볼린저 밴드와 VWAP 기반의 퀀트 트레이딩 전략

개요

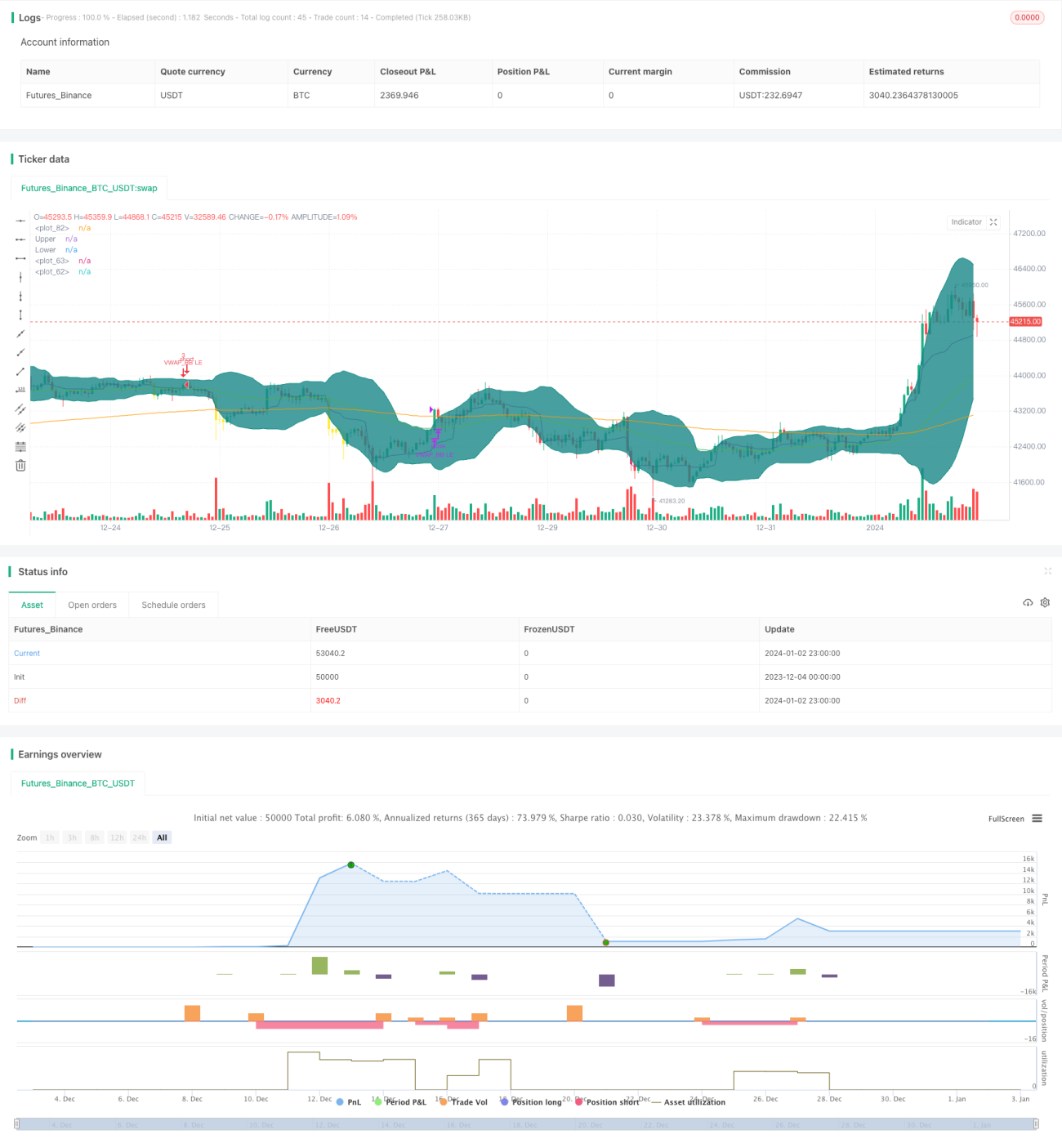

해당 전략은 볼린저 밴드(BB)와 전형적 가격 가중 평균(VWAP)이라는 두 가지 지표를 결합하여 매수 및 매도 결정을 내립니다. 단기적인 가격 이상 징후를 발견하여 거래에 활용하며, 단기 매매에 적합합니다.

