Strategi Kuantitatif Gabungan Tiga Purata Pergerakan dan MACD

Gambaran Keseluruhan

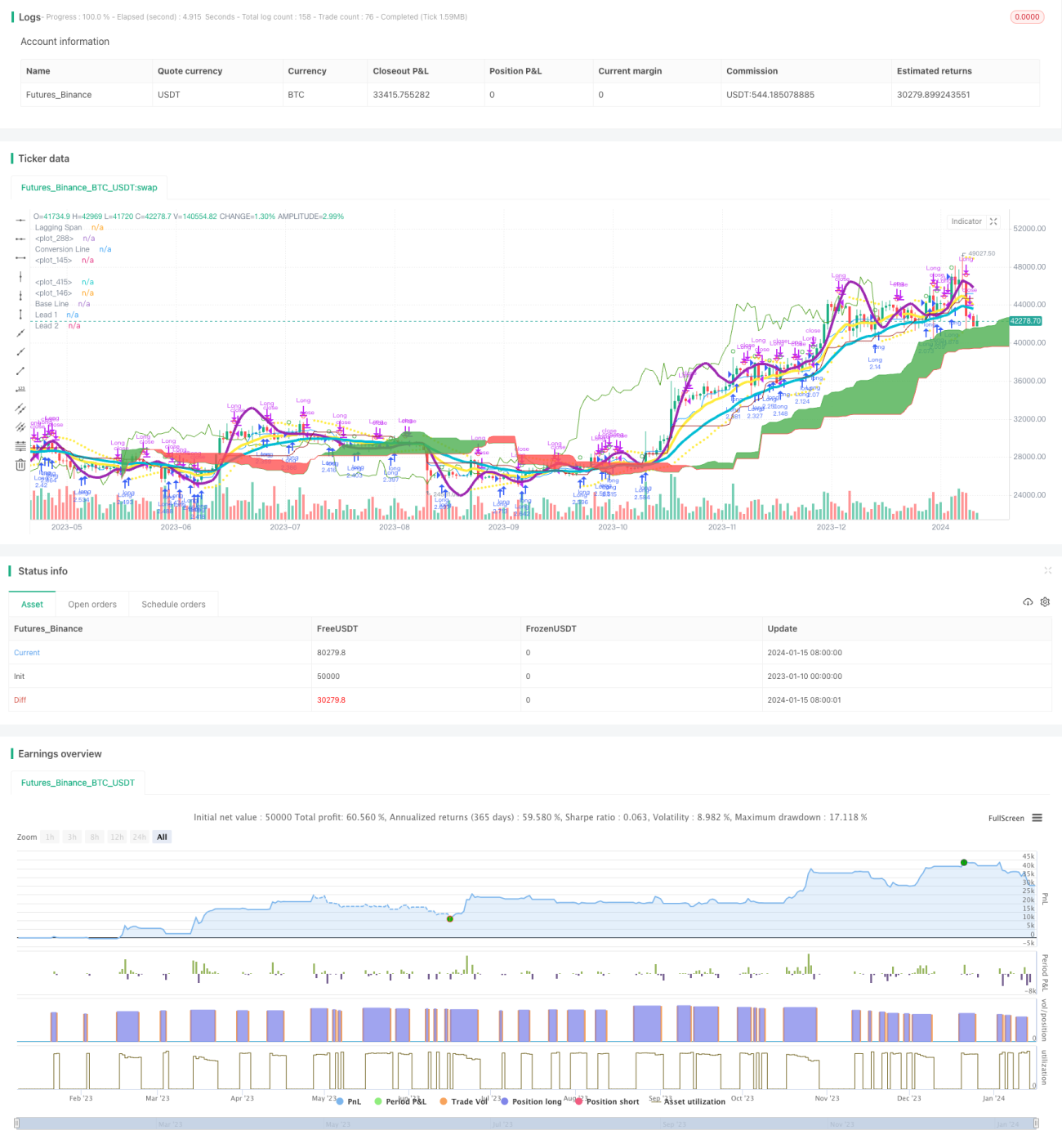

Strategi ini membangunkan strategi perdagangan kuantitatif yang agak stabil dan boleh dipercayai dengan menggabungkan penggunaan penunjuk Purata Bergerak Tiga Kali ganda dan penunjuk MACD. Strategi ini bertujuan untuk menangkap arah aliran yang mungkin muncul pada masa hadapan, dan sangat sesuai untuk pegangan jangka sederhana hingga panjang.

