개요

S&P500 혼합 계절성 트레이딩 전략은 계절적 패턴을 활용하여 주식을 거래하는 퀀트 전략입니다. 이 전략은 강화된 매수 후 보유 시스템, 기술적 지표 조건 및 자금 흐름 지표를 결합하여 한 해 중 성과가 좋은 달과 나쁜 달 사이에서 로테이션을 실행합니다.

전략 원리

전략의 매매 신호 및 규칙은 다음과 같습니다.

- 매년 10월 첫 번째 거래일 개장 시 롱 포지션 진입.

- VIX가 60% 이상이거나 15일 ATR이 90% 이상일 경우, 계절성 거래를 보류하고 시장 변동성이 진정될 때까지 기다린 후 진입.

- 매년 8월 첫 번째 거래일 개장 시 청산.

- VIX가 120%를 초과하거나 자금 흐름 지표 VFI가 -20 이하로 하락하고 10일 이동평균선이 하락할 때도 청산 신호 발생.

- 선택적으로 숏 거래 추가 가능.

이 전략은 주식 시장이 1년 동안 균등하게 움직이지 않는 패턴을 활용하여, 역사적으로 성과가 좋은 10월~4월에는 롱 포지션을 취하고, 성과가 좋지 않은 5월~9월에는 이익 실현 또는 숏 포지션을 통해 역방향 거래를 합니다. 동시에 시장이 크게 변동할 때 거래를 보류하는 기술적 지표 조건을 추가하여 위험을 회피합니다.

장점 분석

S&P500 혼합 계절성 트레이딩 전략의 장점은 다음과 같습니다.

- 성숙하고 안정적인 계절성 패턴 활용. 이 전략은 S&P500 지수가 1년 내에 월별 수익률이 명확히 다른 사실에 기반합니다.

- 다양한 필터 조건 결합. VIX, ATR, VFI 등 여러 조건을 추가하여 노이즈를 효과적으로 걸러내고 보다 신뢰할 수 있는 거래 신호를 생성합니다.

- 구성 가능한 거래 규칙. 롱 또는 숏 거래를 선택할 수 있으며, 거래 월도 필요에 따라 조정 가능하여 테스트 및 최적화가 용이합니다.

- 내장된 위험 회피 메커니즘. VIX 및 ATR 변동성 감지를 통해 시장의 급격한 변동 영향을 효과적으로 회피합니다.

- 자금 흐름 지표 보조 판단. VFI는 시장 참여자의 자금 흐름을 반영하여 전략 결정에 추가 근거를 제공합니다.

위험 분석

S&P500 혼합 계절성 트레이딩 전략에는 잠재적 위험도 존재합니다.

- 역사적 패턴 실패 위험. 주식 시장은 불확실성이 크므로 역사적 패턴이 항상 유효하다고 볼 수 없습니다.

- 기술적 지표 오신호 위험. VIX, ATR, VFI 등 지표도 오판할 가능성이 있습니다.

- 파라미터 최적화 미비 위험. 전략 파라미터는 추가 테스트 및 최적화가 필요하며, 현재 파라미터가 최적이 아닐 수 있습니다.

- 숏 거래로 인한 추가 위험. 선택적 숏 거래는 무한 손실 위험을 초래할 수 있습니다.

위험 관리, 지표 조합, 파라미터 조정, 머신러닝 도입 등을 통해 전략을 강화하고 위험을 해결할 수 있습니다.

최적화 방향

S&P500 혼합 계절성 트레이딩 전략은 다음과 같은 측면에서 추가 최적화가 가능합니다.

- 더 긴 과거 데이터 테스트. 더 많은 과거 데이터를 사용하여 전략 파라미터를 재테스트 및 최적화합니다.

- 손절 메커니즘 추가. 트레일링 스탑 또는 시간 기반 손절을 설정하여 개별 손실을 효과적으로 제어합니다.

- 기술적 지표 파라미터 최적화. VIX, ATR, VFI의 파라미터를 조정하여 최적의 조합을 찾습니다.

- 머신러닝 모델 도입. 신경망 또는 의사결정 트리를 사용하여 파라미터 자체 적응 최적화를 수행합니다.

- 전략 조합. 다른 전략과 조합하여 비상관성을 활용해 시장 시스템 리스크를 낮춥니다.

