Strategi Pelaburan Berkala Kos Purata Dinamik dengan Faedah Kompaun

Gambaran Keseluruhan

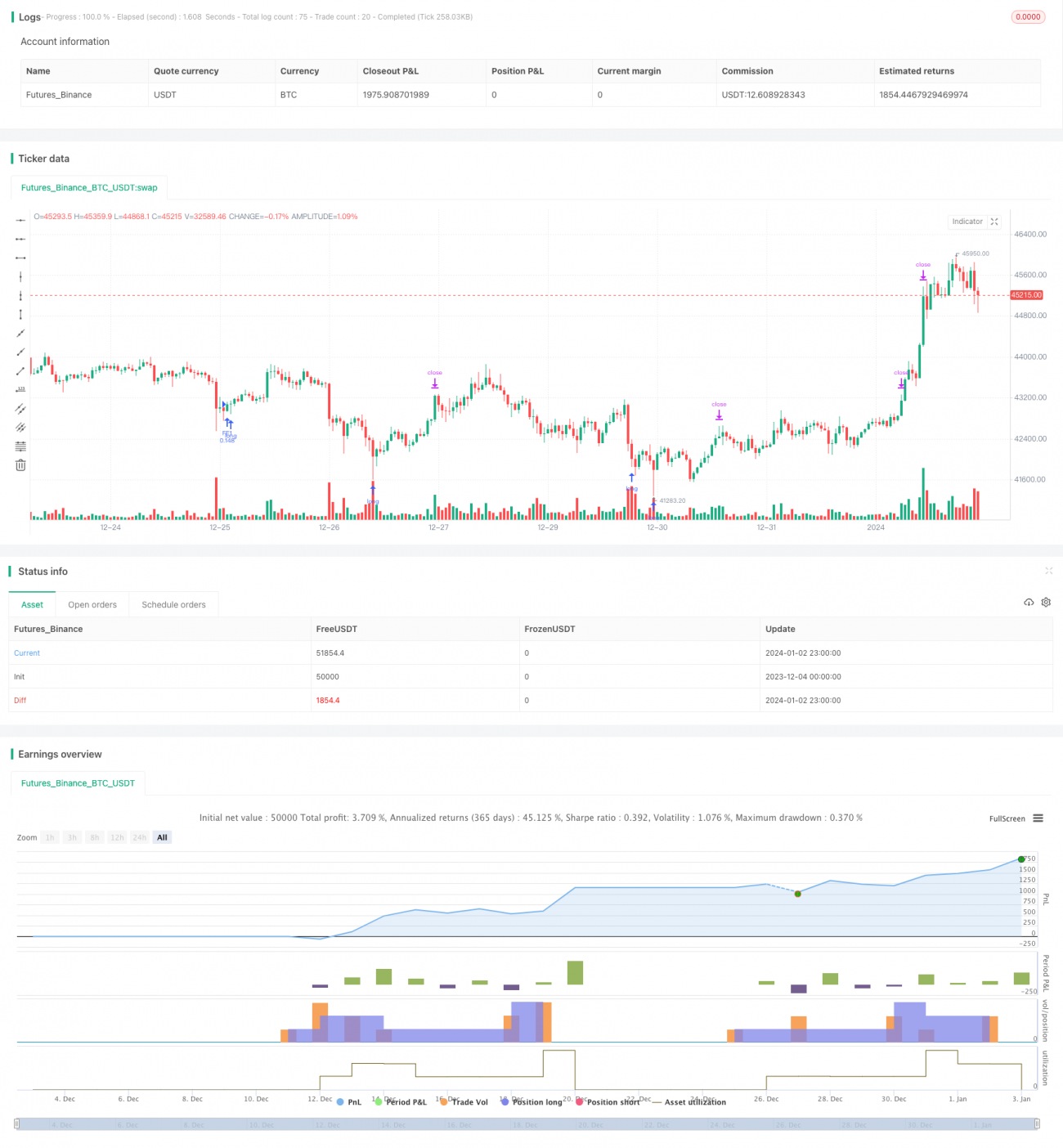

Strategi pelaburan berkala kos purata dinamik dan faedah kompaun ini melaraskan kuantiti bukaan setiap kali secara dinamik. Pada fasa awal arah aliran, buka sedikit posisi terlebih dahulu, dan secara beransur-ansur meningkatkan saiz posisi apabila kedalaman pengukuhan meningkat. Strategi ini menggunakan fungsi eksponen untuk mengira tahap henti rugi setiap lapisan, dan mencetuskan pembukaan semula posisi secara berperingkat, membolehkan garis kos pegangan menurun secara eksponen. Dengan peningkatan kedalaman, kos pegangan boleh dimampatkan ke bawah secara berperingkat, dan selepas harga berbalik, keuntungan diambil secara berperingkat untuk memperoleh pulangan yang lebih besar.

