Strategi Kuantitatif Berdasarkan Kadar Perubahan Harga dan Purata Bergerak

Gambaran Keseluruhan

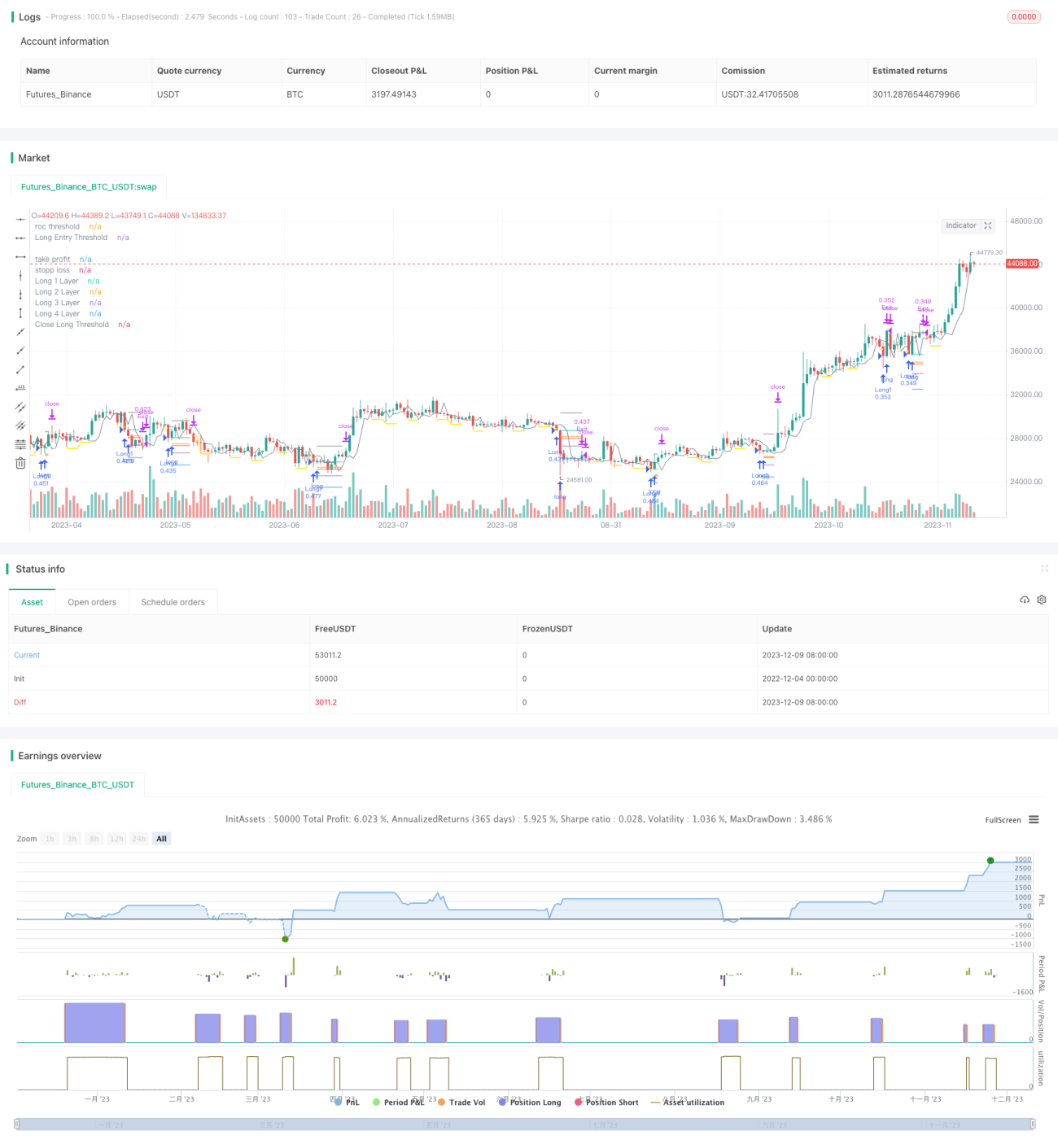

Strategi ini menggabungkan penunjuk teknikal kadar perubahan harga dan purata bergerak untuk mencapai penentuan tepat titik beli dan titik jual. Apabila harga menurun dengan ketara, ambang beli ditetapkan, dan apabila harga terus menurun, kedudukan beli (long) dibuka; apabila harga meningkat, ambang jual ditetapkan, dan apabila harga terus meningkat, kedudukan ditutup. Pada masa yang sama, strategi ini juga menggunakan kaedah penambahan kedudukan (pyramiding) dengan membeli secara berperingkat untuk mengurangkan kos.

