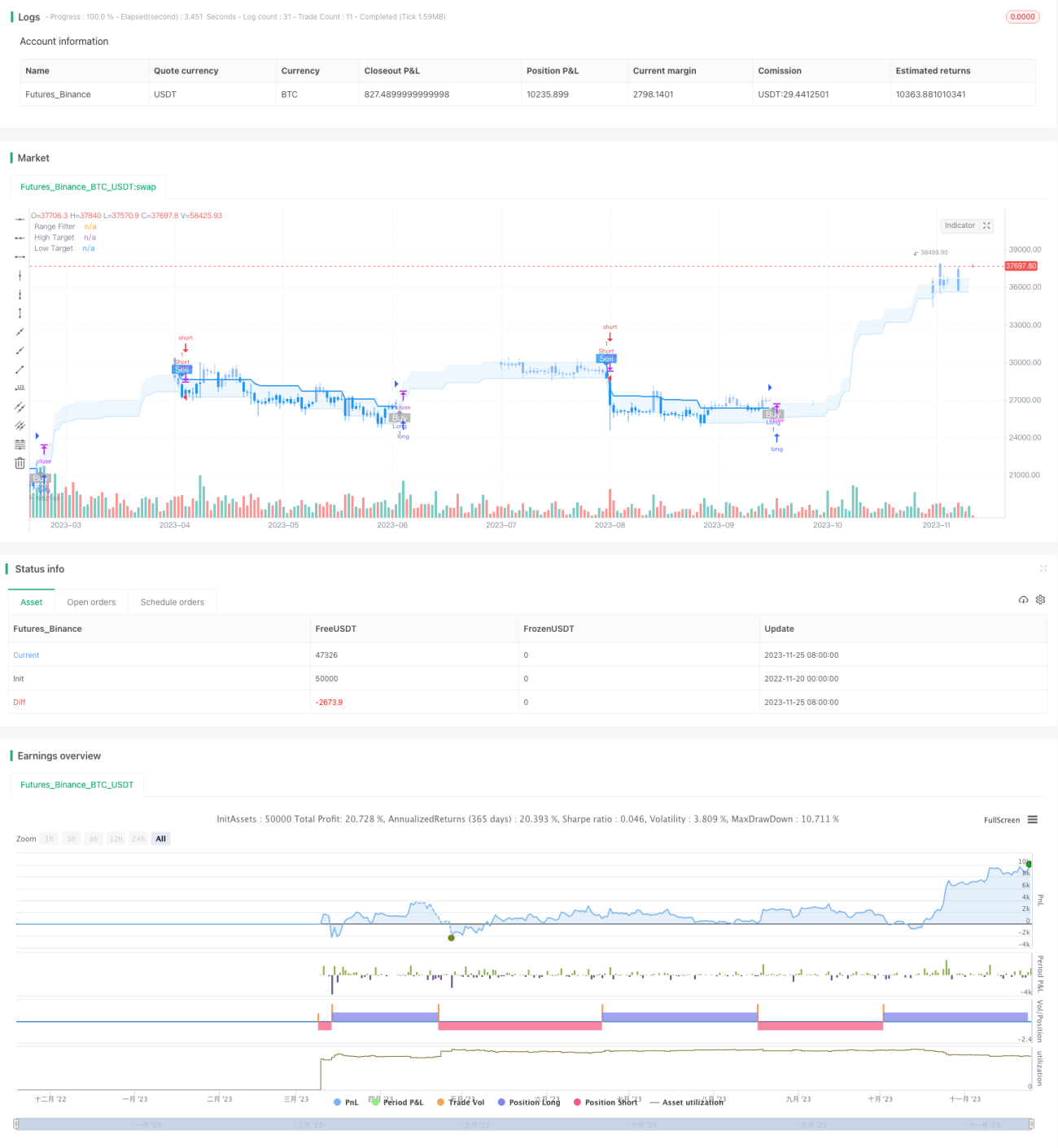

Estratégia de Rompimento de Tendência com Filtro de Duas Médias Móveis

Visão Geral

Esta é uma estratégia que utiliza médias móveis e Bandas de Bollinger para julgar a tendência, combinada com princípios de filtro de rompimento e stop loss. Ela pode capturar sinais rapidamente quando a tendência muda, reduz sinais falsos através de médias móveis duplas e define stop loss para controlar o risco.

