Strategi Penghentian Kerugian Pengesanan Trend Berdasarkan TFO dan ATR

Gambaran Keseluruhan

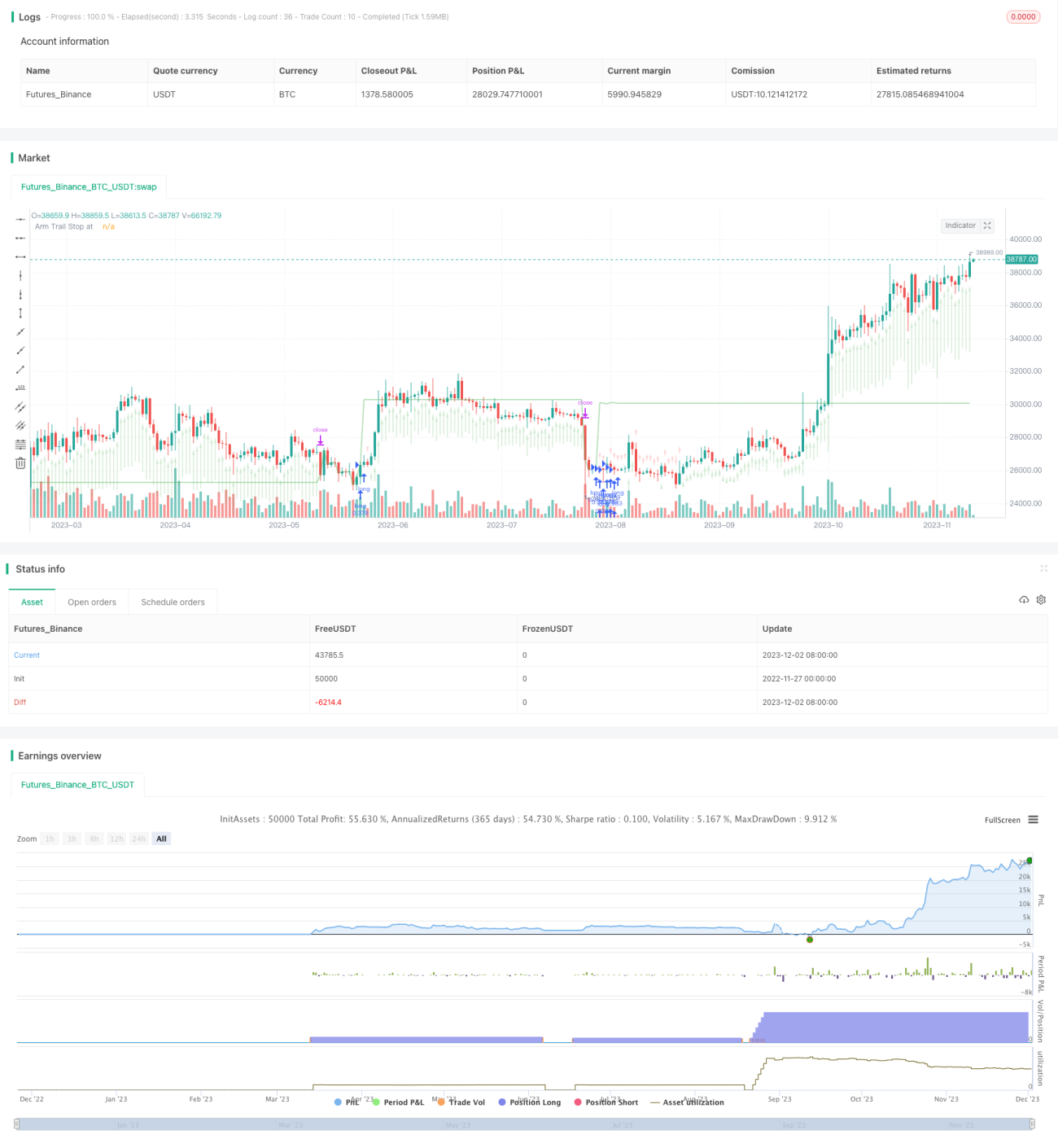

Strategi ini adalah strategi hentian rugi berdasarkan penjejakan arah aliran yang direka menggunakan Osilator Fleksibel Trend (TFO) oleh Dr. John Ehlers dan penunjuk Purata Julat Sebenar (ATR). Ia sesuai untuk pasaran menaik, dan akan membuka kedudukan beli apabila harga berbalik selepas keadaan terlebih jual. Biasanya ia akan menutup kedudukan dalam beberapa hari, melainkan ia terperangkap dalam pasaran menurun, di mana ia akan bertahan pada kedudukan tersebut. Strategi ini melaraskan parameter yang boleh dikonfigurasikan melalui ujian belakang yang mudah, tetapi hasil ujian belakang tidak boleh dipercayai sepenuhnya.

