다중 지표 기반의 추세 추종 전략

개요

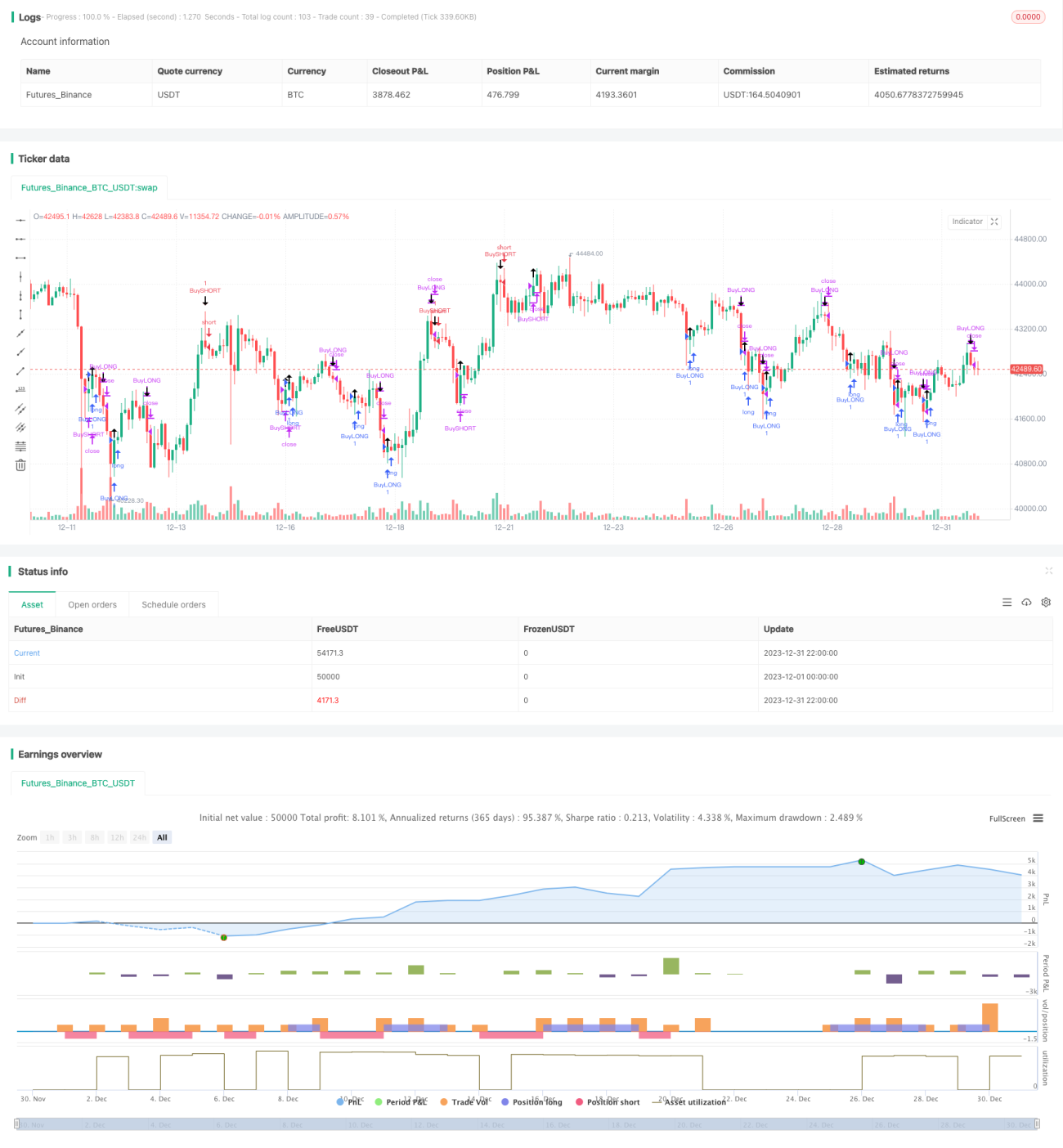

이 전략은 여러 지표를 결합하여 추세를 식별하고, 추세 추적 손절매를 설정하여 이익을 확보합니다. 주로 볼린저 밴드, RSI, ADX 등의 지표로 진입 시점을 판단하고, ATR과 볼린저 밴드로 손절매를 수행합니다.