Princípio da Estratégia

A estratégia é composta principalmente pelas seguintes partes:

-

Julgamento de Tendência: Utiliza o MACD para determinar a tendência de preço, distinguindo entre tendências de alta e baixa.

-

Filtro de Faixa: Utiliza as Bandas de Bollinger para avaliar a faixa de flutuação do preço, filtrando sinais que não rompem a faixa.

-

Confirmação por Médias Móveis Duplas: Uma combinação de EMA rápida e EMA lenta é usada para confirmar os sinais de tendência. O sinal de compra só é gerado quando a EMA rápida é maior que a EMA lenta.

-

Mecanismo de Stop Loss: Define um ponto de stop loss, liquidando a posição quando o preço rompe desfavoravelmente esse ponto.

A lógica para o sinal de entrada é:

- O MACD indica uma tendência de alta;

- O preço rompe a banda superior das Bandas de Bollinger;

- A EMA rápida está acima da EMA lenta.

Quando todas as três condições são atendidas simultaneamente, é gerado um sinal de compra.

A lógica de saída é dividida em dois tipos: take profit e stop loss. O ponto de take profit é o preço de entrada multiplicado por uma determinada proporção, e o ponto de stop loss é o preço de entrada multiplicado por uma determinada proporção. Quando o preço rompe um desses pontos, a posição é liquidada.

Análise de Vantagens

Esta estratégia apresenta as seguintes vantagens:

- Capacidade de capturar rapidamente mudanças de tendência, com poucos rastreamentos.

- Filtra sinais falsos através de médias móveis duplas, melhorando a qualidade dos sinais.

- O mecanismo de stop loss controla efetivamente as perdas individuais.

- Grande espaço para otimização de parâmetros, podendo ser ajustada para o estado ideal.

Análise de Riscos

A estratégia também apresenta alguns riscos:

- Sinais falsos em mercados laterais podem causar perdas.

- Um ponto de stop loss mal definido pode resultar em perdas desnecessárias.

- Parâmetros inadequados podem levar a um desempenho insatisfatório da estratégia.

Para mitigar esses riscos, é possível otimizar e melhorar a estratégia ajustando parâmetros e reposicionando o stop loss.

Direções de Otimização

A estratégia pode ser otimizada nas seguintes direções:

- Ajustar os períodos das médias móveis duplas para encontrar a melhor combinação de parâmetros.

- Testar diferentes tipos de stop loss, como stop loss dinâmico (trailing stop) ou stop loss por volatilidade.

- Testar os parâmetros do MACD para encontrar os valores ideais.

- Utilizar aprendizado de máquina para otimizar automaticamente os parâmetros.

- Adicionar condições extras para filtrar sinais.

Ao testar diferentes configurações de parâmetros e avaliar a rentabilidade e o índice de Sharpe, é possível encontrar o estado ótimo da estratégia.

Resumo

Esta é uma estratégia quantitativa que combina julgamento de tendência, filtro de faixa, confirmação por médias móveis duplas e o conceito de stop loss. Ela é capaz de julgar efetivamente a direção da tendência, equilibrando a maximização do lucro com o controle de risco. Através de otimização de parâmetros e aprendizado de máquina, esta estratégia ainda possui grande potencial de melhoria para obter melhores resultados.

/*backtest

start: 2022-11-20 00:00:00

end: 2023-11-26 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy(title="Range Filter Buy and Sell Strategies", shorttitle="Range Filter Strategies", overlay=true,pyramiding = 5)

// Original Script > @DonovanWall- 1