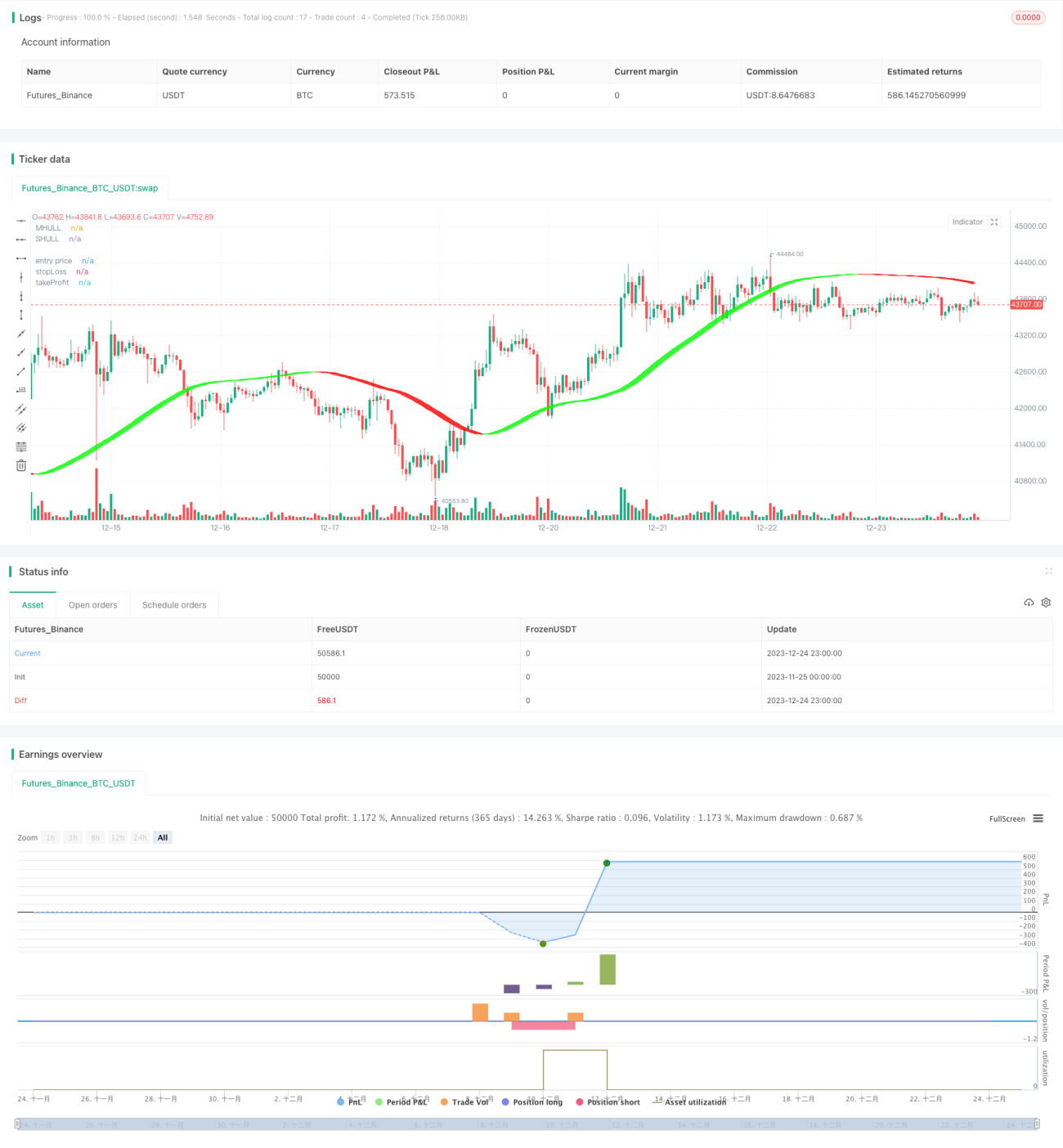

Strategi perdagangan Bitcoin berdasarkan penunjuk kuantitatif

Gambaran Keseluruhan

Strategi ini menggunakan pelbagai penunjuk kuantitatif untuk menentukan masa beli dan jual Bitcoin, dan melaksanakan perdagangan automatik. Ia merangkumi Indeks Hull (Hull), Indeks Kekuatan Relatif (RSI), Bollinger Band (BB), dan Pengayun Volume (VO).

Prinsip Strategi

-

Menggunakan Purata Pergerakan Hull yang diubah suai untuk menentukan arah aliran utama pasaran, digabungkan dengan Bollinger Band untuk membantu mengenal pasti titik beli dan jual yang menembusi.

-

Penunjuk RSI digabungkan dengan julat turun naik adaptif untuk mengenal pasti kawasan terlebih beli dan terlebih jual, menghasilkan isyarat dagangan. Pada masa yang sama, dua set parameter ditetapkan sebagai pengesahan isyarat Duplikat.

-

Pengayun Volume menilai momentum beli dan jual untuk mengelakkan penembusan palsu.

-

Mempreskripsi tahap henti rugi dan ambil untung berdasarkan nisbah harga henti rugi/ambil untung untuk menguruskan risiko.

Analisis Kelebihan

-

Lengkung Hull dapat menangkap perubahan arah aliran dengan lebih cepat, manakala bantuan Bollinger Band dapat mengurangkan isyarat palsu.

-

Pengoptimuman parameter RSI dan pengesahan isyarat Duplikat meningkatkan kebolehpercayaan.

-

Pengayun Volume digabungkan dengan isyarat aliran dan penunjuk mengelakkan perdagangan yang tidak tepat.

-

Kaedah henti rugi dan ambil untung yang dipreskripsi dapat mengawal untung/rugi setiap transaksi secara automatik, mengawal risiko keseluruhan dengan berkesan.

Analisis Risiko

-

Penetapan parameter yang tidak sesuai boleh menyebabkan frekuensi perdagangan terlalu tinggi atau kesan isyarat menjadi lemah.

-

Apabila pasaran berubah secara mendadak akibat peristiwa luar jangka, henti rugi mungkin tertembus, menyebabkan kerugian besar.

-

Apabila menukar instrumen dagangan kepada mata wang kripto lain, parameter perlu diuji dan dioptimumkan semula.

-

Apabila data volume hilang, Pengayun Volume akan menjadi tidak berkesan.

Hala Tuju Pengoptimuman

-

Melakukan lebih banyak ujian gabungan parameter RSI untuk mencari parameter terbaik.

-

Mencuba penunjuk lain seperti MACD, KD dan lain-lain digabungkan dengan RSI untuk meningkatkan ketepatan isyarat.

-

Menambah modul ramalan model, menggabungkan pembelajaran mesin untuk menentukan arah pasaran.

-

Menguji kesan parameter apabila menukar kepada instrumen dagangan lain.

-

Mengoptimumkan algoritma henti rugi dan ambil untung untuk memaksimumkan keuntungan.

Ringkasan

Strategi ini menggabungkan pelbagai penunjuk teknikal kuantitatif untuk menentukan masa beli dan jual. Dengan kaedah seperti pengoptimuman parameter dan kawalan risiko, perdagangan automatik Bitcoin telah dicapai. Prestasi agak baik, tetapi masih memerlukan ujian dan pengoptimuman berterusan untuk menyesuaikan diri dengan perubahan pasaran. Ia boleh dijadikan rujukan bagi pelabur untuk membantu keputusan perdagangan.

- 1