Prinsip Strategi

Strategi ini menggunakan isyarat RSI tak terlebih jual yang ringkas dan gabungan kaedah pemasaan purata bergerak untuk memilih masa buka posisi. Apabila RSI jatuh di bawah garis tak terlebih jual dan harga penutupan kurang daripada purata bergerak, isyarat bukaan pertama dicetuskan. Selepas bukaan pertama, berdasarkan fungsi eksponen, had bawah penurunan harga dikira untuk menghasilkan isyarat DCA. Setiap kali DCA, kedudukan pegangan diselaraskan supaya setiap lot adalah sama. Oleh kerana perubahan dinamik dalam kuantiti dan kos pegangan, kesan leveraj berlaku.

Dengan peningkatan bilangan DCA, kos pegangan terus menurun, dan setiap pengambilan untung hanya memerlukan lantunan yang sangat kecil untuk mencapai keuntungan. Selepas beberapa pesanan berturut-turut dibuka, garis henti rugi akan dilukis di atas harga purata. Setelah harga menembusi semula ke atas, melebihi harga purata pegangan dan garis henti rugi, posisi akan ditutup untuk henti rugi.

Kelebihan utama strategi ini ialah apabila kos pegangan terus menurun, walaupun dalam pasaran pengukuhan, kos dapat dikurangkan secara beransur-ansur. Apabila arah aliran berbalik, kerana kos pegangan sudah jauh lebih rendah daripada harga pasaran, keuntungan yang lebih besar dapat dicapai.

Risiko dan Kelemahan

Risiko terbesar strategi ini ialah kedudukan awal yang terhad. Sekiranya berlaku penurunan berterusan, terdapat risiko henti rugi. Oleh itu, perlu menetapkan tahap henti rugi yang boleh diterima.

Selain itu, penetapan tahap henti rugi juga mempunyai dua ekstrem. Jika tetapan terlalu besar, lantunan yang cukup dalam tidak dapat ditangkap. Manakala jika tetapan terlalu kecil, dalam pelarasan pertengahan, kemungkinan harga berbalik naik semula adalah lebih tinggi. Oleh itu, memilih tahap henti rugi yang sesuai berdasarkan pasaran yang berbeza dan toleransi risiko sendiri adalah sangat penting.

Apabila kitaran DCA panjang dan membentuk banyak lapisan, jika harga melonjak naik, risiko kos pegangan terlalu tinggi dan tidak boleh dihentikan rugi akan timbul. Oleh itu, perlu menetapkan lapisan DCA secara munasabah berdasarkan jumlah pegangan sendiri dan kos pegangan maksimum yang boleh diterima.

Cadangan Pengoptimuman

-

Optimumkan isyarat pemasaan. Uji parameter yang berbeza dan kombinasi penunjuk yang berbeza untuk memilih isyarat dengan kadar kemenangan yang lebih tinggi.

-

Optimumkan mekanisme henti rugi. Uji penggunaan henti rugi berbentuk Λ atau henti rugi lengkung bulat sebagai ganti henti rugi bergerak mudah, yang mungkin memberikan kesan henti rugi yang lebih baik. Juga boleh menambah strategi pelarasan saiz posisi mengikut masa untuk melaraskan tahap henti rugi.

-

Optimumkan cara pengambilan untung. Uji pelbagai jenis ambil untung bergerak untuk mencari peluang ambil untung yang lebih baik, dengan itu meningkatkan kadar pulangan keseluruhan.

-

Tambah mekanisme anti-lantunan. Selepas henti rugi, mungkin berlaku isyarat DCA semula yang menyebabkan posisi dibuka semula. Dalam kes ini, pertimbangkan untuk menambah julat anti-lantunan tertentu untuk mengelakkan pembukaan posisi secara agresif semula dengan segera selepas henti rugi.

Kesimpulan

Strategi ini menggunakan penunjuk RSI untuk menentukan masa beli, serta strategi DCA henti rugi dinamik yang dikira berdasarkan fungsi eksponen, untuk melaraskan kuantiti dan kos pegangan secara dinamik, dengan itu memperoleh kelebihan harga dalam pasaran julat. Pengoptimuman tertumpu pada isyarat masuk/keluar, kaedah henti rugi dan ambil untung, dan lain-lain. Secara keseluruhan, strategi ini menggunakan konsep teras DCA eksponen, menjadikan kos pegangan terus bergerak ke bawah, memberikan lebih banyak ruang operasi semasa pengukuhan dan pulangan yang lebih tinggi dalam pasaran arah aliran. Walau bagaimanapun, masih perlu memilih parameter yang sesuai berdasarkan pelan pengurusan modal sendiri untuk mengawal risiko posisi keseluruhan.

- 1