Strategi Kuantitatif Garis Gangguan Belitan Harian

Gambaran Keseluruhan

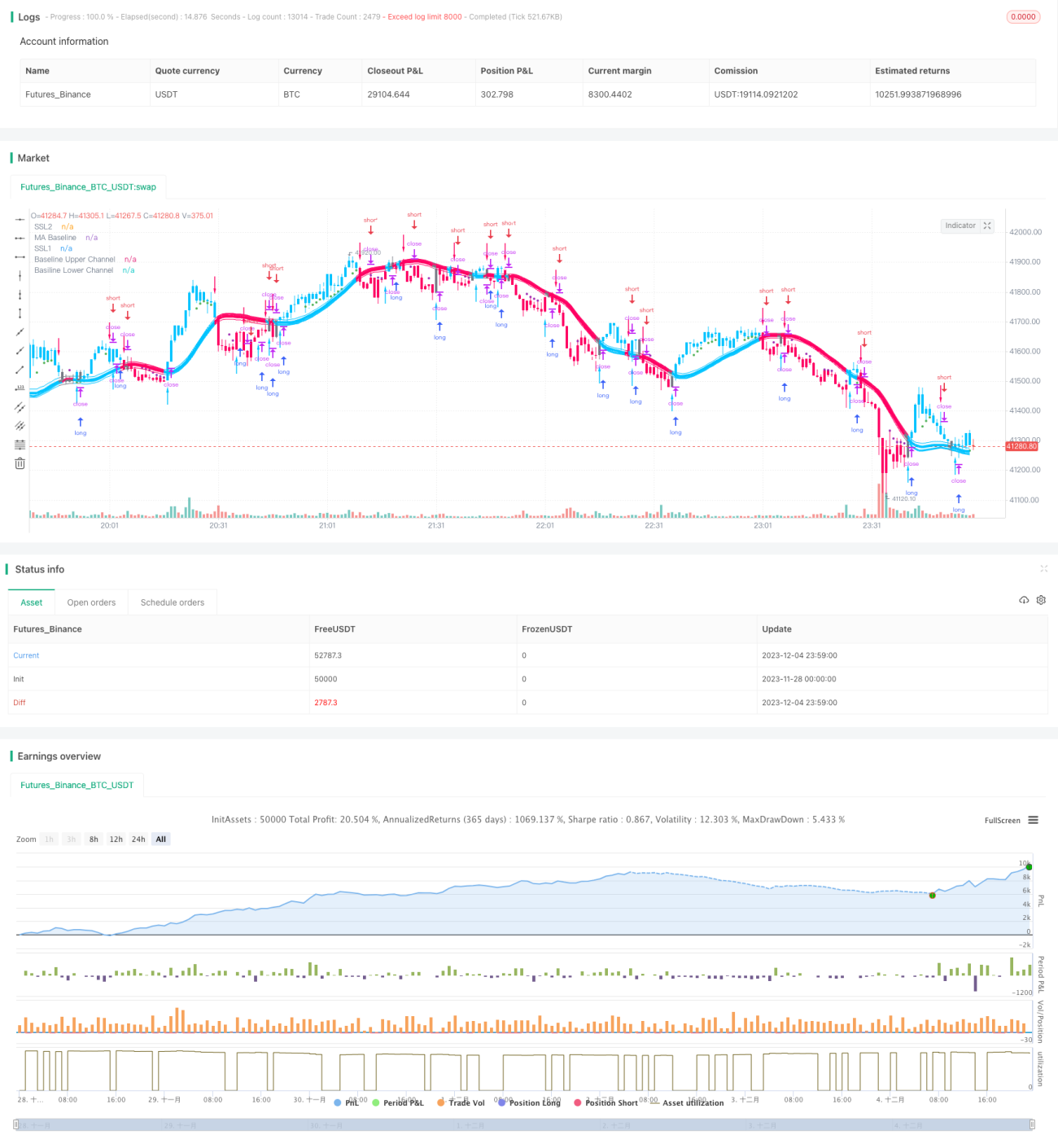

Strategi kuantitatif garisan pembahagian belitan harian ialah strategi dagangan kuantitatif jangka pendek berdasarkan purata bergerak dan penunjuk harga maksimum-minimum. Ia menggunakan anak panah EXIT daripada penunjuk hibrid SSL untuk menentukan titik beli dan jual, ditapis dengan penunjuk QQE, dan menggunakan penunjuk ATR untuk mengira tahap henti rugi dan kedudukan penambahan secara berperingkat. Strategi ini sesuai untuk pelabur yang sensitif terhadap turun naik pasaran dan mempunyai kawalan risiko yang ketat.