전략 원리

이 전략은 주로 다음과 같은 규칙에 따라 매수 및 매도를 실행합니다.

-

빠른 EMA 선이 느린 EMA 선보다 위에 있는 경우를 추세 판단의 선행 조건으로 삼습니다.

-

종가가 VWAP보다 높을 때 가격 상승으로 판단하여 매수합니다.

-

이전 10개 캔들 중 하나라도 종가가 볼린저 밴드 하한선 아래에 있으면 가격 이상으로 판단하여 매수합니다.

-

종가가 볼린저 밴드 상한선보다 높을 때 가격이 반전되었다고 판단하여 매도합니다.

구체적으로, 전략은 먼저 50일 EMA가 200일 EMA보다 높은지 확인하여 단기 및 장기 EMA로 큰 추세를 판단합니다. 그런 다음 VWAP와 결합하여 가격이 단기적으로 상승 추세에 있는지 판단합니다. 마지막으로 볼린저 밴드를 이용해 가격이 단기적으로 비정상적으로 하락했는지 진입 기회로 활용합니다.

청산 규칙은 비교적 간단합니다. 가격이 볼린저 밴드 상한선보다 높을 때 가격이 반전되었다고 판단하고 포지션을 청산합니다.

장점 분석

해당 전략은 여러 지표를 결합하여 가격 이상을 판단함으로써 진입 신호의 효력을 높일 수 있습니다. EMA를 사용한 큰 추세 판단은 역추세 거래를 피하는 데 도움이 됩니다. VWAP와 결합하여 단기적인 가격 상승 기회를 포착할 수 있습니다. 볼린저 밴드를 이용한 가격 이상 판단은 단기 매매 타이밍을 정확하게 찾아낼 수 있습니다.

위험 분석

- EMA가 큰 추세를 정확히 판단하지 못해 시장 전체의 역추세 거래를 초래할 수 있습니다.

- VWAP 지표는 시간봉 또는 당일 데이터에 적용할 때 가장 효과적이며, 일봉 데이터에 적용하면 효과가 떨어질 수 있습니다.

- 볼린저 밴드 매개변수 설정이 적절하지 않아 상하한선이 너무 넓거나 좁으면 신호를 놓칠 수 있습니다.

이러한 위험에 대응하여 EMA 기간 매개변수를 적절히 조정하거나 다른 큰 추세 판단 지표를 시도할 수 있습니다. VWAP 매개변수를 당일 데이터에 적용하거나 다른 단기 지표로 대체할 수 있습니다. 볼린저 밴드 매개변수를 조정하여 최적의 폭을 찾을 수 있습니다.

최적화 방향

- MACD 등 다른 지표로 큰 추세를 판단해 볼 수 있습니다.

- EMA와 볼린저 밴드 매개변수를 최적화하여 최적의 구성을 찾습니다.

- 손절매 메커니즘을 추가합니다.

- 다른 지표와 결합하여 허위 신호를 필터링합니다.

- 다양한 종목과 주기 데이터를 테스트합니다.

요약

해당 전략은 볼린저 밴드와 VWAP 두 지표를 결합하여 단기 가격 이상을 진입 시점으로 판단합니다. EMA를 사용하여 큰 추세를 판단함으로써 역추세 거래를 피합니다. 단기 가격 추세 기회를 신속하게 포착할 수 있습니다. 당일 및 단기 매매에 적합합니다. 매개변수 최적화와 더 많은 판단 지표 추가를 통해 전략의 안정성과 수익성을 더욱 강화할 수 있습니다.

- 1