동적 RSI 지표 거래 전략

개요

본 전략은 RSI 지표를 계산하고 과매수/과매도 구간을 설정한 후, 동적 손절 및 목표 수익 청산을 결합하여 트레이딩 전략을 구성합니다. RSI 지표가 과매도 구간을 상향 돌파하면 매도하고, 과매수 구간을 하향 돌파하면 매수하며, 동시에 추적 손절 및 목표 수익을 설정하여 포지션을 청산합니다.

전략 원리

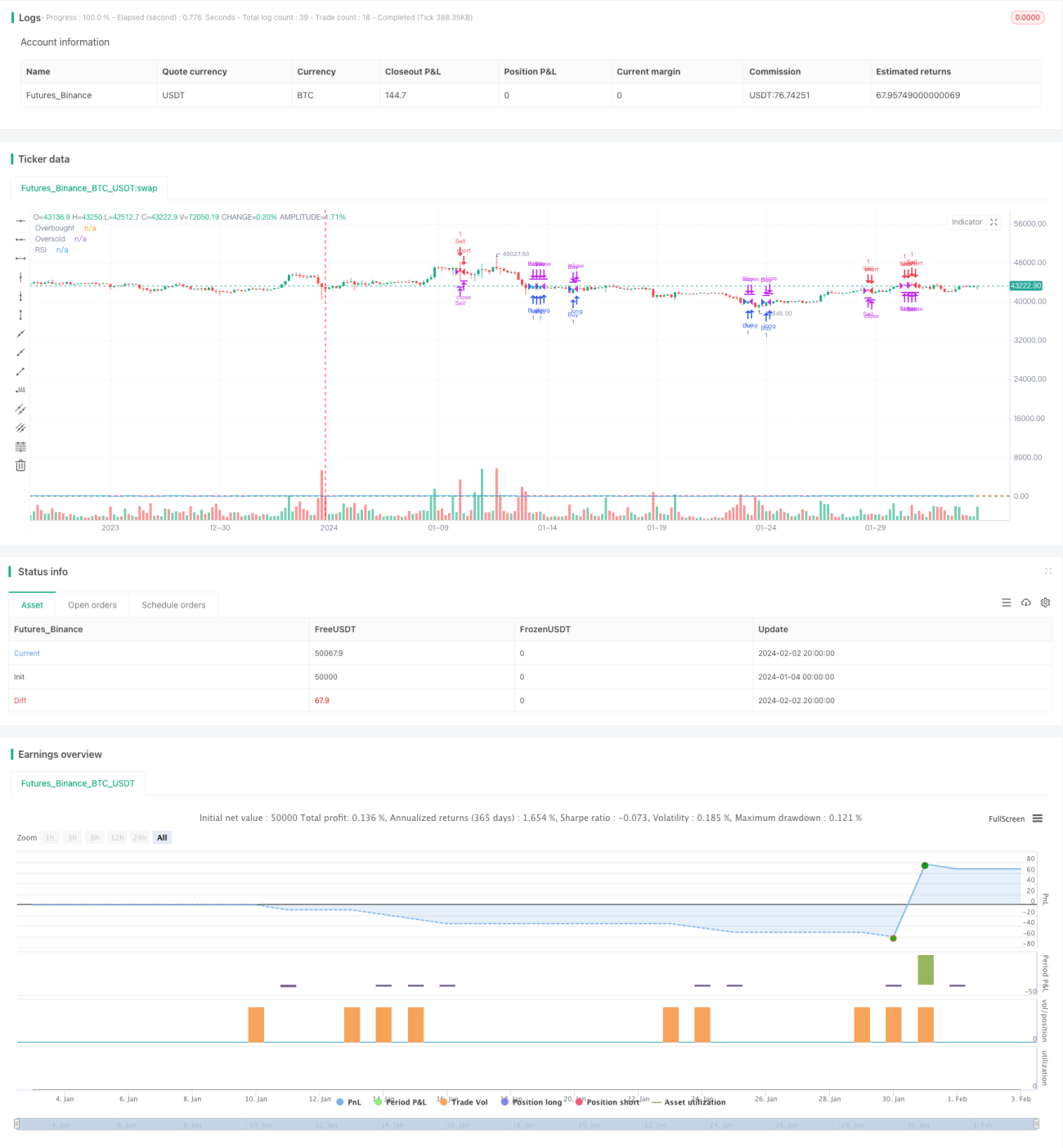

본 전략은 14일 RSI 지표를 사용하여 시장의 기술적 형태를 판단합니다. RSI 지표는 일정 기간 동안의 상승/하락 모멘텀 비율을 반영하여 시장이 과매수인지 과매도인지 판단하는 데 사용됩니다. 본 전략의 RSI 기간은 14입니다. RSI가 70을 상향 돌파하면 시장이 과매수 상태로 간주되어 매도하고, RSI가 30을 하향 돌파하면 시장이 과매도 상태로 간주되어 매수합니다.

또한 본 전략은 동적 추적 손절 메커니즘을 사용합니다. 매수 포지션을 보유할 때 추적 손절 가격은 종가의 97%이고, 매도 포지션을 보유할 때 추적 손절 가격은 종가의 103%입니다. 이를 통해 대부분의 이익을 확보하면서도 손절이 흔들려 빠져나가는 것을 방지할 수 있습니다.

마지막으로 본 전략은 목표 수익 메커니즘도 사용합니다. 포지션 수익률이 20%에 도달하면 포지션을 청산합니다. 이를 통해 일부 이익을 확보하고 이익이 다시 줄어드는 것을 방지할 수 있습니다.

장점 분석

본 전략은 다음과 같은 장점이 있습니다:

- RSI 지표를 사용하여 과매수/과매도 상황을 판단하여 시장의 전환점을 적시에 포착할 수 있습니다.

- 동적 추적 손절을 채택하여 리스크를 효과적으로 관리할 수 있습니다.