Prinsip Strategi

Strategi ini menggabungkan dua penunjuk TFO dan ATR, membuka kedudukan beli apabila syarat pembelian dipenuhi, dan menutup kedudukan apabila syarat penjualan dipenuhi.

Syarat pembelian: Apabila TFO berada di bawah ambang tertentu (menunjukkan terlebih jual), dan nilai TFO pada lilin sebelumnya lebih rendah daripada lilin semasa (menunjukkan TFO berbalik naik), serta ATR berada di atas ambang turun naik yang ditetapkan (menunjukkan peningkatan turun naik pasaran), maka ketiga-tiga syarat ini akan membuka kedudukan beli.

Syarat penutupan: Apabila TFO berada di atas ambang tertentu (menunjukkan terlebih beli), dan ATR berada di atas ambang yang ditetapkan, maka semua kedudukan beli akan ditutup. Selain itu, strategi ini juga menetapkan hentian rugi menjejak, di mana semua kedudukan beli akan ditutup jika harga jatuh di bawah paras hentian rugi yang ditetapkan. Pengguna boleh memilih sama ada strategi akan menutup kedudukan berdasarkan isyarat penunjuk, atau hanya berdasarkan paras hentian rugi.

Strategi ini boleh membuka sehingga 15 kedudukan beli secara serentak. Parameternya boleh dilaraskan dan sesuai untuk jangka masa yang berbeza.

Kelebihan Strategi

-

Menggabungkan arah aliran dan turun naik untuk menilai arah pasaran, menjadikannya lebih stabil. TFO dapat menangkap isyarat awal penembusan arah aliran, manakala ATR dapat mengenal pasti masa apabila turun naik pasaran meningkat.

-

Mempunyai parameter beli dan jual yang boleh dilaraskan serta parameter hentian rugi, menawarkan fleksibiliti operasi. Pengguna boleh melaraskan parameter mengikut pasaran untuk mencapai pengoptimuman.

-

Dilengkapi dengan fungsi hentian rugi untuk mengurangkan kerugian dalam keadaan pasaran ekstrem. Strategi hentian rugi adalah bahagian yang sangat penting dalam perdagangan kuantitatif.

-

Menyokong penambahan kedudukan dan penutupan separa, membolehkan keuntungan diperbesarkan dengan meningkatkan saiz kedudukan. Sesuai untuk pasaran menaik.

Risiko Strategi

-

Strategi ini hanya mengambil kedudukan beli, tidak menjual pendek, jadi ia tidak dapat menjana keuntungan dalam pasaran menurun. Jika berdepan dengan pasaran menurun yang teruk, ia boleh menyebabkan kerugian besar.

-

Tetapan parameter yang tidak sesuai boleh menyebabkan perdagangan berlebihan atau terlepas beli/jual. Ujian berulang diperlukan untuk mencari kombinasi parameter terbaik.

-

Dalam keadaan pasaran ekstrem, hentian rugi mungkin tidak berkesan dan gagal menghalang kerugian besar. Ini adalah masalah yang dihadapi oleh semua strategi hentian rugi.

-

Ujian belakang tidak sepenuhnya mencerminkan keadaan dagangan sebenar, dan keputusan sebenar mungkin berbeza daripadanya.

Pengoptimuman Strategi

-

Boleh mempertimbangkan untuk menambah garis hentian rugi bergerak dalam syarat penjualan, membolehkan strategi menghentikan kerugian tepat pada masanya dan mengawal risiko penurunan dengan berkesan.

-

Boleh mengembangkan mekanisme jual pendek, membuka kedudukan jual apabila TFO berbalik menurun dan ATR cukup besar, menjadikan strategi sesuai untuk pasaran menurun.

-

Boleh menambah lebih banyak syarat penapisan, seperti perubahan volum, untuk mengurangkan kesan pasaran yang tidak normal ke atas strategi.

-

Boleh menguji tetapan parameter dan hasil ujian belakang untuk jangka masa yang berbeza, mencari kombinasi jangka masa dan parameter terbaik.

Kesimpulan

Strategi ini menggabungkan kelebihan analisis arah aliran dan pemantauan turun naik, menilai arah pasaran melalui gabungan penunjuk TFO dan ATR; ia dilengkapi dengan mekanisme seperti penambahan kedudukan, penutupan separa, dan hentian rugi menjejak, yang boleh membesarkan keuntungan dan mengawal risiko, sesuai untuk pasaran menaik; ia juga mempunyai ruang pengoptimuman yang boleh diperluas, dengan menambah lebih banyak penapis penunjuk dan pelarasan parameter untuk meningkatkan prestasi strategi. Ia pada asasnya memenuhi keperluan fungsi asas strategi kuantitatif, dan patut dikaji serta diaplikasikan secara mendalam.

/*backtest

start: 2022-11-27 00:00:00

end: 2023-12-03 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Chart0bserver

//

// Open Source attributions:- 1