Estratégia de stop loss móvel por reversão de tendência

Visão Geral

Esta estratégia baseia-se em indicadores de reversão de tendência, combinados com um mecanismo de stop loss de acompanhamento de tendência, conseguindo rastrear a tendência em mercados direcionais e reduzir perdas em mercados laterais.

Princípio da Estratégia

A estratégia utiliza a Média Móvel Hull como principal indicador de tendência. Quando o preço cruza para cima da média Hull, abre-se uma posição comprada; quando cruza para baixo, abre-se uma posição vendida. Ao mesmo tempo, a Média Móvel McGinley é usada para confirmar a tendência.

Após a abertura da posição, se o preço reverter, ou seja, quando a média Hull gerar um cruzamento, a lógica de mudança de tendência é executada, fechando a posição atual.

A estratégia também incorpora um mecanismo de stop loss dinâmico. Após abrir uma posição, o nível de stop loss é calculado com base no ATR. Conforme o preço se move, a linha de stop loss é ajustada dinamicamente, permitindo um trailing stop sobre os lucros.

Vantagens da Estratégia

- Uso da média Hull para identificar pontos de reversão de tendência, sendo sensível a sinais de rompimento.

- Combinação com a média McGinley para confirmar a tendência, filtrando alguns rompimentos falsos.

- Mecanismo de stop loss dinâmico que ajusta a amplitude conforme a volatilidade do mercado, controlando perdas de forma eficaz.

- Resposta rápida a reversões de tendência ao monitorar cruzamentos da média Hull, evitando o agravamento das perdas.

- Facilidade para testar diferentes combinações de parâmetros em busca dos valores ideais.

Riscos e Soluções

-

Em mercados oscilantes, o stop loss pode ser acionado indevidamente.

- Pode-se aumentar a amplitude do stop loss ou adicionar uma zona de buffer.

-

Em movimentos bruscos de preço, o stop loss dinâmico pode não acompanhar a velocidade.

- Reduzir o período de suavização para que o stop loss reaja mais rapidamente.

-

Rompimentos falsos podem causar perdas desnecessárias.

- Adicionar outros indicadores de confirmação para evitar sinais falsos.

-

Parâmetros inadequados podem prejudicar o desempenho.

- Realizar backtests em diferentes ciclos de mercado para encontrar os parâmetros ideais.

Ideias de Otimização

- Adicionar outros indicadores para confirmação, como padrões de candlestick, Bandas de Bollinger, RSI, etc., melhorando a qualidade dos sinais.

- Otimizar parâmetros para diferentes ativos e períodos, encontrando a melhor combinação.

- Tentar métodos como aprendizado de máquina para otimização adaptativa de parâmetros.

- Aprimorar o algoritmo de stop loss, minimizando acionamentos desnecessários sem comprometer a proteção.

- Combinar gestão de capital para otimizar o gerenciamento de posições.

- Considerar a adição de mecanismos de take profit automáticos.

Resumo

No geral, esta estratégia é uma abordagem robusta de acompanhamento de tendência. Em comparação com um stop loss fixo, ela utiliza um mecanismo dinâmico que ajusta a amplitude de acordo com a volatilidade do mercado, reduzindo a probabilidade de ser pego em stops. Além disso, a introdução da média Hull e da lógica de mudança de tendência permite respostas rápidas a reversões. No entanto, a estratégia apresenta riscos, como acionamento de stop loss em mercados laterais e rompimentos falsos. Por meio de otimizações adicionais nos parâmetros dos indicadores, no algoritmo de stop loss e no gerenciamento de posições, é possível obter um desempenho mais estável em diferentes mercados.

