Strategi Terobosan Volatiliti Dinamik

Gambaran Keseluruhan

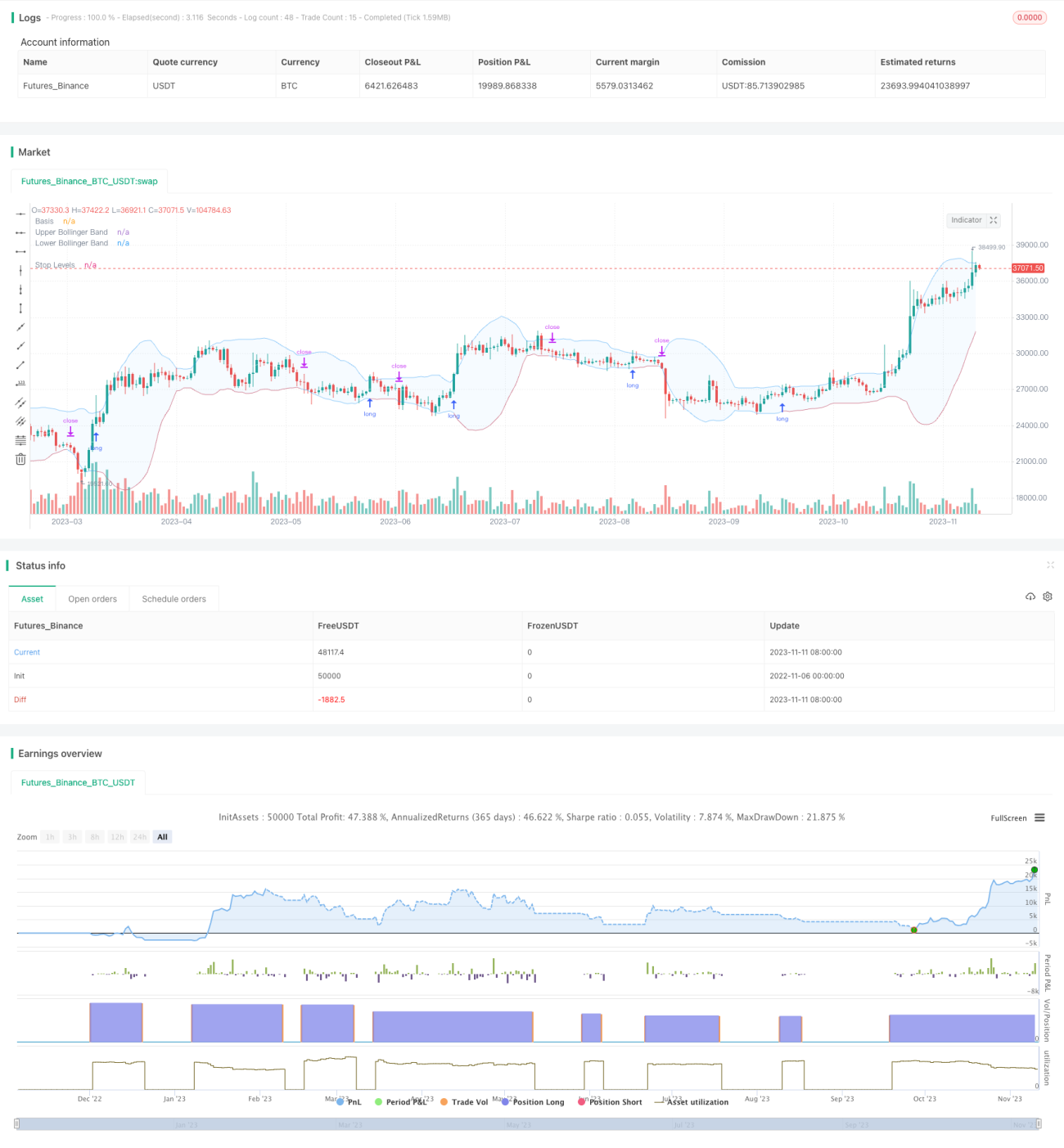

Strategi ini menggunakan jalur atas dan bawah Bollinger Bands yang dinamik untuk melaksanakan posisi beli apabila harga menembusi jalur atas, dan menutup posisi apabila harga jatuh di bawah jalur bawah. Berbeza dengan strategi penembusan tradisional, jalur atas dan bawah Bollinger Bands berubah secara dinamik berdasarkan turun naik sejarah, membolehkan penilaian yang lebih baik terhadap keadaan terlebih beli dan terlebih jual pasaran.

