Strategi Keuntungan Jangka Pendek Berdasarkan Corak V RSI

Gambaran Keseluruhan

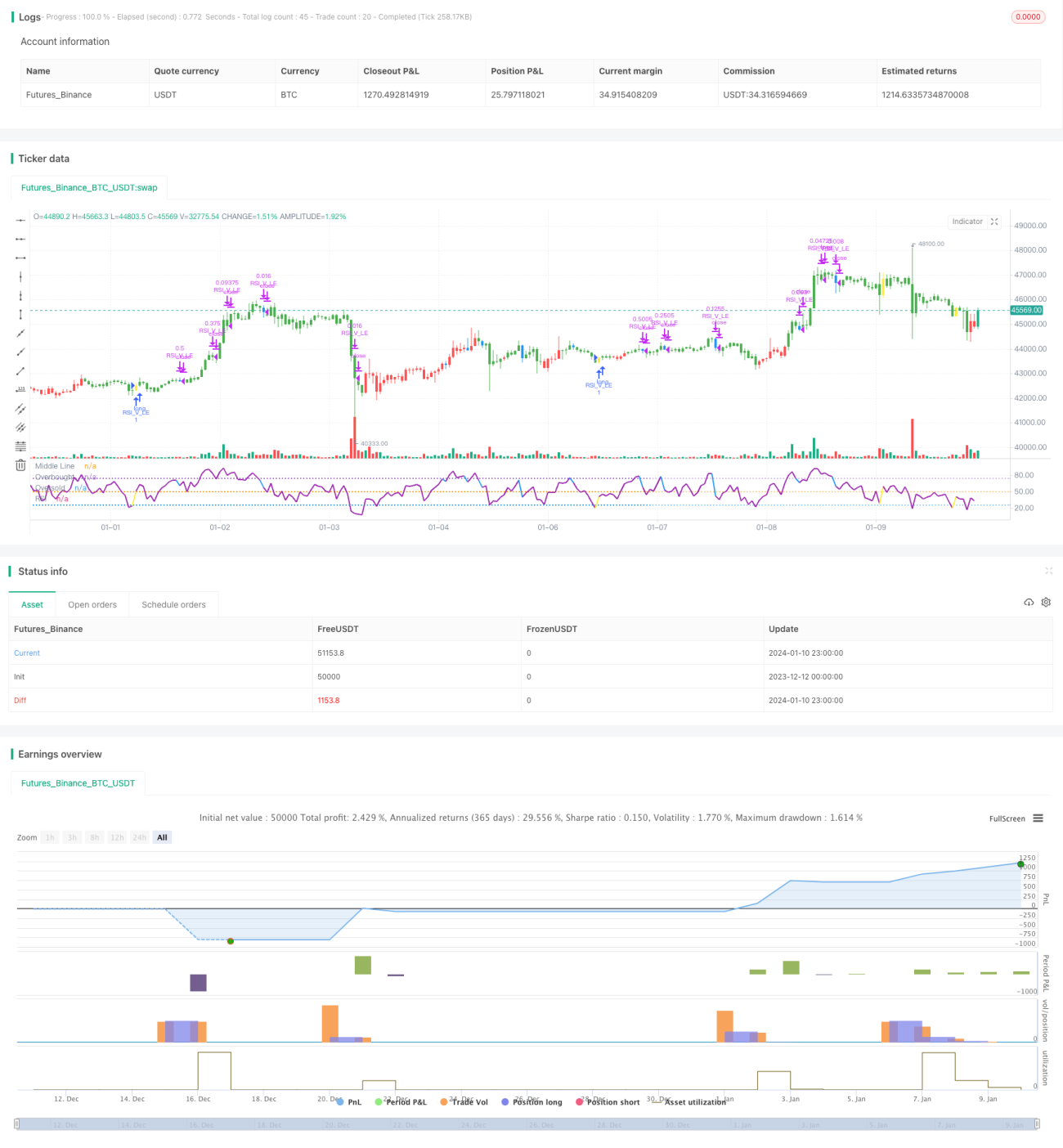

Strategi ini berdasarkan bentuk V pada indikator RSI, digabungkan dengan penapis EMA, untuk membentuk strategi jangka pendek yang agak boleh dipercayai. Ia dapat menangkap peluang lantunan semula harga di zon terlebih jual, dengan isyarat bentuk V pada RSI untuk membuka posisi beli dengan tepat, seterusnya meraih keuntungan dalam jangka pendek.

Prinsip Strategi

- Menggunakan garis 20 hari di atas garis 50 hari sebagai penentu arah menaik jangka panjang.

- RSI membentuk bentuk V, menandakan peluang lantunan semula dari zon terlebih jual.

- Titik terendah bar sebelumnya lebih rendah daripada titik terendah dua bar sebelumnya.

- RSI bar semasa lebih tinggi daripada RSI dua bar sebelumnya.

- RSI menembusi 30 sebagai isyarat bentuk V selesai, buka posisi beli.

- Henti rugi ditetapkan pada 8% di bawah harga masuk.

- RSI menembusi 70, mula menutup sebahagian kedudukan (tzinfo), henti rugi dialihkan ke harga masuk.

- RSI menembusi 90, mula menutup 3/4 kedudukan (tzinfo).

- RSI menembusi 10 / henti rugi tersentuh, tutup semua kedudukan.

Analisis Kelebihan

- Menggunakan EMA untuk menentukan arah trend utama, mengelakkan perdagangan melawan trend.

- Bentuk V RSI mengesan peluang lantunan semula di zon terlebih jual, menangkap pembalikan trend.

- Pelbagai mekanisme henti rugi mengawal risiko.

Analisis Risiko

- Kejatuhan pasaran yang besar mungkin tidak dapat dihentikan rugi, menyebabkan kerugian besar.

- Isyarat bentuk V RSI mungkin tersilap, menyebabkan kerugian yang tidak perlu.

Arah Pengoptimuman

- Mengoptimumkan parameter RSI untuk mencari bentuk V RSI yang lebih boleh dipercayai.

- Menggabungkan indikator lain untuk menilai kebolehpercayaan isyarat pembalikan.

- Mengoptimumkan strategi henti rugi, mengekalkan keseimbangan antara mengelakkan agresif dan henti rugi tepat pada masanya.

Kesimpulan

Strategi ini mengintegrasikan penapis EMA dan penilaian bentuk V RSI, membentuk satu set strategi operasi jangka pendek yang agak boleh dipercayai. Ia dapat memanfaatkan peluang lantunan semula di zon terlebih jual, mencapai keuntungan dalam jangka pendek. Dengan pengoptimuman parameter dan model yang berterusan, serta penambahbaikan mekanisme henti rugi, strategi ini dapat meningkatkan kestabilan dan keuntungan. Ia membuka satu lagi pintu keuntungan jangka pendek untuk pedagang kuantitatif.

- 1