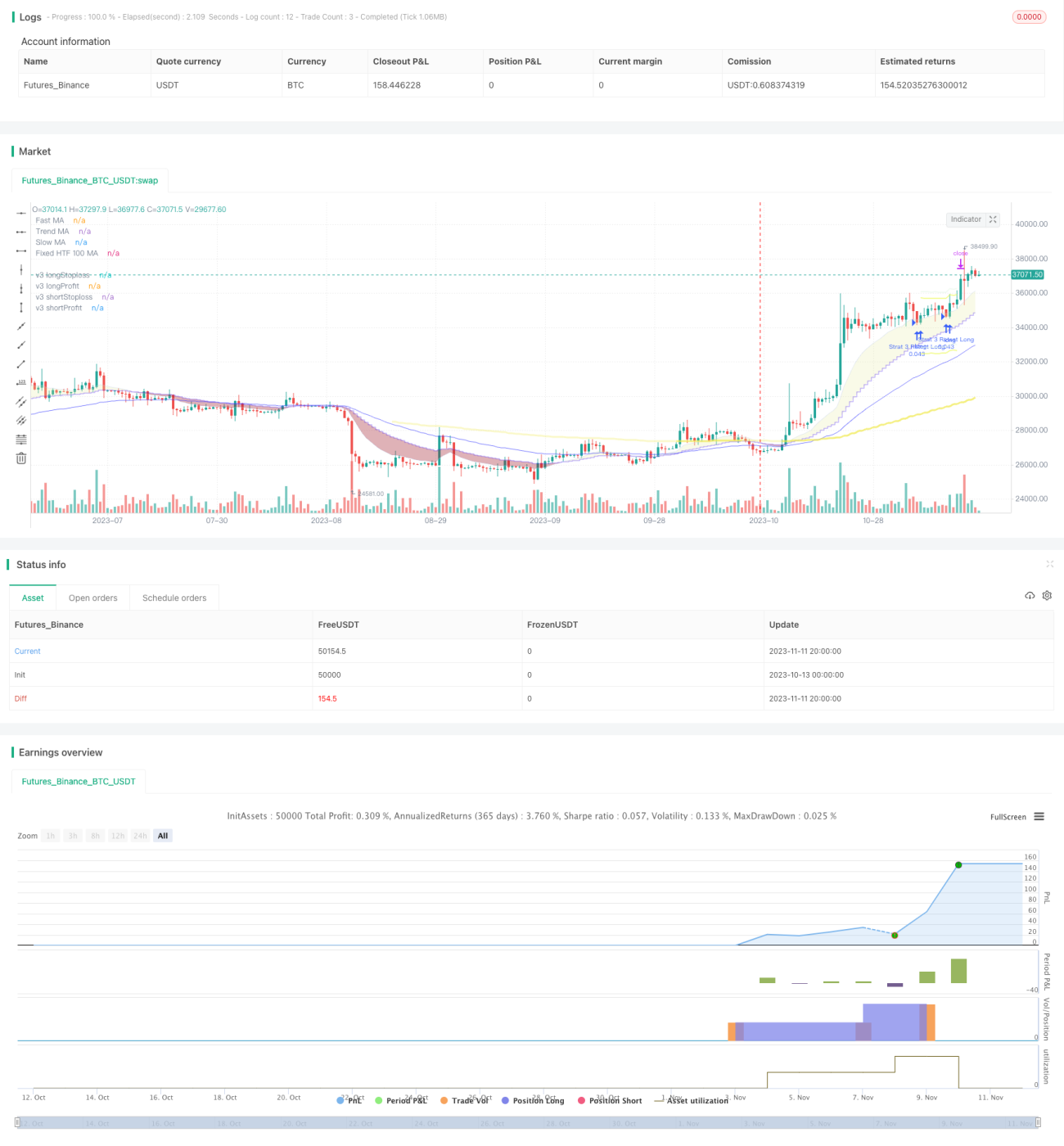

Estratégia de Negociação do Sistema de Cruzamento de Médias Móveis

Visão Geral

Esta estratégia é baseada em um sistema de cruzamento de médias móveis. Ela calcula médias móveis de diferentes períodos e utiliza os cruzamentos entre elas como sinais de compra e venda. Também combina o indicador RSI para filtrar os sinais, reduzindo a frequência de negociações e aumentando a taxa de lucro.

Princípio da Estratégia

-

Calcular a média móvel rápida, a média móvel média e a média móvel lenta. As médias rápida e média formam um canal de negociação.

-

Quando o preço cruza acima da média rápida, comprar; quando o preço cruza abaixo da média rápida, vender.

-

Direção do canal de negociação: média rápida > média média → tendência de alta; média rápida < média média → tendência de baixa. Negociar apenas quando a direção do canal for consistente.

-

A média lenta atua como filtro de tendência: comprar apenas quando o preço estiver acima da média lenta; vender apenas quando estiver abaixo.

-

Indicador RSI: comprar quando o RSI estiver acima da linha de compra definida; vender quando o RSI estiver abaixo da linha de venda definida.

-

Stop loss e take profit: utilizar stop loss baseado no ATR e take profit baseado no ATR.

Análise de Vantagens

-

Múltiplas combinações de médias móveis, adaptando-se flexivelmente às mudanças do mercado.

-

O indicador RSI evita falsos rompimentos, melhorando a qualidade dos sinais.

-

Stop loss e take profit dinâmicos com ATR reduzem o risco de liquidação forçada.

-

Dupla filtragem (média lenta + RSI) evita negociações desnecessárias.

Análise de Riscos

-

Os sinais de cruzamento de médias móveis podem apresentar atraso.

-

A dupla filtragem pode perder algumas oportunidades de negociação.

-

O stop loss baseado em ATR pode exceder a faixa normal de stop loss.

-

Parâmetros mal ajustados podem resultar em negociações muito frequentes ou muito esparsas.

Medidas correspondentes de gerenciamento de risco:

-

Reduzir adequadamente o período das médias móveis para diminuir a probabilidade de atraso.

-

Ajustar adequadamente os parâmetros de filtragem para manter uma frequência moderada de negociações.

-

Ajustar o múltiplo do ATR para garantir que o stop loss esteja dentro de uma faixa aceitável.

-

Otimizar a configuração dos parâmetros para encontrar a melhor combinação.

Direções de Otimização

-

Testar o efeito de diferentes tipos de médias móveis combinadas.

-

Testar a otimização dos períodos das médias móveis.

-

Testar a otimização dos parâmetros do RSI.

-

Otimizar os coeficientes de stop loss e take profit baseados em ATR.

-

Otimizar os parâmetros de filtragem para encontrar a intensidade ideal de filtragem.

Resumo

Esta estratégia utiliza de forma integrada os indicadores de médias móveis, RSI e ATR. Através da otimização de parâmetros, é possível configurar um sistema de negociação adaptável a diferentes mercados. Em comparação com indicadores técnicos únicos, ela pode reduzir efetivamente sinais falsos e aumentar a probabilidade de lucro. No entanto, nenhuma estratégia baseada em indicadores técnicos pode eliminar completamente os riscos de mercado, sendo necessário estabelecer um sistema rigoroso de gerenciamento de riscos como garantia.

- 1