전략 원리

전략의 주요 판단 지표는 볼린저 밴드, RSI 및 ADX입니다. 가격이 볼린저 밴드 하단에 근접하고 RSI가 30 미만일 때 과매도로 판단하여 매수하고, 가격이 볼린저 밴드 상단에 근접하고 RSI가 70 초과일 때 과매수로 판단하여 매도합니다. 또한 ADX가 25 이상이면 추세가 형성된 것으로 판단하여, 이때 매수/매도 신호가 더 효과적입니다.

포지션 진입 후, 전략은 ATR 지표와 볼린저 밴드 상하단을 사용하여 손절매를 수행합니다. 구체적으로, ATR은 최대 손절매 폭에 사용되며, 가격이 최대 손절매 지점에 도달하면 손절매합니다. 볼린저 밴드 상하단은 추적 손절매 지점 설정에 사용되며, 가격 움직임에 따라 추적 손절매 가격을 실시간으로 업데이트합니다.

장점 분석

이 전략은 여러 지표를 결합하여 판단함으로써 추세를 효과적으로 식별하고, 손절매 메커니즘을 사용하여 이익을 확보하고 손실 위험을 낮추므로 비교적 안정적인 전략입니다. 구체적인 장점은 다음과 같습니다.

- 볼린저 밴드를 사용하여 과매수/과매도 상황을 판단하여 반전 기회를 식별

- RSI 지표를 결합하여 판단 정확도 향상

- ADX 지표로 추세 형성을 판단하여 거래 방향의 정확성 확보

- ATR과 볼린저 밴드 추적 손절매로 이익을 최대한 확보

위험 분석

이 전략에도 일부 위험이 존재합니다:

- 여러 지표 판단으로 인해 매개변수 설정이 과최적화되기 쉬움

- 볼린저 밴드 폭이 넓을 때 과매수/과매도 신호 효과가 낮음

- 손절매 추적이 부적절할 경우 손실 확대 가능

이러한 위험에 대해 다음과 같은 조치를 취할 수 있습니다:

- 다양한 조합의 매개변수 최적화를 통해 과최적화 방지

- 시장 변동성에 따라 볼린저 밴드 매개변수 조정

- 손절매 거리 매개변수 테스트를 통해 정상적인 변동성을 견딜 수 있도록 보장

최적화 방향

이 전략은 다음과 같은 방향으로 최적화할 수 있습니다:

- 포지션 규모 조절 추가: 손절매 승수에 따라 포지션 크기 조정

- 자금 관리 모듈 추가: 단일 손절매 한도를 엄격히 통제

- DMI, Envelop 등 다른 손절매 지표 테스트

- 머신러닝 모델을 추가하여 추세 확률 판단, 효과 향상

요약

이 전략은 전반적으로 비교적 안정적인 추세 추적 전략입니다. 여러 지표 판단을 통해 추세 방향을 결정하고 손절매 조치를 통해 위험을 통제함으로써 비교적 좋은 수익률을 얻을 수 있습니다. 또한 여러 최적화 방향을 제시했으며, 추가 최적화를 통해 더 나은 효과를 얻을 수 있습니다.

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

// THIS SCRIPT IS MEANT TO ACCOMPANY COMMAND EXECUTION BOTS

// THE INCLUDED STRATEGY IS NOT MEANT FOR LIVE TRADING

// THIS STRATEGY IS PURELY AN EXAMLE TO START EXPERIMENTATING WITH YOUR OWN IDEAS- 1