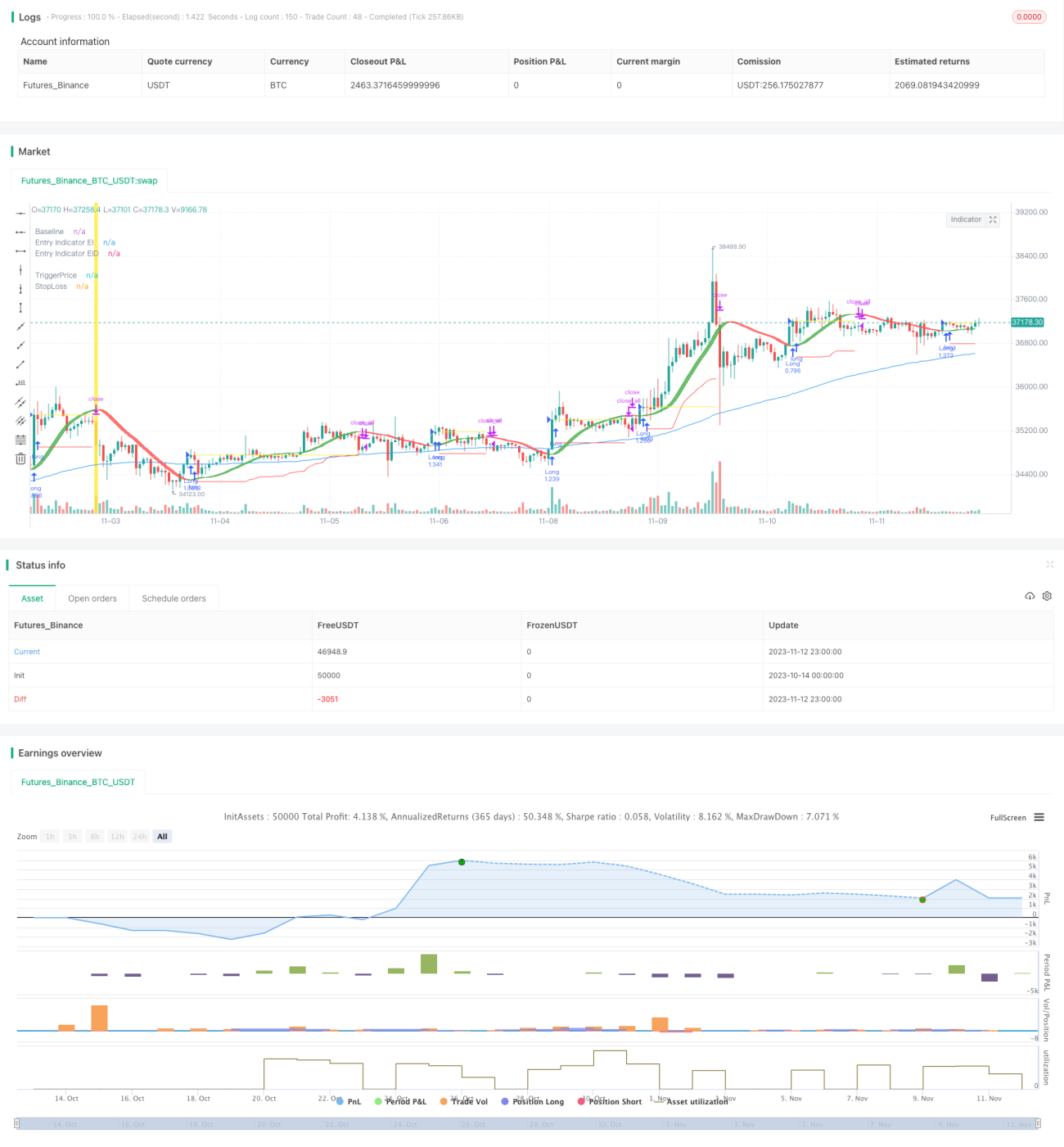

/*backtest

start: 2023-10-14 00:00:00

end: 2023-11-13 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// © Milleman

//@version=4

strategy("MilleMachine", overlay=true, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, initial_capital=10000, commission_type=strategy.commission.percent, commission_value=0.06)

- 1