Strategi Henti Rugi Mengekori Pembalikan Trend

Gambaran Keseluruhan

Strategi ini berdasarkan penunjuk pembalikan arah aliran, digabungkan dengan mekanisme henti rugi penjejakan arah aliran, untuk mengikuti arah aliran dalam pasaran yang sedang bertrend dan mengurangkan kerugian dalam pasaran yang mendatar.

Prinsip Strategi

Strategi ini menggunakan Purata Bergerak Hull (Hull Moving Average) sebagai penunjuk utama untuk menentukan arah aliran. Apabila harga menembusi ke atas Purata Bergerak Hull, posisi beli dibuka; apabila harga menembusi ke bawah Purata Bergerak Hull, posisi jual dibuka. Pada masa yang sama, Purata Bergerak McGinley digunakan bersama untuk mengesahkan arah aliran.

Selepas posisi dibuka, jika harga berbalik arah, iaitu apabila berlaku persilangan pada Purata Bergerak Hull, logik perubahan arah aliran akan dilaksanakan, menutup posisi semasa.

Strategi ini juga menggabungkan mekanisme henti rugi penjejakan arah aliran. Selepas posisi dibuka, tahap henti rugi dinamik dikira berdasarkan ATR. Apabila harga bergerak, garis henti rugi juga akan menyesuaikan secara dinamik, membolehkan penjejakan henti rugi untuk mengunci keuntungan.

Kelebihan Strategi

- Menggunakan Purata Bergerak Hull untuk menentukan titik pembalikan arah aliran, di mana Purata Bergerak Hull sensitif terhadap isyarat penembusan.

- Menggabungkan Purata Bergerak McGinley untuk mengesahkan arah aliran, menapis sebahagian isyarat penembusan palsu.

- Mengguna pakai mekanisme henti rugi penjejakan dinamik yang boleh menyesuaikan lebar henti rugi berdasarkan turun naik pasaran, mengawal kerugian dengan berkesan.

- Bertindak balas dengan cepat terhadap pembalikan arah aliran apabila Purata Bergerak Hull disahkan, mengelakkan kerugian daripada terus meluas.

- Membolehkan penukaran parameter yang mudah untuk diuji dalam kombinasi berbeza bagi mencari parameter optimum.

Risiko dan Penyelesaian

-

Dalam pasaran yang berombak, henti rugi mungkin tercetus.

- Boleh meluaskan sedikit jurang henti rugi atau menambah zon penampan henti rugi.

-

Dalam pasaran yang sangat bergejolak, henti rugi penjejakan mungkin tidak dapat mengikuti perubahan harga.

- Boleh memendekkan kitaran pelicinan supaya henti rugi dapat mengikuti harga dengan lebih pantas.

-

Penembusan palsu boleh menyebabkan kerugian yang tidak perlu.

- Tambah penunjuk lain untuk pengesahan bagi mengelakkan penembusan palsu.

-

Parameter yang tidak sesuai boleh menyebabkan prestasi strategi yang lemah.

- Boleh melakukan ujian semula dalam kitaran pasaran yang berbeza untuk mencari parameter terbaik.

Idea Pengoptimuman

-

Menambah penunjuk lain untuk pengesahan bersama, seperti corak lilin, Bollinger Bands, RSI, dan lain-lain, untuk meningkatkan kualiti isyarat.

-

Optimumkan berdasarkan parameter yang berbeza untuk instrumen dan jangka masa yang berbeza, untuk mencari kombinasi parameter terbaik.

-

Boleh mencuba kaedah pembelajaran mesin untuk pengoptimuman parameter adaptif.

-

Optimumkan algoritma henti rugi, sambil mengekalkan perlindungan henti rugi, kurangkan henti rugi yang tidak perlu.

-

Gabungkan pengurusan modal untuk mengoptimumkan strategi saiz posisi.

-

Pertimbangkan untuk menambah mekanisme ambil untung automatik.

Kesimpulan

Secara keseluruhannya, strategi ini adalah strategi penjejakan arah aliran yang agak kukuh. Berbanding henti rugi tetap, strategi ini menggunakan mekanisme henti rugi dinamik yang boleh menyesuaikan lebar henti rugi berdasarkan turun naik pasaran, dengan berkesan mengurangkan kebarangkalian henti rugi terperangkap. Pada masa yang sama, pengenalan Purata Bergerak Hull dan logik perubahan arah aliran membolehkan respons yang lebih pantas terhadap pembalikan arah aliran. Walau bagaimanapun, strategi ini juga mempunyai risiko tertentu, seperti risiko henti rugi dalam pasaran berombak, risiko penembusan palsu, dan lain-lain. Dengan pengoptimuman lanjut pada parameter penunjuk, algoritma henti rugi, pengurusan posisi, dan lain-lain, strategi ini boleh mencapai prestasi yang lebih stabil dalam pasaran yang berbeza.