Prinsip Strategi

Strategi ini bergantung terutamanya pada penunjuk Bollinger Bands untuk menentukan penembusan harga. Bollinger Bands terdiri daripada tiga garisan:

- Garisan tengah: Purata bergerak n hari

- Jalur atas: Garisan tengah + k * sisihan piawai n hari

- Jalur bawah: Garisan tengah - k * sisihan piawai n hari

Apabila harga meningkat melebihi jalur atas, pasaran dianggap berada dalam keadaan terlebih beli, dan posisi beli boleh diambil. Apabila harga jatuh di bawah jalur bawah, pasaran dianggap berada dalam keadaan terlebih jual, dan posisi harus ditutup.

Strategi ini membolehkan penyesuaian parameter Bollinger Bands: panjang garisan tengah n dan gandaan sisihan piawai k. Panjang garisan tengah lalai ialah 20 hari, dan gandaan sisihan piawai ialah 2.

Pada setiap hari selepas pasaran ditutup, strategi akan memeriksa sama ada harga penutup hari tersebut menembusi jalur atas. Jika ya, isyarat beli akan dilaksanakan semasa pembukaan pada hari berikutnya. Selepas posisi beli diambil, harga akan dipantau secara masa nyata untuk melihat sama ada ia menembusi jalur bawah; jika ya, posisi akan ditutup.

Strategi ini juga memperkenalkan penapis purata bergerak, di mana isyarat beli hanya akan dijana apabila harga berada di atas purata bergerak. Pengguna boleh memilih untuk melukis purata bergerak pada kitaran semasa atau kitaran yang lebih tinggi untuk mengawal masa kemasukan.

Kaedah henti rugi juga menyediakan dua pilihan: henti rugi peratusan tetap atau mengikut jalur bawah Bollinger Bands. Yang terakhir menyediakan ruang yang lebih besar untuk keuntungan bergerak.

Kelebihan Strategi

- Menggunakan Bollinger Bands untuk menentukan keadaan SUPERBUY/SUPERSELL pasaran

- Penapis purata bergerak untuk mengelakkan dagangan menentang arah aliran

- Parameter Bollinger Bands boleh disesuaikan untuk menyesuaikan kitaran yang berbeza

- Menyediakan dua pilihan kaedah henti rugi

- Menyokong pengoptimuman parameter melalui ujian semula dan pengesahan strategi dalam dagangan sebenar

Risiko Strategi

- Bollinger Bands tidak dapat menentukan keadaan terlebih beli/terlebih jual dengan sempurna

- Penapis purata bergerak mungkin terlepas peluang penembusan yang pantas

- Henti rugi tetap mungkin terlalu konservatif, manakala henti rugi mengikut mungkin terlalu agresif

- Parameter perlu dioptimumkan untuk menyesuaikan instrumen dan kitaran yang berbeza

- Tidak dapat mengehadkan saiz kerugian; pengurusan modal perlu dipertimbangkan

Pengoptimuman Strategi

- Menguji kombinasi parameter purata bergerak yang berbeza

- Mencuba parameter Bollinger Bands yang berbeza

- Membandingkan pulangan antara henti rugi peratusan tetap dan henti rugi mengikut jalur bawah

- Menambah modul pengurusan modal untuk mengehadkan kerugian setiap dagangan

- Menggabungkan penunjuk lain untuk mengesahkan isyarat Bollinger Bands

Kesimpulan

Strategi ini menggunakan jalur atas dan bawah Bollinger Bands yang dinamik untuk menentukan keadaan terlebih beli dan terlebih jual, merujuk penapis purata bergerak untuk isyarat, dan menggunakan henti rugi untuk melindungi modal. Berbanding dengan penembusan jalur tetap tradisional, strategi ini lebih mampu menyesuaikan diri dengan turun naik pasaran. Melalui pengoptimuman parameter dan kawalan risiko, kestabilan dan pulangan strategi dapat dipertingkatkan lagi. Secara keseluruhan, strategi ini memanfaatkan ciri dinamik Bollinger Bands untuk mendapatkan kelebihan strategi penembusan, dan ia patut diuji dalam dagangan sebenar serta dioptimumkan secara berterusan untuk jangka masa panjang.

- 1