Prinsip Strategi

Logik Beli

- Kira kadar perubahan harga (ROC) dan tetapkan garis ambang beli.

- Apabila harga menembusi di bawah garis ambang beli, catat titik tersebut dan aktifkan garis had beli.

- Garis had beli mempunyai tempoh masa yang ditetapkan berdasarkan parameter input, dan akan ditutup selepas tamat tempoh.

- Apabila harga terus menurun dan menembusi di bawah garis had beli, buka kedudukan beli (long) pertama.

Logik Jual

- Kira kadar perubahan harga (ROC) dan tetapkan garis ambang jual.

- Apabila harga menembusi di atas garis ambang jual, catat titik tersebut dan aktifkan garis had jual.

- Garis had jual mempunyai tempoh masa yang ditetapkan berdasarkan parameter input, dan akan ditutup selepas tamat tempoh.

- Apabila harga terus meningkat dan menembusi di atas garis had jual, tutup semua kedudukan beli (long).

Kawalan Risiko

Strategi ini dilengkapi dengan fungsi henti rugi (stop loss) dan ambil untung (take profit) yang boleh disesuaikan parameternya untuk mengawal risiko kedudukan secara masa nyata.

Kaedah Penambahan Kedudukan

Setiap kali kedudukan dagangan dibuka, harga beli seterusnya ditetapkan mengikut nisbah tertentu berdasarkan parameter input, membolehkan pembelian secara berperingkat dan menambah kedudukan.

Analisis Kelebihan

- Menggunakan penunjuk kadar perubahan harga (ROC) untuk mencari titik beli dan jual. ROC sangat sensitif terhadap perubahan harga, menjadikan penentuan titik beli dan jual tepat.

- Menggunakan kaedah garis had untuk mengesahkan masa dagangan dengan lebih lanjut, mengelakkan penembusan palsu.

- Kaedah penambahan kedudukan membolehkan pengesanan nilai pasaran sambil memastikan risiko terkawal.

- Fungsi henti rugi dan ambil untung terbina dalam mengawal risiko setiap kedudukan dengan ketat.

Risiko dan Penyelesaian

- Apabila pasaran turun naik secara mendadak, strategi mungkin membuka terlalu banyak kedudukan. Penyelesaiannya adalah dengan menetapkan parameter penambahan kedudukan secara munasabah dan mengawal jumlah kedudukan.

- Apabila arah aliran harga tidak jelas (sideways), harga henti rugi atau ambil untung mungkin sering dicetuskan. Ini boleh ditangani dengan melonggarkan julat henti rugi/ambil untung atau mematikan fungsi tersebut.

Cadangan Pengoptimuman

- Gabungkan dengan penunjuk lain untuk menapis masa masuk, contohnya dengan purata bergerak, hanya mempercayai isyarat ROC apabila harga jatuh di bawah purata bergerak.

- Optimumkan logik penambahan kedudukan, hanya memulakan penambahan apabila syarat tertentu dipenuhi, seperti hanya menambah kedudukan apabila harga turun semula melebihi had tertentu.

- Parameter untuk instrumen yang berbeza mungkin berbeza dengan ketara; ujian semula (backtesting) dan dagangan simulasi yang mencukupi diperlukan untuk mendapatkan kombinasi parameter terbaik.

- Boleh menetapkan henti rugi/ambil untung adaptif berdasarkan tahap turun naik pasaran.

Kesimpulan

Strategi ini menggabungkan penunjuk ROC untuk menentukan titik beli dan jual dengan tepat, kaedah garis had untuk menapis isyarat, fungsi henti rugi/ambil untung terbina dalam untuk mengawal risiko, dan penambahan kedudukan untuk meluaskan keuntungan. Dengan parameter yang ditetapkan secara munasabah, strategi ini boleh memperoleh pulangan lebih tinggi sambil memastikan risiko terkawal. Pada masa hadapan, mekanisme penapisan isyarat dan kawalan risiko boleh dioptimumkan lagi supaya strategi ini dapat menyesuaikan diri dengan lebih banyak persekitaran pasaran.

- 1