요약

S&P500 혼합 계절성 트레이딩 전략은 검증된 계절성 패턴, 기술적 지표 조건 및 자금 흐름 지표를 종합적으로 활용합니다. 이 전략은 주식 시장의 성과가 가장 나쁜 몇 달을 회피하고, 성과가 좋은 거래 월에 포지션을 배분하며, 효과적인 시장 변동성 필터 메커니즘을 내장하여 안정적인 초과 수익을 창출할 수 있습니다. 또한 전략은 테스트, 최적화 및 조정이 용이하여 퀀트 트레이더가 참고하고 재개발할 수 있는 프레임워크를 제공합니다. 더 많은 데이터, 손절 조치, 파라미터 조정 및 조합 방법을 도입하면 전략의 효과를 더욱 강화할 수 있습니다.

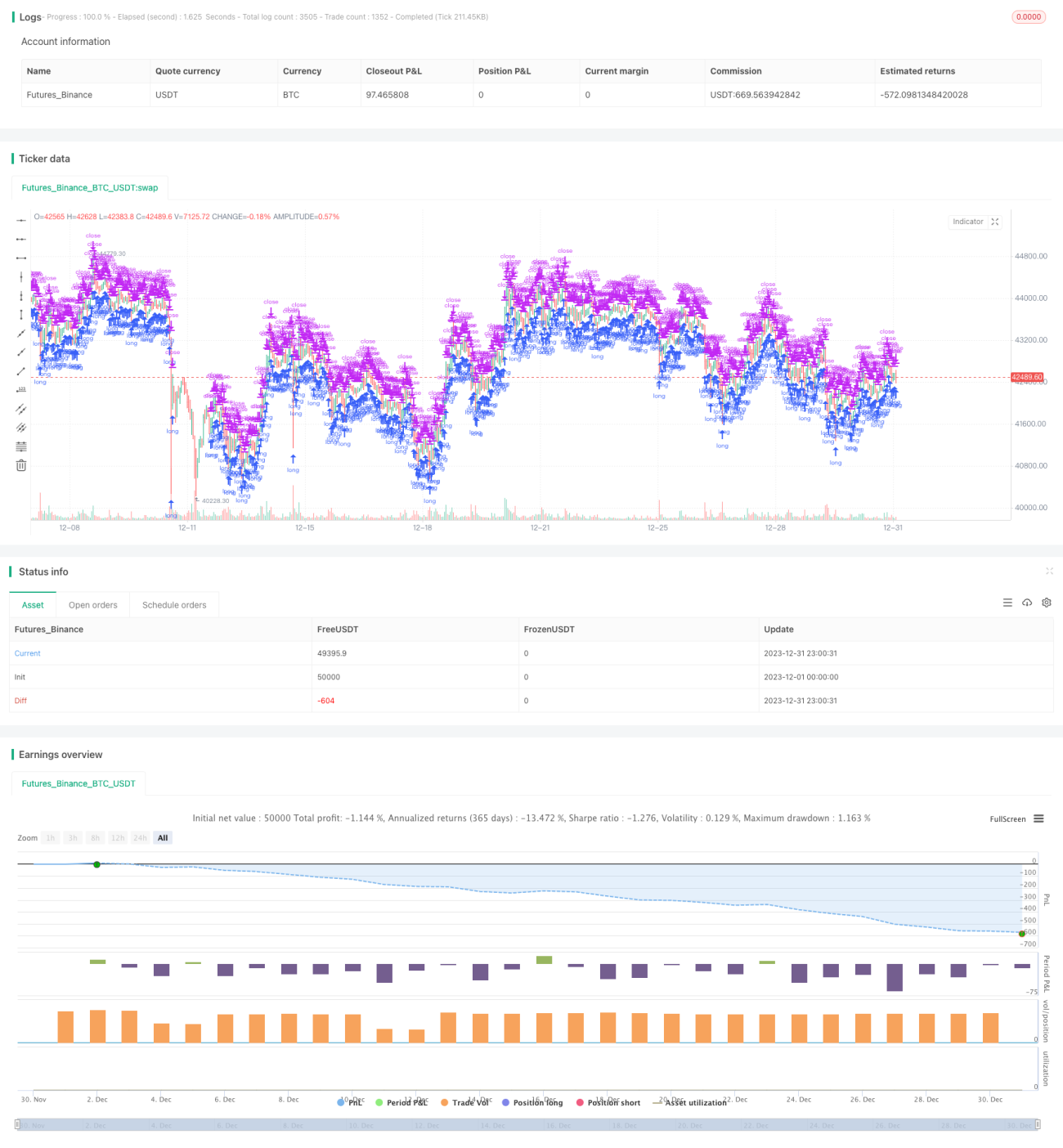

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// TASC Issue: April 2022 - Vol. 40, Issue 4

// Article: Sell In May? Stock Market Seasonality

// Article By: Markos Katsanos

// Language: TradingView's Pine Script v5- 1