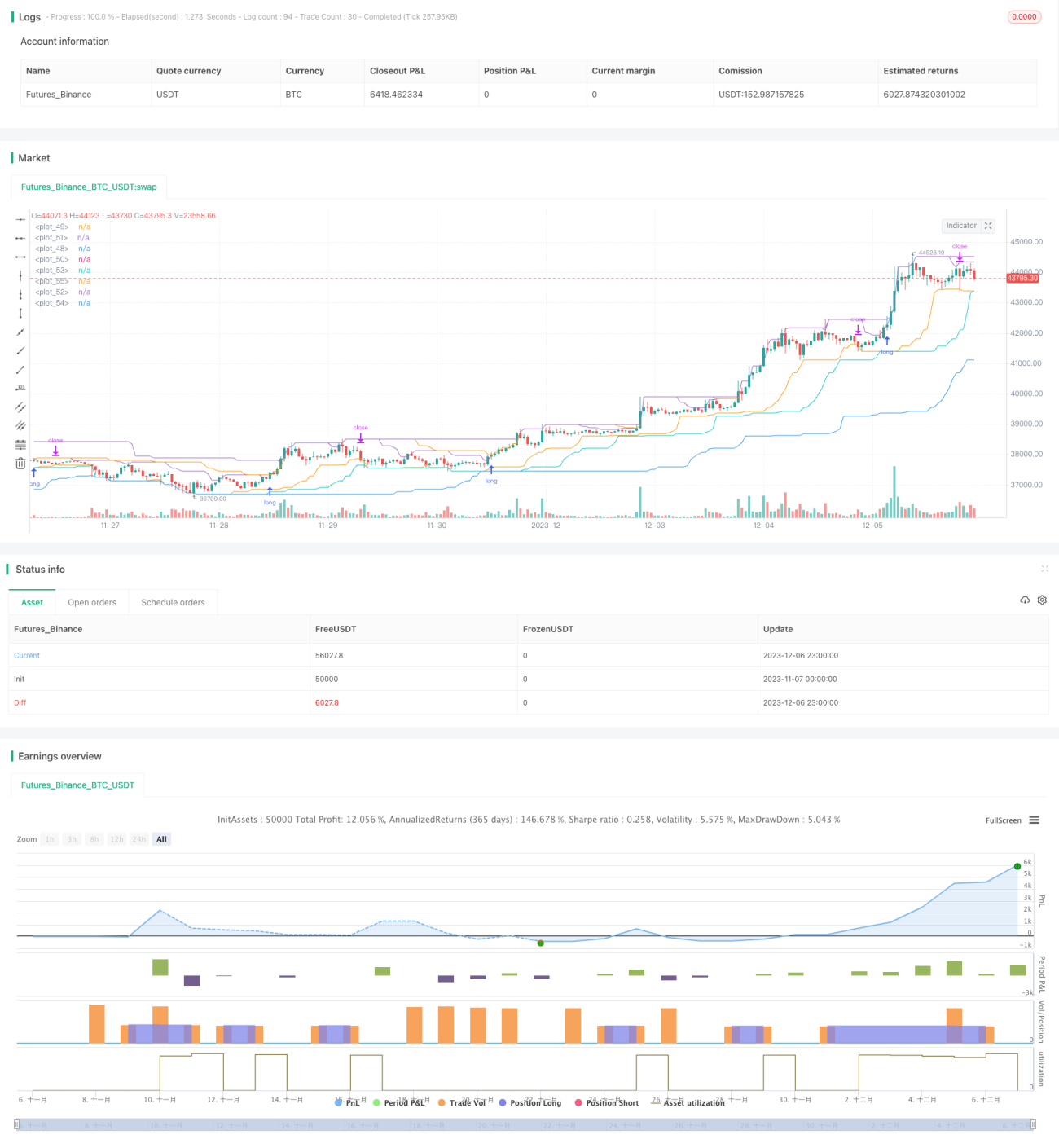

이 전략은 주로 추세 돌파 원리를 기반으로 하며, 채널 돌파 방식을 결합하여 빠른 선과 느린 선의 이중 채널 돌파를 통해 추세 방향을 판단합니다. 전략은 돌파 진입과 되돌림 청산이라는 이중 보호 기능을 동시에 갖추고 있어 급격한 시장 변동에 효과적으로 대응할 수 있습니다. 이 전략의 가장 큰 장점은 계좌의 최대 손실률을 실시간으로 모니터링하여 손실률이 일정 비율을 초과하면 보유 포지션 규모를 능동적으로 줄인다는 점입니다. 이를 통해 시장 위험과 계좌의 위험 대응 능력을 효과적으로 통제할 수 있습니다.

