RSI penjejakan arah aliran strategi henti rugi

Gambaran Keseluruhan

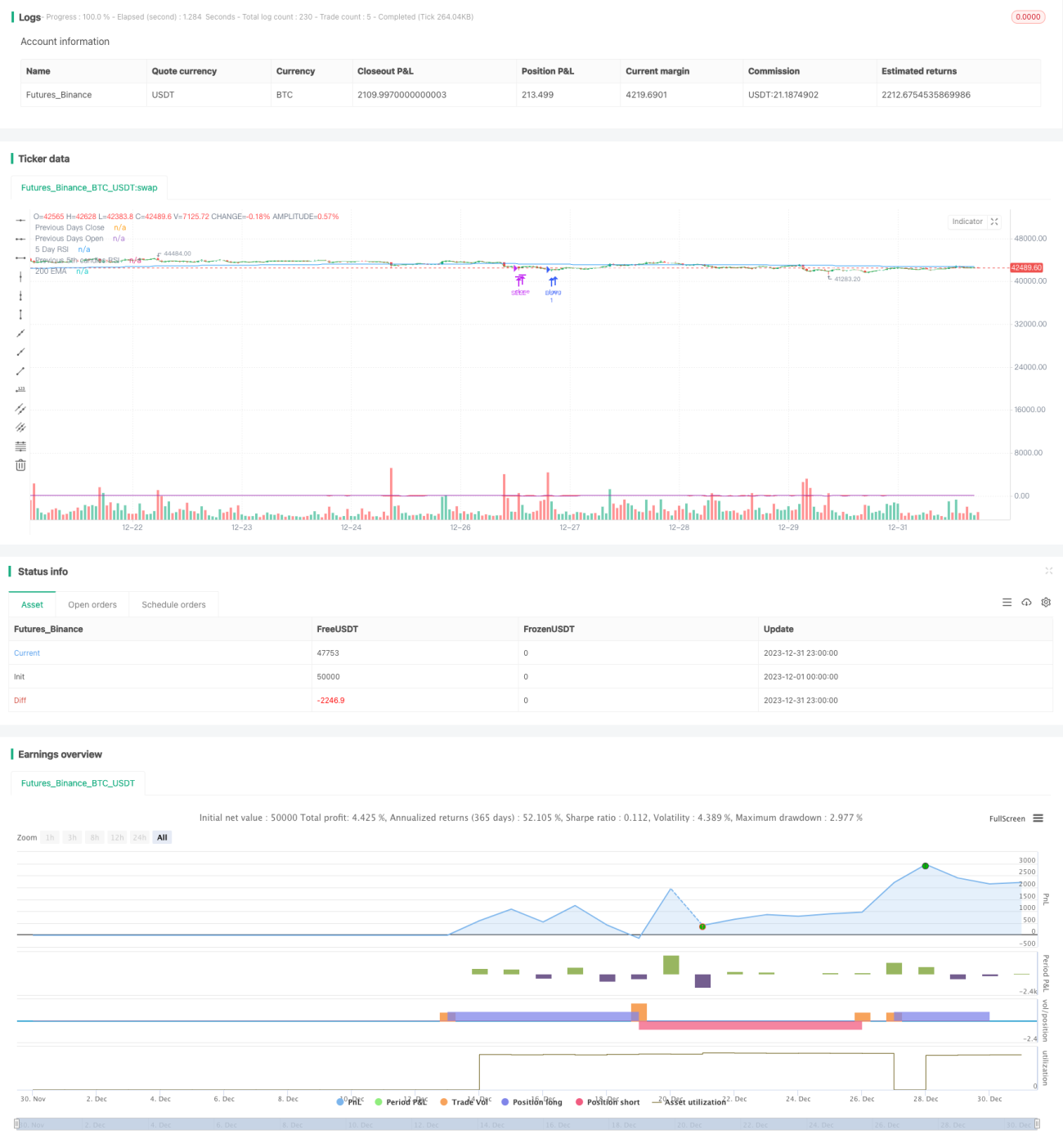

Ini adalah strategi perdagangan kuantitatif yang menggunakan indikator RSI untuk menentukan arah tren dan menetapkan henti rugi serta ambil untung. Strategi ini menggabungkan indikator RSI untuk menilai arah tren pasaran, serta menetapkan henti rugi dan ambil untung dinamik untuk mengunci keuntungan dan meminimumkan risiko.

Prinsip Strategi

Strategi ini terutamanya menggunakan indikator RSI untuk menentukan arah tren pasaran bagi memutuskan sama ada untuk membeli atau menjual. Apabila indikator RSI menembusi garisan rendah ke atas, ia dianggap sebagai pasaran berada dalam arah menaik, maka beli (long). Apabila indikator RSI menembusi garisan tinggi ke bawah, ia dianggap sebagai pasaran berada dalam arah menurun, maka jual (short).

Pada masa yang sama, strategi ini menjejaki harga buka setiap pesanan dan menetapkan henti rugi dan ambil untung terapung. Untuk pesanan beli, satu peratusan tertentu daripada harga buka ditetapkan sebagai garisan henti rugi, manakala untuk pesanan jual, satu peratusan tertentu daripada harga buka ditetapkan sebagai garisan ambil untung. Apabila harga menyentuh garisan henti rugi atau ambil untung, strategi akan menutup kedudukan secara automatik untuk henti rugi atau ambil untung.

Kelebihan Strategi

- Menggunakan indikator RSI untuk menentukan arah tren pasaran, mengelakkan perdagangan dalam julat penyatuan;

- Menetapkan henti rugi dan ambil untung terapung, dapat mengunci keuntungan secara fleksibel dan mengawal risiko dengan berkesan;

- Parameter RSI dan nisbah henti rugi/ambil untung boleh dilaraskan dan dioptimumkan melalui input luaran.

Risiko Strategi

- Indikator RSI mempunyai sedikit kelewatan, mungkin terlepas titik perubahan tren jangka pendek;

- Garisan henti rugi dan ambil untung yang terlalu rapat mungkin menyebabkan kedudukan tertutup akibat penembusan.

Arah Pengoptimuman

- Boleh menguji kesan indikator RSI pada jangka masa yang berbeza;

- Boleh menguji pelbagai kombinasi parameter untuk mencari nisbah henti rugi/ambil untung yang optimum;

- Boleh menambah indikator tambahan untuk menapis isyarat.

Kesimpulan

Secara keseluruhan, strategi ini adalah strategi perdagangan kuantitatif yang menggunakan indikator RSI untuk menjejaki arah tren, serta dilengkapi dengan henti rugi dan ambil untung terapung. Berbanding dengan strategi yang hanya menggunakan satu indikator, strategi ini lebih baik dalam mengawal risiko dan dapat mengunci keuntungan dengan berkesan. Prestasi strategi boleh ditingkatkan lagi melalui pengoptimuman parameter dan penambahan indikator tambahan.

- 1