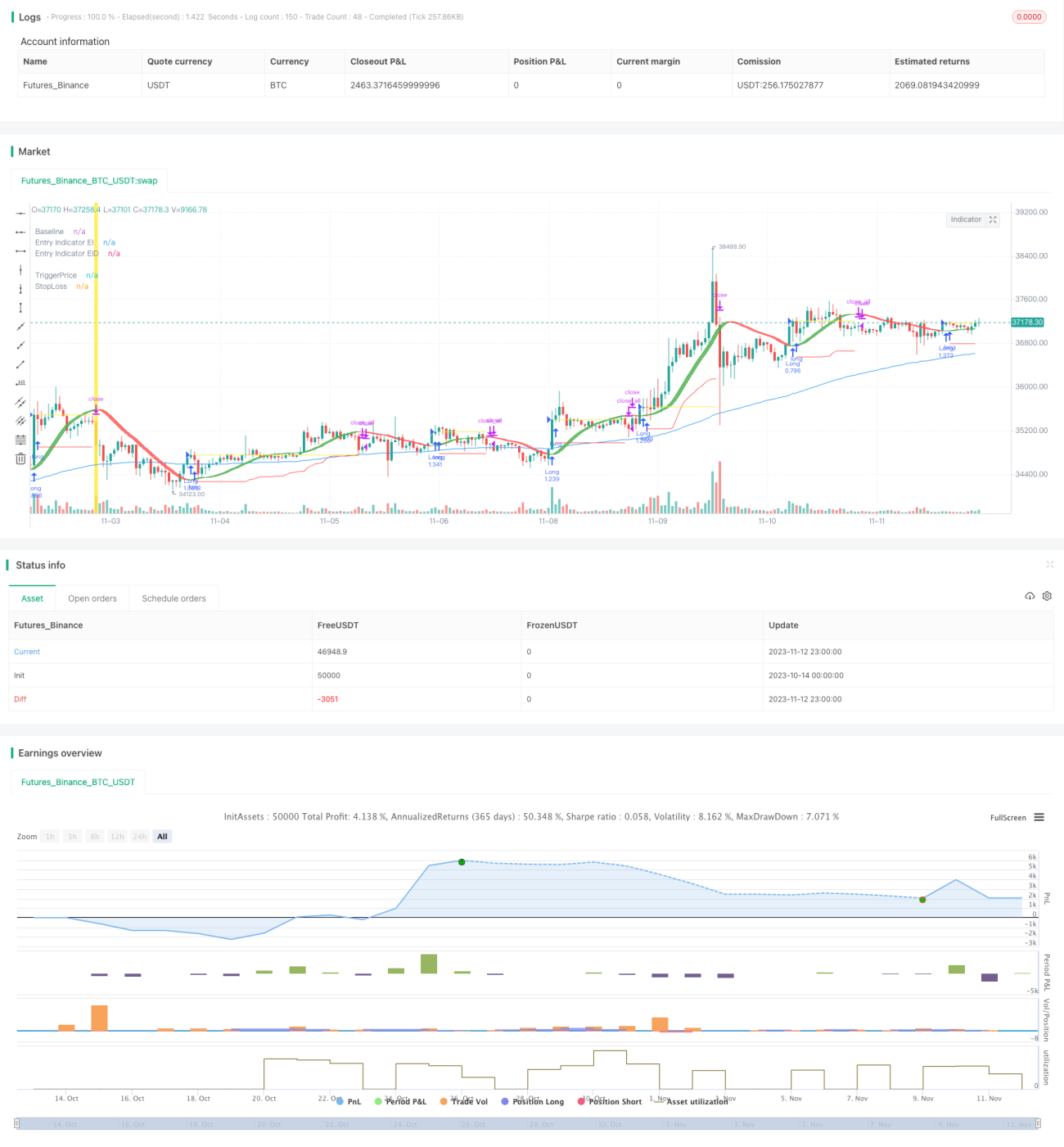

/*backtest

start: 2023-10-14 00:00:00

end: 2023-11-13 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// © Milleman

//@version=4

strategy("MilleMachine", overlay=true, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, initial_capital=10000, commission_type=strategy.commission.percent, commission_value=0.06)

- 1