전략 원리

-

빠른 선과 느린 선 이중 채널: 각각 빠른 선과 느린 선을 사용하여 채널을 구성합니다. 빠른 선은 응답 속도가 더 빠르고, 느린 선은 평활도가 더 높습니다. 이중 채널 돌파를 결합하여 추세 방향을 판단합니다.

-

돌파 진입: 가격이 상방 채널을 돌파하면 매수하고, 하방 채널을 돌파하면 매도합니다. 손절매 주문 방식을 사용하여 위험을 최소화합니다.

-

되돌림 청산: 최대 손실률을 실시간 모니터링합니다. 손실률이 되돌림 청산 지점에 도달하면 능동적으로 손절매하여 포지션을 청산합니다. 되돌림 청산 지점은 시장 상황에 따라 조정할 수 있습니다.

-

포지션 규모 적응: 보유 포지션 수량은 계좌 자본에 따라 실시간 조정되어 시장 위험을 회피합니다. 계좌 손실률이 클수록 보유 포지션이 줄어듭니다. 위험 대응 능력이 더욱 강화됩니다.

전략 장점

-

이중 채널 + 돌파 진입으로 추세 판단이 더 정확합니다.

-

손절매 및 이익 실현 메커니즘으로 개별 손실을 효과적으로 통제합니다.

-

계좌 손실률을 실시간 모니터링하고 포지션 규모를 능동적으로 조정하여 시장 위험을 낮춥니다.

-

포지션 규모가 계좌 자본과 연동되어 위험 대응 능력이 강하며, 급격한 시장 변동에 대응할 수 있습니다.

전략 위험

-

큰 변동폭의 횡보장세에서는 손실률 통제가 실패하여 손실이 확대될 수 있습니다.

-

빠른 선이 중립 영역에 진입할 때 여러 번의 무효 돌파 신호가 발생할 수 있습니다.

-

느린 선이 지나치게 평활하여 빠른 추세 반전을 적시에 포착하지 못할 수 있습니다.

-

매수와 매도를 혼합하여 사용할 경우 양방향 포지션 보유에 따른 갇힘 위험이 존재합니다.

전략 최적화 방향

-

큰 변동폭의 횡보장세에서는 더 높은 손실률 허용 범위를 설정하여 과도한 손절매를 방지할 수 있습니다.

-

중립 영역 필터를 추가하여 중립 영역에서의 무효 신호를 방지합니다.

-

느린 선 채널의 매개변수를 최적화하여 빠른 시장 변동에 대한 응답 속도를 높입니다.

-

포지션 진입 순서 규칙을 추가하여 양방향 포지션 보유에 따른 갇힘을 방지합니다.

요약

이 전략은 전반적으로 중장기 추세 거래에 적합한 효과적인 전략입니다. 이 전략의 가장 큰 장점은 실시간 손실률 모니터링과 동적 포지션 조정입니다. 이를 통해 전략이 포지션 규모를 자동으로 조절하여 시장에 대한 강력한 적응 능력을 갖출 수 있습니다. 급격한 시장 변동이나 가격 변동이 발생할 경우 전략이 자동으로 포지션 규모를 줄여 손실 확대를 효과적으로 방지합니다. 이는 많은 전통적인 전략이 달성하기 어려운 점입니다. 전반적으로 이 전략은 참신한 아이디어를 바탕으로 하며 실용성이 높습니다. 탐구하고 최적화하여 적용할 가치가 있습니다.

//Noro

//2020

//Original idea from «Way of the Turtle: The Secret Methods that Turned Ordinary People into Legendary Traders» (2007, CURTIS FAITH, ISBN: 9780071486644)

//@version=4

strategy("Noro's Turtles Strategy", shorttitle = "Turtles str", overlay = true, default_qty_type = strategy.percent_of_equity, initial_capital = 100, default_qty_value = 100, commission_value = 0.1)

//Settings

needlong = input(true, title = "Long")

needshort = input(false, title = "Short")

sizelong = input(100, defval = 100, minval = 1, maxval = 10000, title = "Lot long, %")- 1