Prinsip Strategi

Strategi ini menggunakan anak panah EXIT daripada penunjuk hibrid SSL untuk menentukan titik masuk beli dan jual. Anak panah EXIT mempunyai titik tinggi EXIT di atas dan titik rendah EXIT di bawah. Apabila harga penutupan menembusi ke bawah dari titik tinggi EXIT, ia menghasilkan isyarat jual. Apabila harga penutupan menembusi ke atas dari titik rendah EXIT, ia menghasilkan isyarat beli.

Untuk meningkatkan kebolehpercayaan isyarat, strategi ini memperkenalkan penunjuk QQE sebagai penapis tambahan. Isyarat yang dihasilkan oleh anak panah EXIT hanya akan dilaksanakan apabila penunjuk QQE berada dalam arah yang sama.

Untuk mengawal risiko, strategi ini menggunakan penunjuk ATR berganda untuk mengira tahap henti rugi dan kedudukan penambahan secara berperingkat. Henti rugi pendek ialah harga penutupan + ATR × 1.8, henti rugi panjang ialah harga penutupan - ATR × 1.8. Penambahan dibuat dalam tiga kelompok, setiap kelompok ialah 10% daripada jumlah awal, dengan kedudukan tambahan masing-masing pada harga penutupan - ATR × 0.1, harga penutupan - ATR × 0.3, dan harga penutupan - ATR × 0.7.

Setiap kelompok tambahan mempunyai henti rugi yang berasingan. 20% daripada jumlah pertama akan dihenti rugi apabila mencapai tahap henti rugi, manakala baki kedudukan akan terus dipegang.

Kelebihan Strategi

- Mendapat keuntungan melalui anak panah EXIT, henti rugi tepat pada masanya, mengawal risiko dengan berkesan.

- Penapis penunjuk QQE meningkatkan ketepatan isyarat.

- Menggunakan penunjuk ATR untuk mengira henti rugi dan kedudukan tambahan berdasarkan turun naik pasaran, kawalan risiko lebih tepat.

- Penambahan secara berperingkat membolehkan memanfaatkan sepenuhnya arah aliran untuk keuntungan.

Risiko Strategi

- Kedudukan untung yang mencapai sebahagian henti rugi mungkin menyebabkan baki kedudukan berdepan risiko henti rugi seterusnya. Boleh pertimbangkan ambil untung keseluruhan atau ambil untung berdasarkan asas saham.

- Anak panah EXIT dan penunjuk QQE mempunyai sensitiviti yang berbeza terhadap turun naik pasaran, mungkin menghasilkan isyarat bercanggah. Parameter perlu dilaraskan untuk mengurangkan konflik isyarat.

- Penambahan yang terlalu agresif boleh menyebabkan membeli di puncak dan menjual di lantai. Perlu menilai keadaan, mengurangkan tahap leveraj.

Arah Pengoptimuman

- Menggabungkan penunjuk asas saham untuk ambil untung, contohnya menetapkan tahap ambil untung yang sesuai berdasarkan nisbah nilai buku, nisbah P/E dan dividen.

- Melaraskan parameter penunjuk QQE agar selaras dengan isyarat yang dihasilkan oleh anak panah EXIT.

- Mengurangkan nisbah penambahan berdasarkan sentimen pasaran, kurangkan penambahan dalam pasaran yang berayun.

- Menguji kombinasi parameter terbaik berdasarkan metrik seperti pengeluaran maksimum, nisbah untung/rugi.

Kesimpulan

Strategi ini menggunakan anak panah EXIT daripada penunjuk hibrid SSL sebagai isyarat teras, ditapis dengan penunjuk QQE dan ATR untuk henti rugi. Melalui penambahan secara berperingkat, keuntungan diperbesarkan. Ia adalah strategi kuantitatif jangka pendek yang sesuai untuk mengikuti arah aliran jangka pendek pasaran. Strategi ini mempunyai keupayaan kawalan pengeluaran dan risiko, tetapi perlu berhati-hati terhadap risiko isyarat bercanggah, membeli di puncak dan menjual di lantai. Jika boleh menggabungkan kaedah ambil untung berdasarkan asas saham, dan lebih berhati-hati dalam menilai pasaran berayun serta melaraskan nisbah penambahan, ruang keuntungan strategi ini akan menjadi lebih besar.

- 1