Prinsip Strategi

Strategi ini terutamanya berdasarkan gabungan penggunaan Purata Bergerak Tiga Kali ganda dan penunjuk MACD.

Pertama, strategi ini menggunakan purata bergerak eksponen tiga kali ganda dengan panjang masing-masing 3, 7, dan 2. Ketiga-tiga purata bergerak ini membina sistem purata bergerak dari pantas ke perlahan, digunakan untuk menentukan arah aliran masa hadapan. Apabila purata bergerak jangka pendek melintasi ke atas purata bergerak jangka panjang, ia adalah isyarat untuk posisi panjang; apabila purata bergerak jangka pendek melintasi ke bawah purata bergerak jangka panjang, ia adalah isyarat untuk posisi pendek.

Kedua, strategi ini juga menggunakan penunjuk MACD dengan parameter 3 dan 7 secara serentak. Apabila garis utama MACD melintasi ke atas garis isyarat, ia adalah isyarat untuk posisi panjang, dan apabila melintasi ke bawah, ia adalah isyarat untuk posisi pendek.

Dengan menggabungkan penggunaan dua penunjuk, ia dapat mengelakkan pelbagai isyarat palsu yang disebabkan oleh satu penunjuk, sekali gus meningkatkan kestabilan strategi.

Kelebihan Strategi

- Menggunakan penapisan dua penunjuk untuk meningkatkan kualiti isyarat

- Parameter telah diuji dan dioptimumkan berkali-kali, stabil dan boleh dipercayai

- Menggunakan sistem purata bergerak tiga kali ganda, mampu menapis gangguan pasaran dengan berkesan dan menentukan arah aliran masa hadapan

- Tetapan parameter penunjuk MACD yang lebih pantas membolehkan penangkapan peluang jangka pendek dengan cepat

Risiko Strategi

- Terdapat risiko pengeluaran dan kerugian berturut-turut

- Apabila pasaran tidak mempunyai arah aliran yang jelas, strategi ini akan menghasilkan lebih banyak perdagangan yang salah

- Penunjuk MACD mudah menghasilkan isyarat palsu, perlu digunakan bersama dengan penunjuk purata bergerak

Kaedah Penyelesaian:

- Menggunakan strategi henti rugi yang sesuai untuk mengawal pengeluaran maksimum

- Apabila Keadaan Pasaran jelas tidak mempunyai arah aliran, kurangkan kekerapan perdagangan

- Optimumkan parameter MACD dan gunakan bersama dengan penunjuk lain

Arah Pengoptimuman Strategi

- Menguji dan mengoptimumkan parameter purata bergerak dan MACD untuk mencari kombinasi terbaik

- Menambah penunjuk tambahan seperti KDJ, RSI untuk mengelakkan isyarat palsu

- Menambah model pembelajaran mesin untuk menilai Keadaan Pasaran, membolehkan pelarasan dinamik

- Menggabungkan strategi henti rugi untuk menetapkan titik henti rugi yang optimum

Kesimpulan

Strategi ini mencapai penangkapan arah aliran yang stabil melalui gabungan purata bergerak dan MACD. Kelebihan strateginya terletak pada penggunaan gabungan penunjuk, yang dapat mengurangkan isyarat palsu dengan berkesan, sekali gus memperoleh kesan strategi yang lebih baik. Seterusnya, melalui pengoptimuman parameter, pengenalan strategi henti rugi, pelarasan dinamik dan cara lain untuk menambah baik strategi ini, menjadikannya alat yang berkesan untuk mencari peluang jangka sederhana hingga panjang.

/*backtest

start: 2023-01-10 00:00:00

end: 2024-01-16 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

strategy("Matt's MACD Algo v1", shorttitle="Matt's MACD Algo v1", overlay=true, pyramiding = 0, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, initial_capital=7000, calc_on_order_fills = true, commission_type=strategy.commission.percent, commission_value=0, currency = currency.USD)

//study("MFI Fresh", shorttitle="MFI Fresh", overlay=true)

- 1