- 목표 수익 수준을 설정하여 일부 이익을 확보할 수 있습니다.

- 전략 로직이 명확하고 이해하기 쉬우며, 매개변수가 적어 실전 운용에 편리합니다.

- RSI 기간, 과매수/과매도 수준, 손절 폭 등의 매개변수를 쉽게 최적화할 수 있습니다.

리스크 분석

본 전략에는 주의해야 할 몇 가지 리스크도 있습니다:

- RSI 지표가 가짜 신호를 생성할 가능성이 있어 불필요한 손실로 이어질 수 있습니다.

- 손절이 돌파될 확률이 있어 손실이 확대될 수 있습니다.

- 목표 수익 설정이 너무 낮아 충분한 이익을 보유하며 벌지 못할 수 있습니다.

위 리스크는 RSI 매개변수 최적화, 손절 폭 조정, 목표 수익 요건을 적절히 완화함으로써 해결할 수 있습니다.

최적화 방향

본 전략은 다음과 같은 방향으로 최적화할 수 있습니다:

- RSI 지표 매개변수를 최적화하고 과매수/과매도 판단 기준을 조정하여 가짜 신호 확률을 낮춥니다.

- 다른 지표 필터를 추가하여 RSI 단일 지표로 인한 오류 신호를 방지합니다.

- 목표 수익 수준을 동적으로 최적화하여 전략이 시장 상황에 따라 유연하게 조정될 수 있도록 합니다.

- 거래량 지표를 결합하여 저량 가짜 돌파를 방지합니다.

- 머신러닝 알고리즘을 추가하여 매개변수를 자동으로 최적화합니다.

요약

본 전략은 전체적으로 명확한 로직을 가지고 있으며, RSI 지표를 사용하여 과매수/과매도를 판단하고 동적 손절 및 목표 수익 청산을 결합합니다. 장점은 이해하고 구현하기 쉬우며, 리스크 관리가 적절하고 확장성이 뛰어납니다. 다음 단계로 신호 품질 향상, 매개변수 동적 조정 등의 방향으로 최적화하여 전략을 더욱 지능화할 수 있습니다.

- 1